FY March 2026 Full Year Performance Briefing (Speech Text)

Noboru Saito

President & CEO

I am Noboru Saito, and I would like to thank you very much for joining us today.

Let me begin by mentioning the key points we wish to touch on today.

We grew our sales and our profits in the FY March 2026, setting new record highs for both. Our free cash flow also exceeded expectations, and we upwardly revised our shareholder return plan from the initial forecast to increase dividends.

Although the FY March 2027 has us facing headwinds such as the escalating situation in the Middle East and a decline in production volumes of smartphones and other ICT devices due to soaring memory prices, we will continue strengthening our management approach focused on “Controlling the Controllable,” that is, improving our own capabilities.

While we expect on the whole to achieve the targets laid out in our Medium-term Plan, we will be stepping up our business portfolio management even further.

Today, I will be explaining our investments in the AI ecosystem, which holds significant medium- to long-term potential for our company, discussing in particular the progress made in our growth strategies for AI data center-related products.

We are also pursuing closer dialogue with investors and analysts. On September 1, 2026, our Investor Day, we plan to discuss the software technologies we have newly added to our core technologies as well as our human capital.

These are the key points we want to share with you today.

Mr. Yamanishi will now take over to provide you with further details.

FY March 2026 Results Highlights

Tetsuji Yamanishi

Senior Executive Vice President & CFO

I am Tetsuji Yamanishi, and I will be presenting an overview of our consolidated financial results.

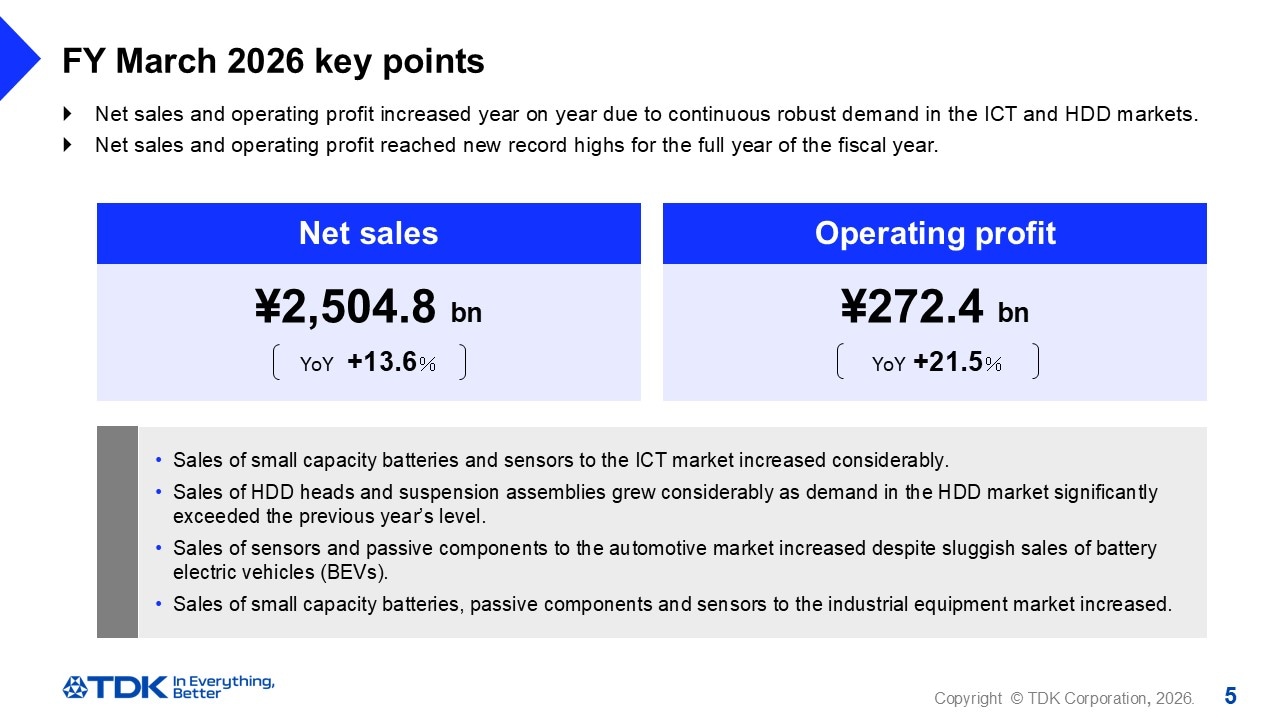

FY March 2026 key points

The first key point in our full-year financial results for the FY March 2026 is that production of ICT-related products for the electronics market, which significantly impacts our business performance, held steady year-on-year, and demand for the nearline HDDs used in data centers remained high.

In the industrial equipment market, demand for renewable energy applications stayed firm.

On the other hand, the automotive market experienced persistently sluggish demand for BEVs, keeping component demand short of initial projections.

Under these business conditions, component demand in the ICT and industrial equipment markets remained robust, leading to year-on-year net sales growth across all segments.

Overall, net sales increased by 13.6% and operating profit rose by 21.5%, with both reaching all-time highs.

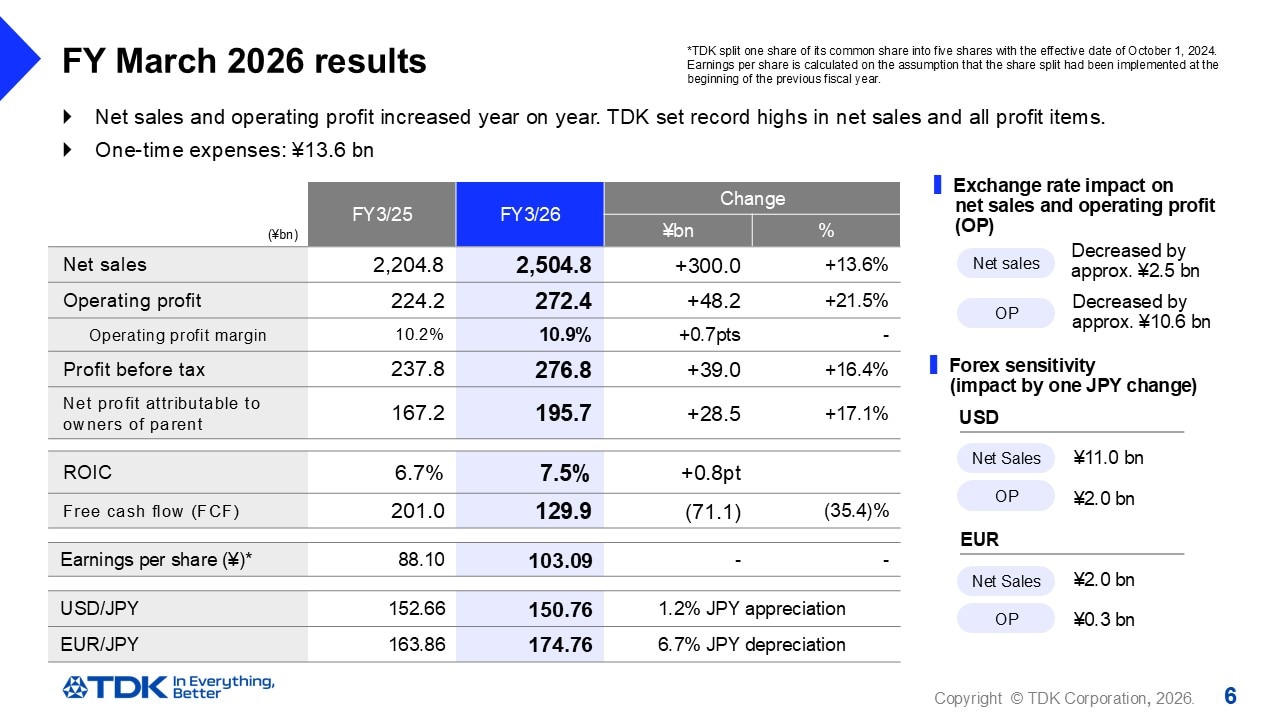

FY March 2026 results

Next, let me point out the full-year financial highlights.

Net sales fell by approximately 2.5 billion yen due to exchange rate fluctuations against the US dollar and other currencies, and operating profit dropped by approximately 10.5 billion yen as a result.

Net sales came in at 2,504.8 billion yen, up by 300.0 billion yen, or 13.6%, from the previous fiscal year.

Our operating profit was 272.4 billion yen, representing an increase of 48.2 billion yen, or 21.5%, from the previous fiscal year.

Profit before tax came to 276.8 billion yen, marking a 39.0 billion yen, or 16.4%, rise from the preceding fiscal year.

Net profit attributable to owners of parent moved higher by 28.5 billion yen, or 17.1%, year-on-year to 195.7 billion yen, so both net sales and profit figures set new records.

Earnings per share were 103.09 yen. Regarding the sensitivity of operating profit to exchange rates, we estimate that a 1-yen fluctuation in the yen-dollar exchange rate produces an annual impact of approximately 2.0 billion yen and in the yen-euro exchange rate an impact of about 300 million yen, as it did last year.

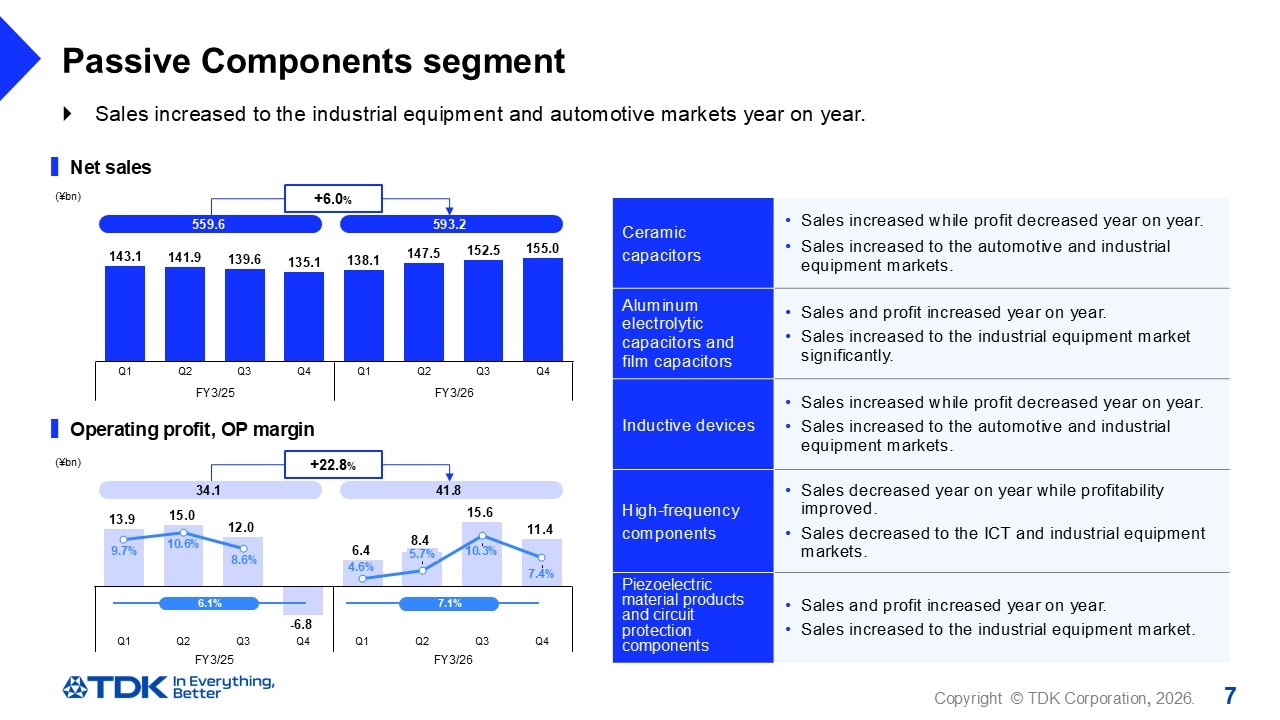

Passive Components segment

Now let’s look at the full-year results by segment, starting with Passive Components.

Sales to the industrial equipment and automotive markets increased, resulting in net sales of 593.2 billion yen, a 6.0% increase year-on-year, and operating profit of 41.8 billion yen, a 22.8% increase year-on-year.

Sales of ceramic capacitors to the automotive and industrial equipment markets did increase but, due to lower average selling prices, operating profit declined.

Sales of aluminum electrolytic capacitors and film capacitors to the industrial equipment market – including those for renewable energy and AI server applications – climbed, leading to higher revenue. Restructuring costs of 2.8 billion yen were incurred as part of our business portfolio management, primarily in the first half of the fiscal year, but operating profit was nevertheless up.

Sales of inductive devices to the automotive and industrial equipment markets rose, generating higher net sales. However, profits were down slightly due to a deterioration in product mix.

Sales of high-frequency components to the ICT and industrial equipment markets dropped, but profitability improved.

Sales of piezoelectric material products and circuit protection components to the industrial equipment market expanded, resulting in higher net sales and profits.

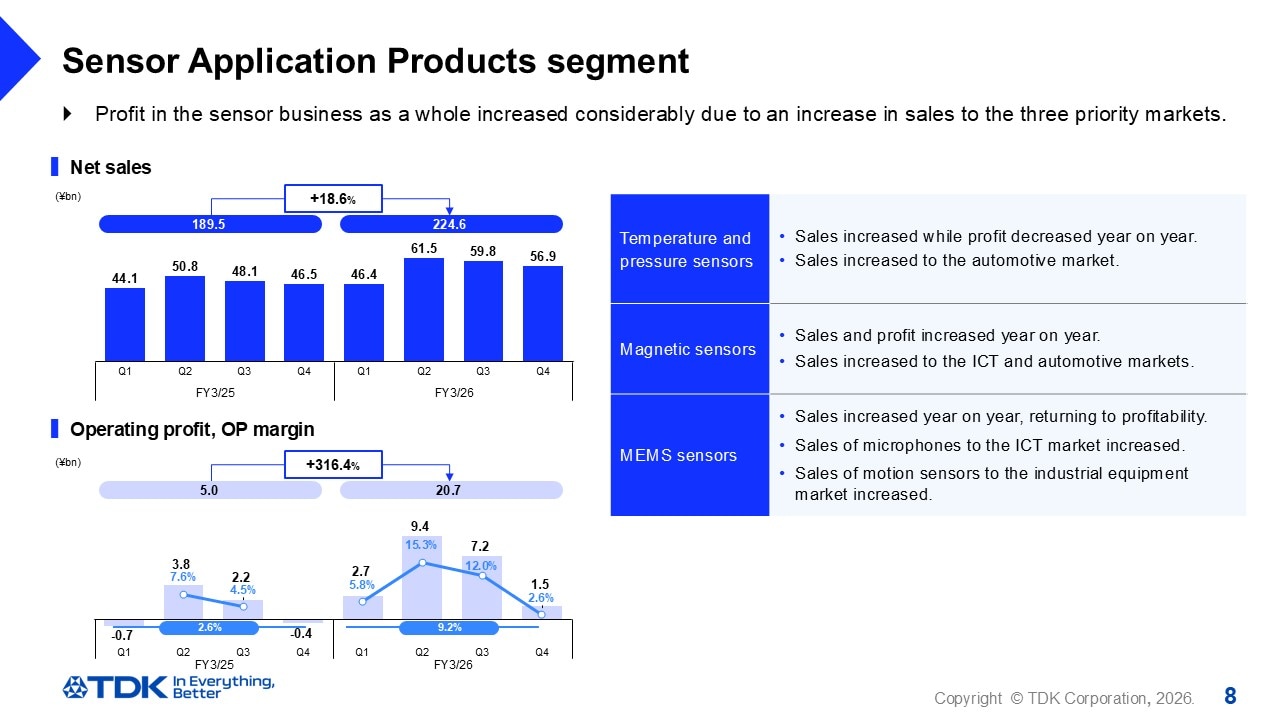

Sensor Application Products segment

Next comes the Sensor Application Products segment.

Net sales were 224.6 billion yen, up 18.6% year-on-year, while operating profit was 20.7 billion yen, approximately four times higher than the previous year.

Although sales of temperature and pressure sensors increased due to higher sales in the automotive market, profit declined due to such factors as a deterioration in product mix.

In magnetic sensors, sales of TMR sensors for smartphones increased, as did sales in the automotive market, leading to higher sales and profit for the magnetic sensor business as a whole.

For MEMS sensors, sales of microphones to the ICT market and of motion sensors for industrial equipment rose, resulting in higher sales for MEMS sensors overall. The MEMS sensors moved from a loss in the previous year to a profit, contributing significantly to the improvement in overall sensor business earnings.

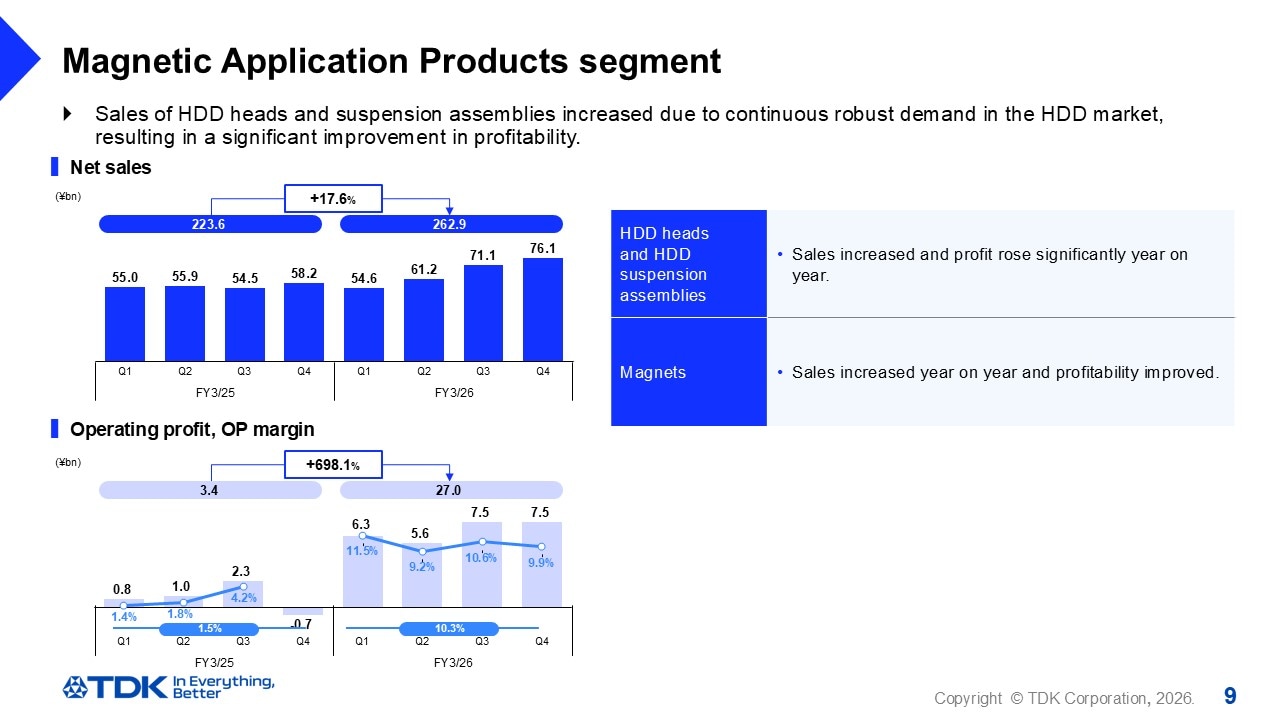

Magnetic Application Products segment

Let’s look next at the Magnetic Application Products segment, where sales were up 17.6% year-on-year to 262.9 billion yen and operating profit enjoyed a significant eightfold increase to 27.0 billion yen.

The HDD heads and suspension assemblies businesses saw sales for nearline HDDs increase by approximately 14% for heads and 35% for suspension assemblies, significantly boosting both net sales and profit.

Net sales for the magnet business rose due to higher sales in the automotive market, and the overall loss narrowed thanks to cost-saving measures such as quality improvements.

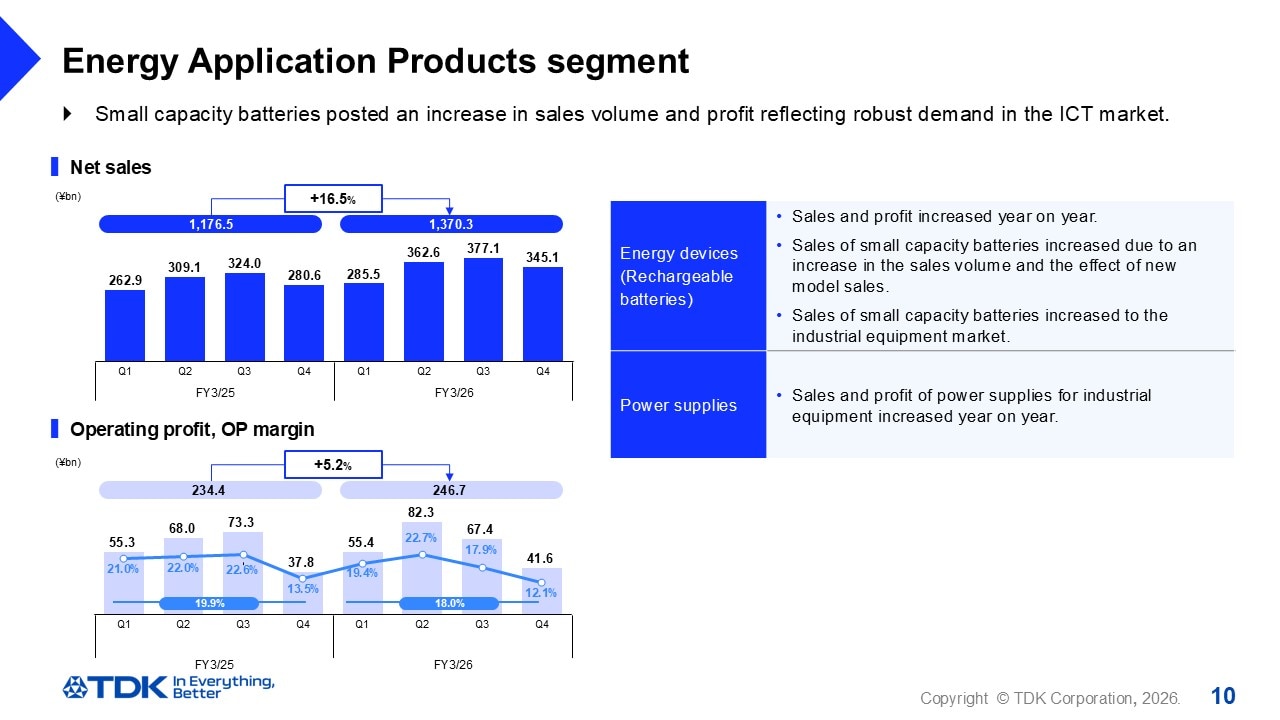

Energy Application Products segment

Let’s take a look now at Energy Application Products. Net sales came to 1.3703 trillion yen, up 16.5% year-on-year, and operating profit to 246.7 billion yen, up 5.2%.

In the rechargeable battery business, higher sales of small-capacity batteries for smartphones were driven by the launch of new models among other factors, while sales of medium-capacity batteries also rose due to increased demand in the industrial equipment market, giving the rechargeable battery business as a whole higher net sales and profit.

A gradual recovery in demand was observed in the industrial equipment power supply business, with the outcome being higher net sales and profit.

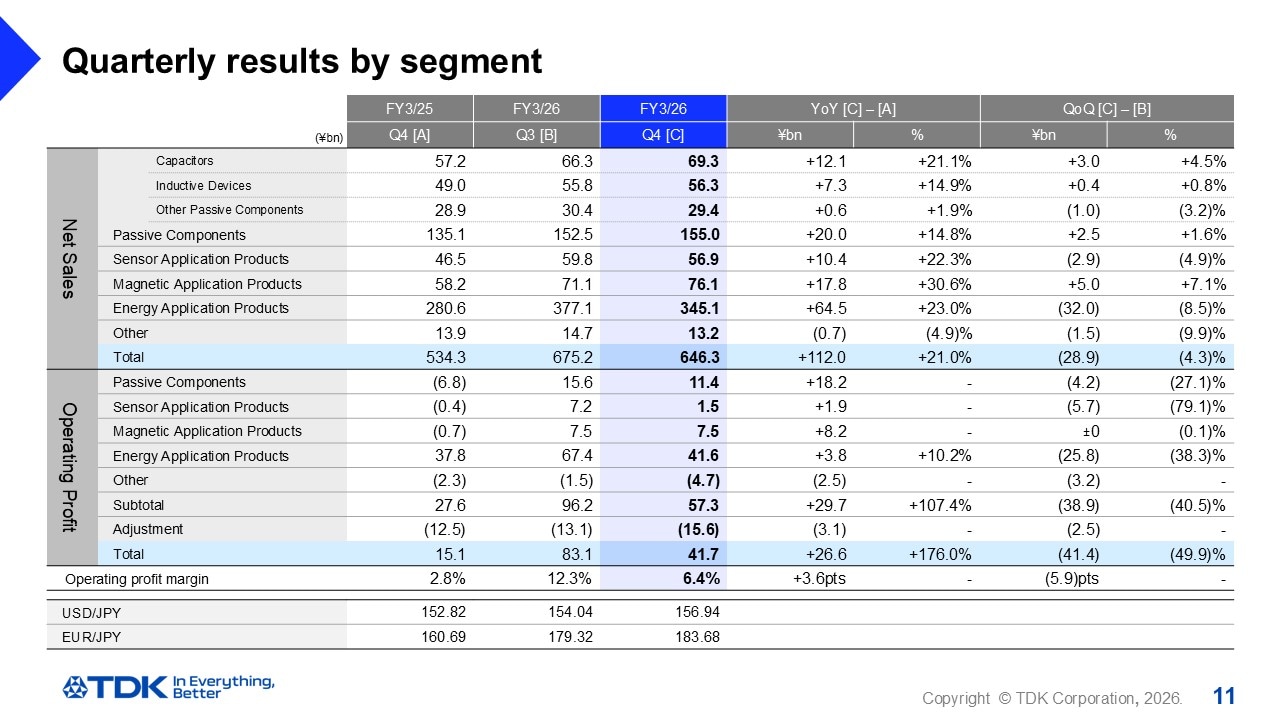

Quarterly results by segment

I will now go segment by segment to explain the factors contributing to the changes in net sales and operating profit from the third quarter to the fourth quarter.

Starting with the Passive Components segment, net sales increased by 2.5 billion yen, or 1.6%, from the third quarter, while operating profit decreased by 4.2 billion yen, partly due to the recognition of property taxes and other expenses.

Although sales of ceramic capacitors to the automotive market declined, sales to the industrial equipment market including AI data center applications increased, leading to higher net sales even as profit remained at roughly the same level. Expanded sales of aluminum electrolytic capacitors and film capacitors for the renewable energy and AI data center applications produced higher net sales and operating profit. Sales of inductors remained flat, while profit fell due to a deterioration in product mix and operational losses caused by the Spring Festival holiday at our Chinese facilities. Sales of high-frequency components to the ICT market dropped due to seasonal factors, resulting in lower net sales and profit; however, piezoelectric material products and circuit protection components saw both net sales and profit increase.

Next, net sales of sensor application products fell by 2.9 billion yen (4.9%) from the third quarter, dragging operating profit down significantly to 5.7 billion yen. Sales of temperature and pressure sensors remained flat, but the sector posted a loss due to the recognition of 300 million yen in restructuring costs. Among magnetic sensors, sales of Hall sensors saw no major change, while sales of TMR sensors to the ICT market declined due to seasonal factors, resulting in a decrease in overall magnetic sensor sales. The recognition of 1.2 billion yen in restructuring costs pulled operating profit for Hall sensors down considerably. In MEMS sensors, sales of both microphones and motion sensors stayed level but profit shrank due to the recognition of restructuring costs.

Looking now at the Magnetic Application Products segment, net sales increased by 5.0 billion yen (7.1%) from the third quarter, while operating profit held steady. Sales volume of HDD heads was higher by 9%, resulting in higher net sales and profit. Sales volume of suspension assemblies was down by 5% in reaction to front-loaded shipments in the third quarter, resulting in lower sales and profit. Overall, the HDD heads and suspension assemblies saw higher net sales but lower profits. Increases in material costs were reflected in selling price increases for magnets, leading to higher net sales and a narrowed loss.

Finally, net sales in the Energy Application Products segment fell by 8.5% to 32.0 billion yen from the third quarter, and operating profit dropped by 38.3% to 25.8 billion yen. In rechargeable batteries, the sales volume of small-capacity batteries for the ICT market was down by approximately 14% due to seasonal factors, the consequence being lower net sales and operating profit. Industrial equipment power supplies showed signs of a recovery in demand, generating increased net sales and operating profit.

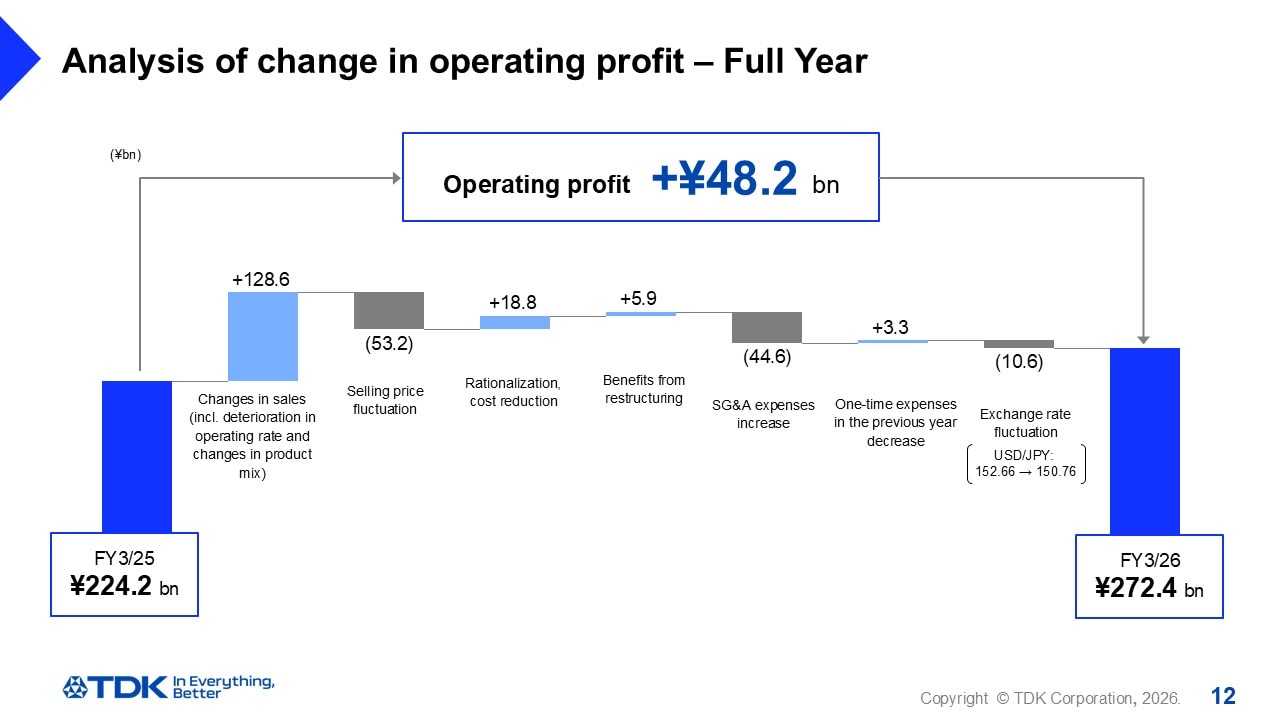

Analysis of change in operating profit – Full Year

Analyzing the 48.2 billion yen increase in operating profit, we see that growing sales volume across all segments contributed to a 128.6 billion yen increase in profit.

Rationalization and cost-cutting measures contributed 18.8 billion yen and the effects of restructurings implemented in the previous fiscal year added another 5.9 billion yen increase, while sales discounts brought about a 53.2 billion yen decrease in profit.

Selling, general, and administrative expenses (SG&A) increased by 44.6 billion yen, primarily due to higher R&D expenses connected with the accelerated development of new technologies and products, particularly in rechargeable batteries.

Despite the negative impacts of 3.3 billion yen in one-time gains recognized in the previous year being absent, 6.6 billion yen from reduced restructuring costs, and 10.6 billion yen from the appreciation of the yen, overall operating profit rose by 48.2 billion yen thanks to higher sales volumes.

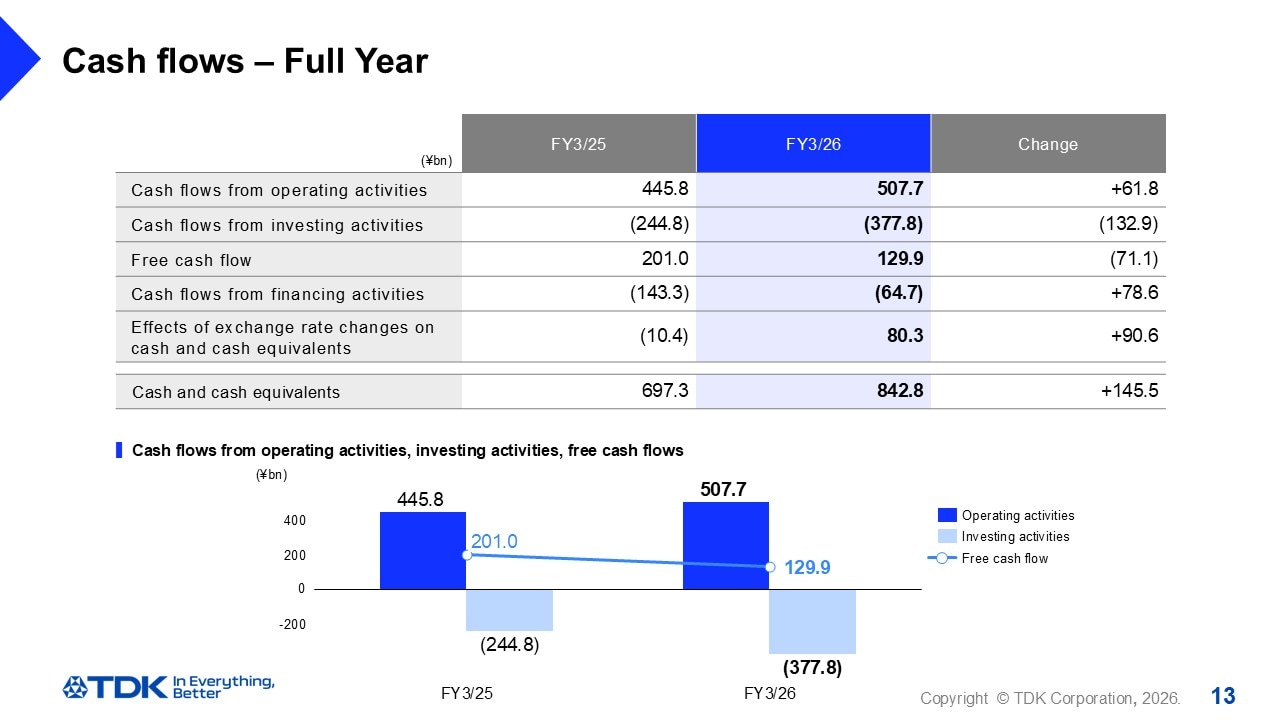

Cash flows – Full Year

Here I would like to explain our cash flow situation.

Our operating cash flow for the full year was 507.7 billion yen.

Investing Cash flows climbed by 132.9 billion yen year-on-year, driven by higher capital expenditures (CAPEX)—primarily for rechargeable batteries—to support new products and technologies.

Free cash flow amounted to 129.9 billion yen, down 71.1 billion yen from the previous year but still above our projected level.

FY March 2027 Projections

I will discuss our projections for the full-year of FY March 2027.

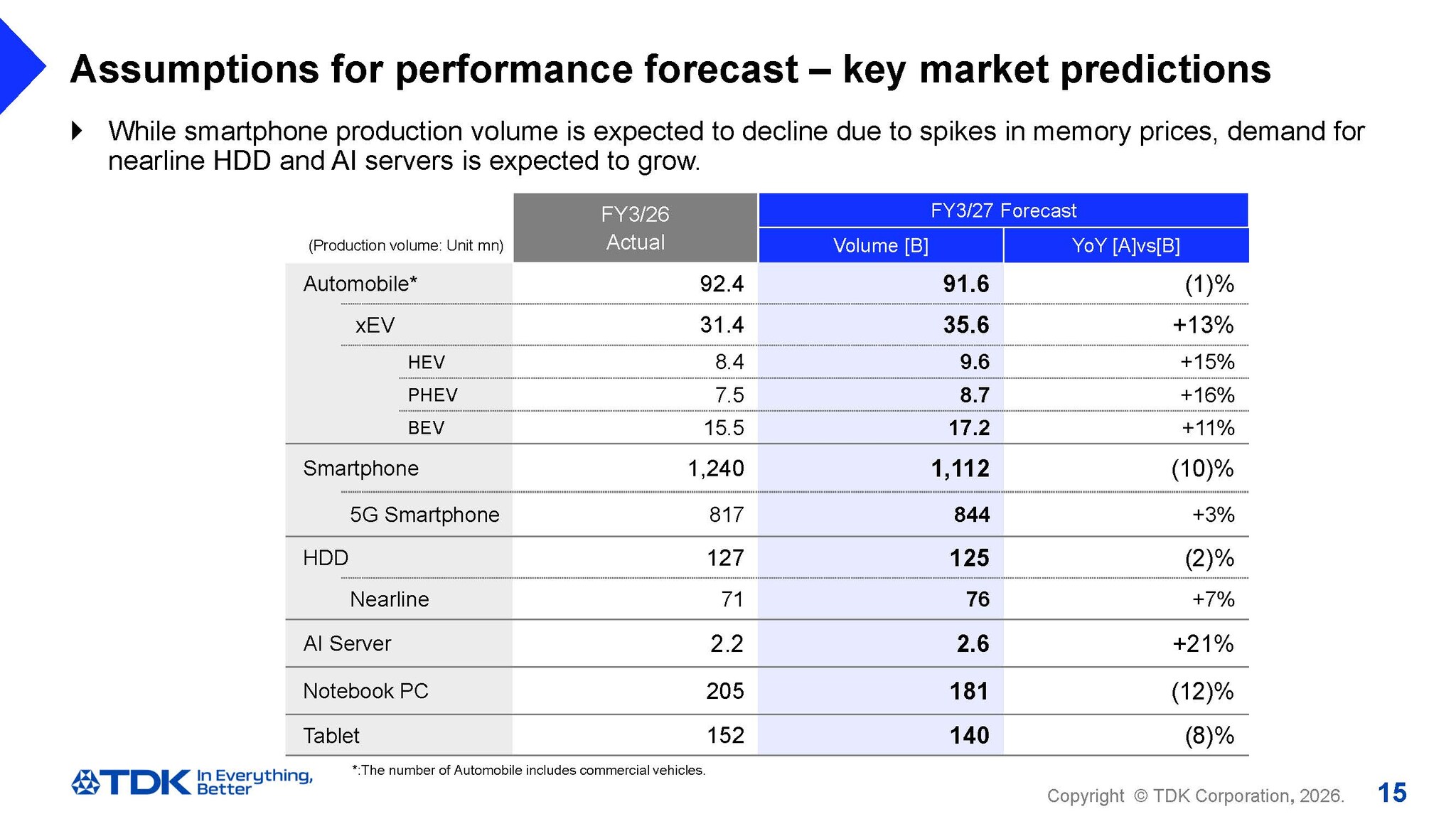

Assumptions for performance forecast - key market predictions

I’ll begin by discussing the production volume forecasts for key devices that form the basis of our earnings projections.

We expect total production in the automotive market to decline by about 1%, but xEV production to increase by around 13%.

For smartphone production volumes—a key indicator of the ICT market—we anticipate a 10% decline to 1.112 billion units due to the impact of memory shortages.

While overall production in the HDD market is expected to slow by approximately 2%, demand for AI data centers remains strong, and we expect production of nearline HDDs for data centers to increase by 7%.

As with smartphones, we also predict production of notebook PCs and tablets to drop by 12% and 8%, respectively, due to memory shortages.

Given the growing demand for AI servers, we have included an additional forecast for AI server boards, which we anticipate to rise by 21%.

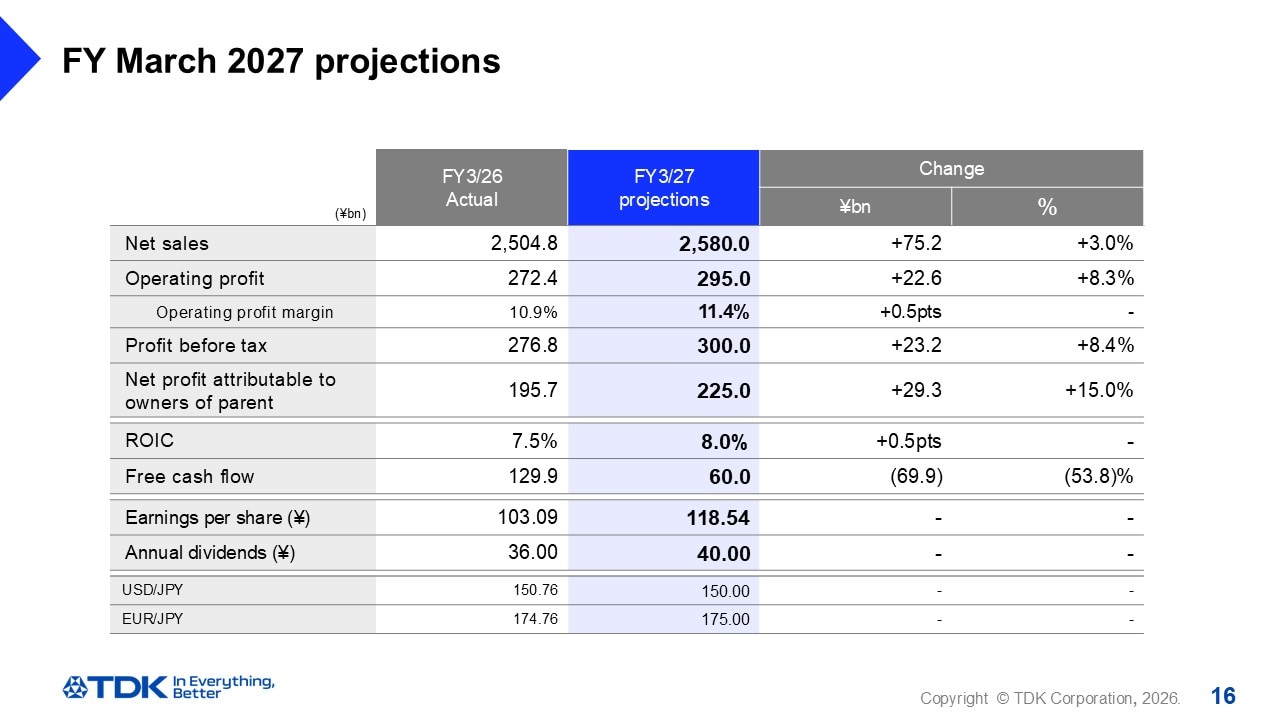

FY March 2027 projections

Now let’s examine our earnings projections for the FY March 2027.

Based on the market forecasts for key devices we just covered and on recent demand trends, our full-year projections are net sales of 2.58 trillion yen, operating profit of 295 billion yen, and net profit attributable to owners of parent of 225 billion yen. These figures assume average exchange rates of 150 yen to the dollar and 175 yen to the euro, roughly equivalent to the average for the FY March 2026.

With a view to medium-term growth, we plan to significantly increase CAPEX, which should generate free cash flow of 60 billion yen.

We anticipate incurring one-time expenses, including restructuring costs, of approximately 6 billion yen as part of our business portfolio management.

Based on our higher profit projections, we plan to pay 20 yen per share for both the interim and year-end dividends, totaling 40 yen for the full year.

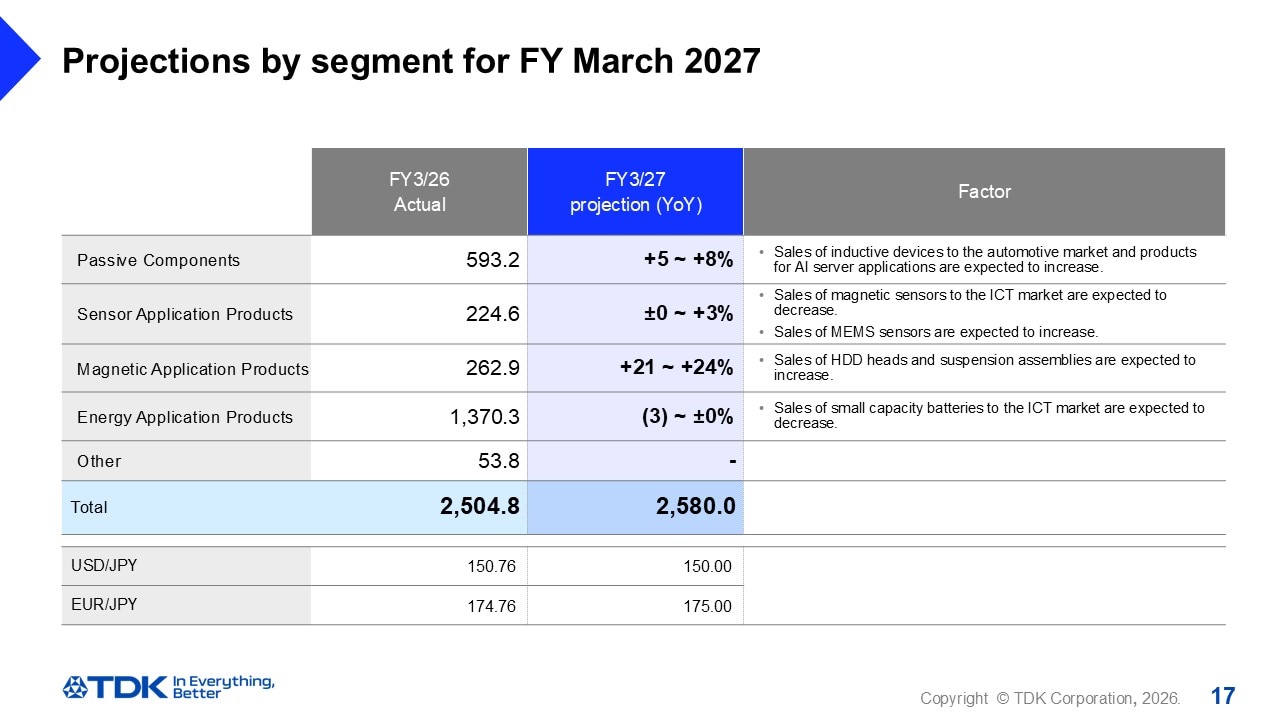

Projections by segment for FY March 2027

This slide shows projected changes in net sales by segment for the full fiscal year.

Please note that the impact of exchange rates is minimal, so we will base our comparisons on the published figures.

First, we anticipate a 5% to 8% increase overall for Passive Components, driven by growth in inductive devices to the automotive market and increased sales of various products—including aluminum electrolytic capacitors—for AI server applications.

In Sensor Application Products, we anticipate a decline in sales volume for magnetic sensors but a rise in sales of MEMS sensors, including new microphone products. Consequently, we project overall growth of between 0% and 3%.

Next, in the Magnetic Application Projects sector, sales of HDD heads for nearline HDDs are expected to increase by approximately 50% in volume, driven by orders from captive manufacturers. Sales volume for suspension assemblies is also forecast to climb by approximately 22%, leading to a significant overall increase of 21% to 24%.

Coming finally to Energy Application Products, smartphone production volumes are expected to decline by approximately 10% and sales volumes for small capacity batteries are projected to decrease by about 7% due to product mix improvements and market share gains, resulting in an overall forecast of -3% to ±0%.

Analysis of change in operating profit projection

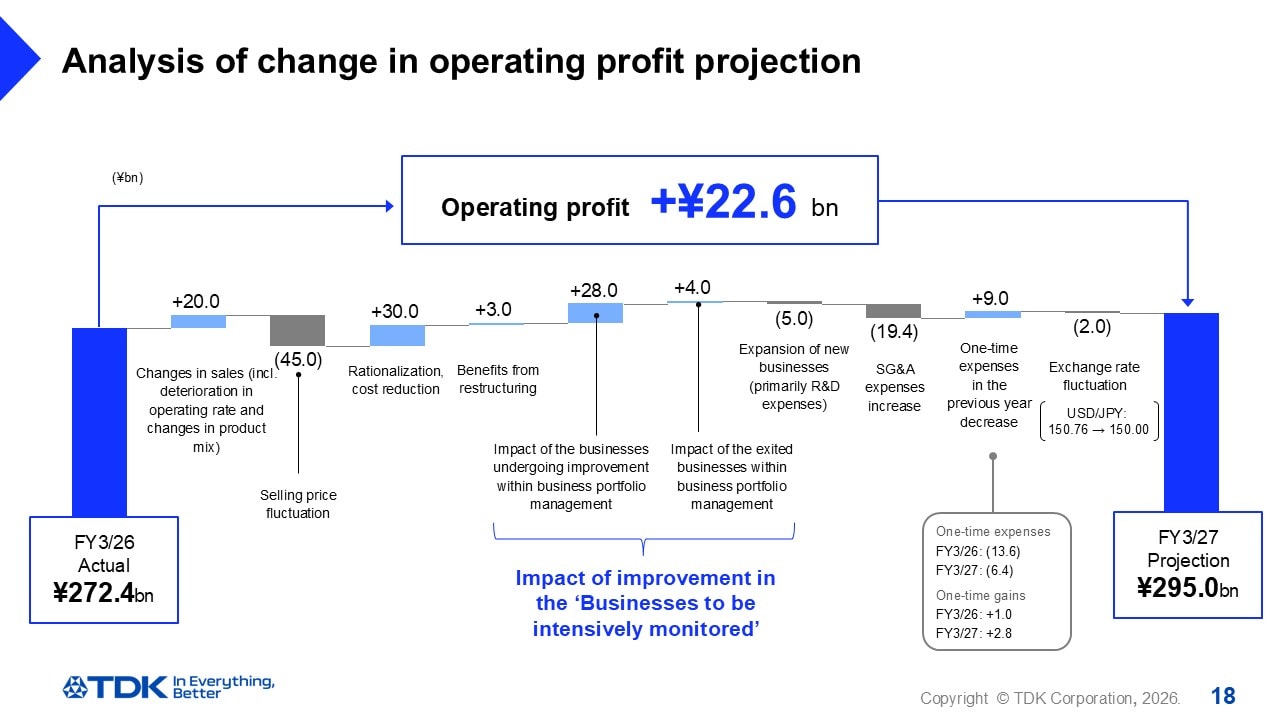

Let’s look now at the projected changes in operating profit for the FY March 2027.

Operating profit is expected to increase by 20 billion yen due to higher sales volumes, primarily in passive components, and by 28 billion yen due to improved profitability in businesses undergoing improvement within our portfolio management strategy, key among these being HDD heads and aluminum electrolytic capacitors. Additionally, we anticipate a 4.0 billion yen increase in profit due to reduced losses stemming from our withdrawal from such businesses such as EV power supply and camera module actuators.

Furthermore, we expect to absorb the 45.0-billion-yen decrease impact of selling price fluctuations while profit increase with enhancing cost competitiveness through 30.0 billion yen in cost cuts from rationalization efforts, 3.0 billion yen from restructurings implemented in the previous fiscal year, and a 9.0 billion yen reduction in one-time expenses.

In aiming for future growth, we plan to increase R&D expenses primarily to strengthen the development of new products and technologies, particularly in rechargeable batteries and HDD heads, resulting in a 19.4 billion yen increase in SG&A expenses. We also plan to invest 5 billion yen, mainly for R&D expenses, to expand new businesses such as edge AI-related operations.

Finally, we anticipate an overall profit increase of 22.6 billion yen, inclusive of a 2-billion-yen negative impact from a stronger yen.

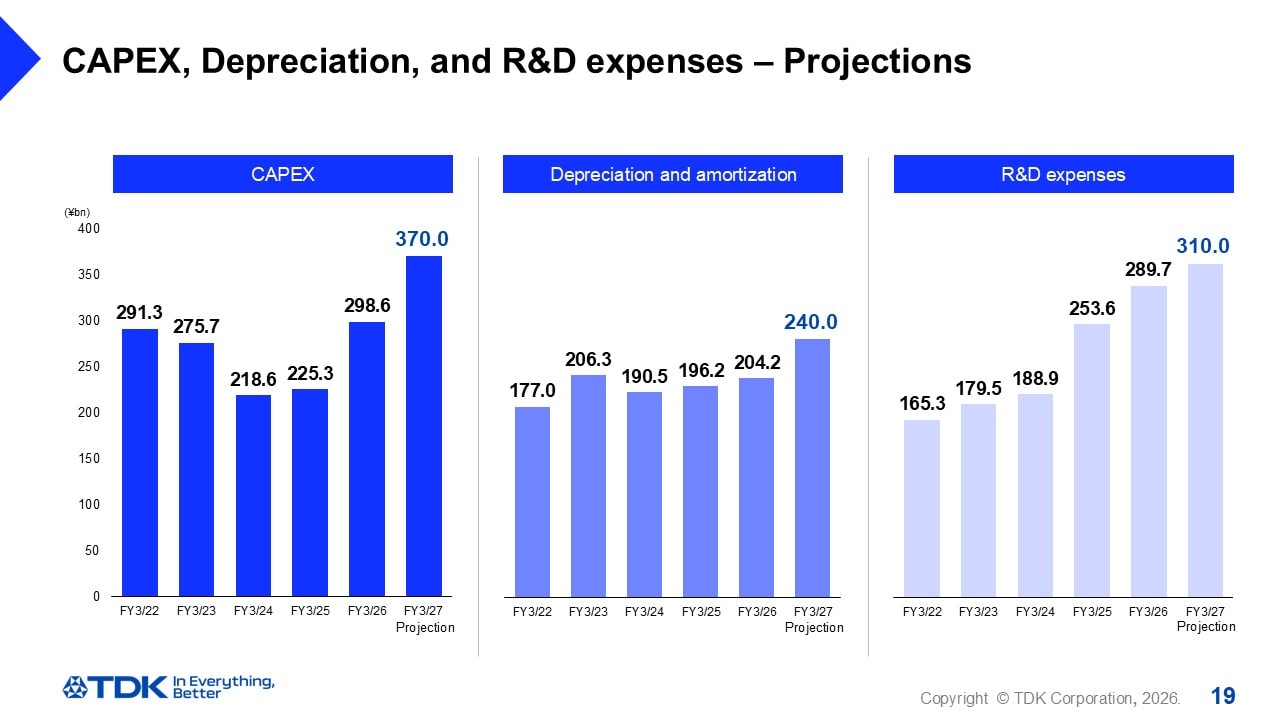

CAPEX, Depreciation, and R&D expenses – Projections

Next, we have our projections for various expenses.

We plan to invest a total of 370 billion yen in capital expenditures. This includes proactive investments in new technologies and product launches for small capacity batteries, as well as capacity expansion for battery packs. Additionally, we anticipate investments in HDD head equipment to support the expected growth in HAMR and further capacity expansion for suspension assemblies.

Depreciation expenses are likely to reach 240 billion yen, partly due to the increase in capital expenditures made in the FY March 2026.

R&D expenses should amount to 310 billion yen, allocated to the development of new rechargeable battery technologies, HAMR development for HDD heads, and accelerated development aimed at expanding new businesses related to edge AI.

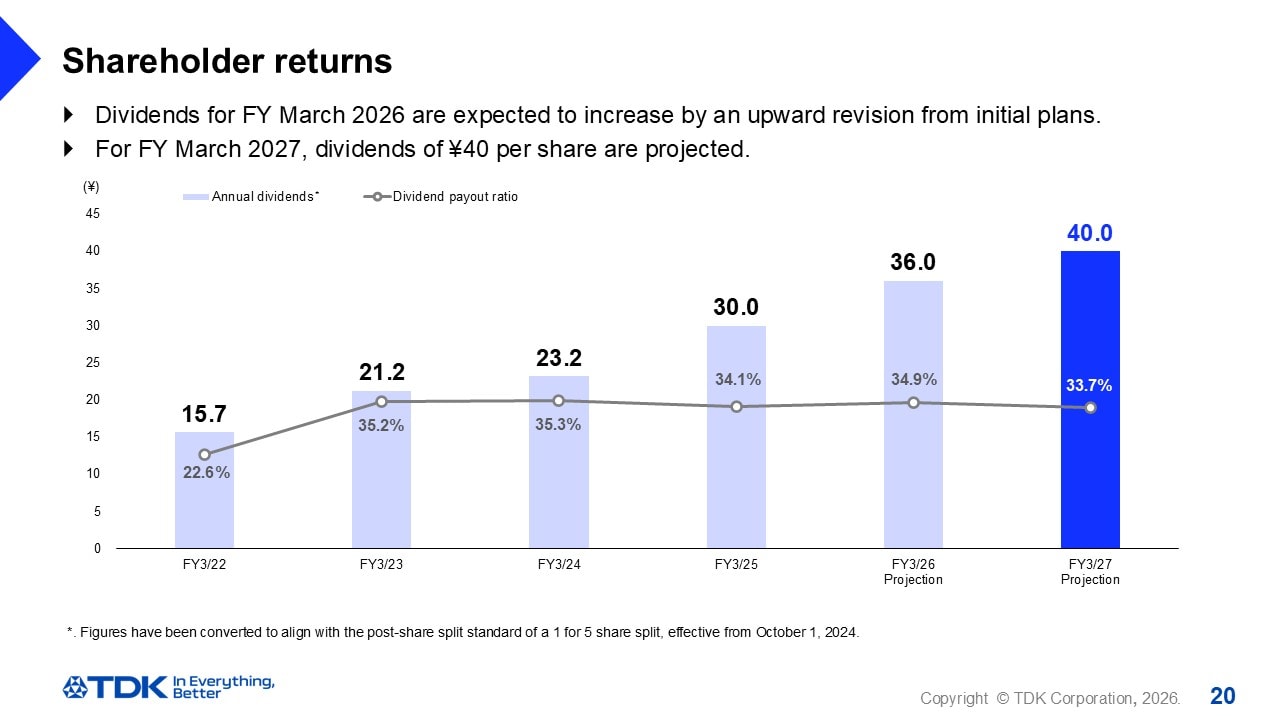

Shareholder returns

Finally, I would like to discuss dividends. During the period of our current Medium-term Plan, our policy is to return value to shareholders based on a dividend payout ratio of 35%.

We had originally planned an interim dividend of 16 yen and a year-end dividend of 18 yen as of the third quarter of the FY March 2026. In light of increased profit, however, we plan to raise the year-end dividend to 20 yen, resulting in an annual dividend of 36 yen.

For the FY March 2027, we intend to increase the dividend to 20 yen for both the interim and year-end dividends – a total of 40 yen for the full year – based on increased profit.

We will continue to consider appropriate shareholder returns in keeping with our future profit performance and our cash position.

That concludes my presentation.

Progress on Medium-term Plan

Noboru Saito

President & CEO

I am Noboru Saito and will now discuss the progress made in carrying out our Medium-term Plan.

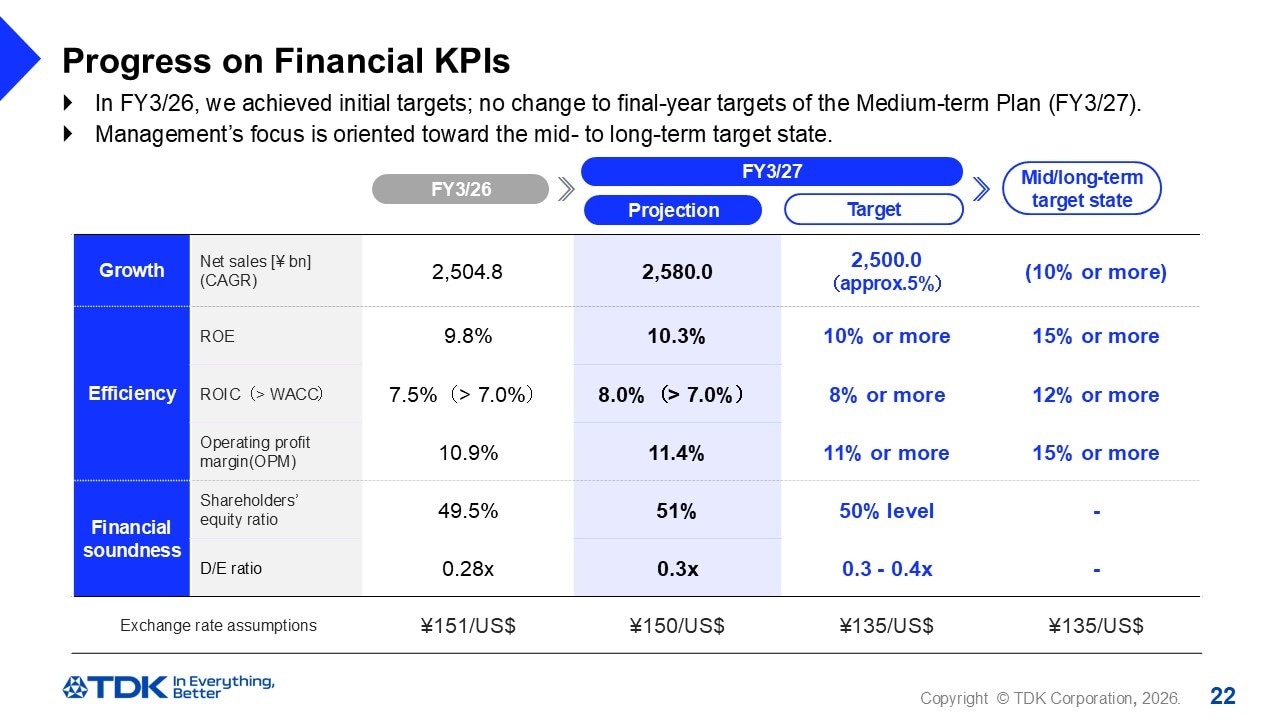

Progress on Financial KPIs

Let’s start out by looking at the actual results and outlook for financial KPIs under our Medium-term Plan.

For the FY March 2026, we achieved record-high net sales and operating profit across all segments, meeting all KPIs.

For the FY March 2027, we will strengthen both financial and pre-financial initiatives and focus on improving capital efficiency by further enhancing our own capabilities toward achieving our targets for the final year of the Medium-term Plan.

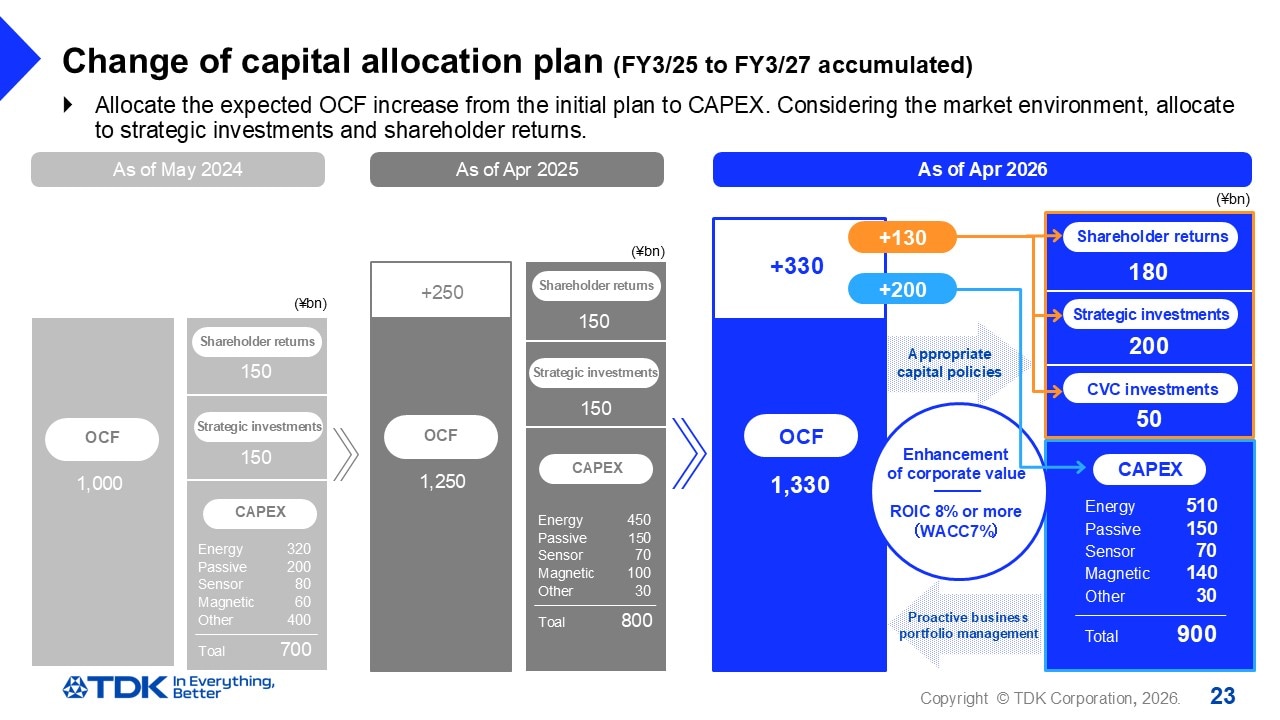

Change of capital allocation plan

Next, let’s examine the progress made in our capital allocation plan.

We had originally projected cumulative operating cash flow of approximately one trillion yen over the three-year period; with free cash flow having exceeded expectations in both of the first two years, though, we now expect the three-year total to exceed the initial plan by approximately 300 billion yen.

About 130 billion yen of this amount will be used to flexibly address shareholder returns and strategic investments while closely monitoring market conditions.

We will also increase capital expenditures by approximately 200 billion yen, allocating this extra amount primarily to the Energy and Magnetic Applications segments.

Due to strong demand for innovative technologies in small capacity batteries, we plan to increase investment in technical facilities for the Energy Application Products segment.

We are also looking to continuously expand capacity in the Magnetic Application Products segment in response to strong demand for both HDD heads and suspension assemblies. For HDD heads, this will involve capital expenditures in preparation for the launch of HAMR.

We further intend to continue actively investing in the AI ecosystem from our strategic investment budget, as demonstrated by our acquisition of SoftEye last year.

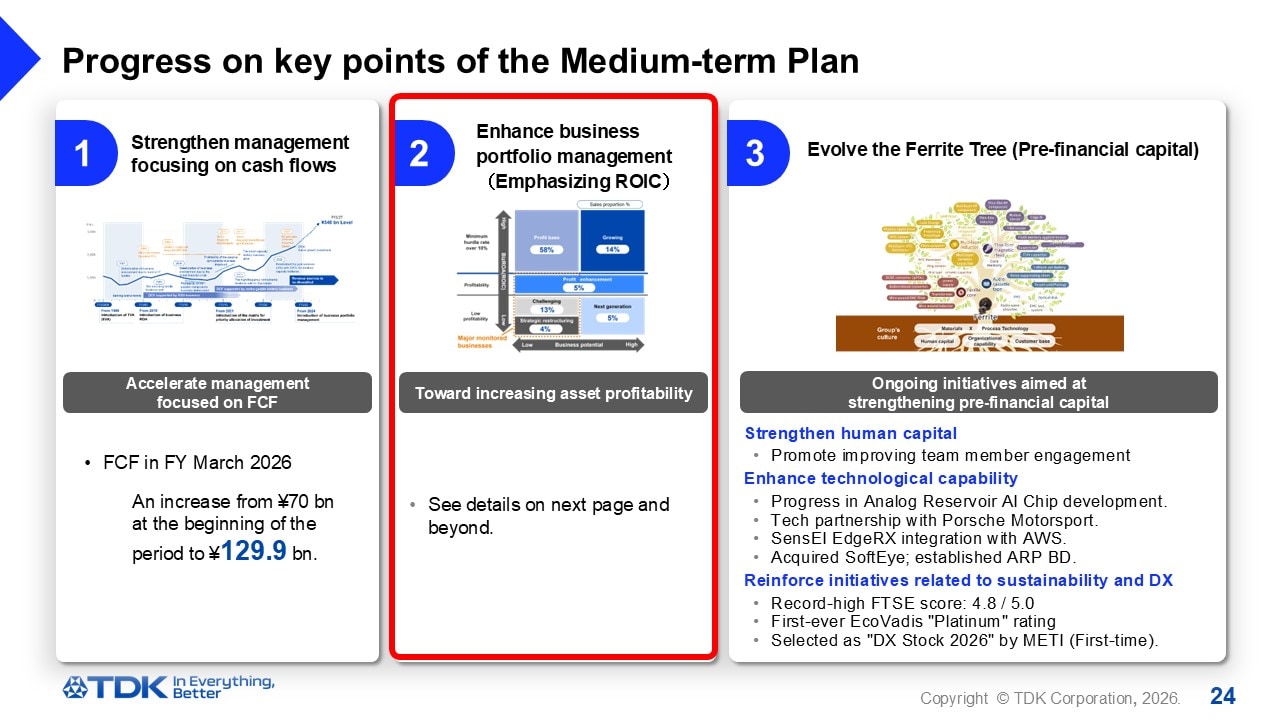

Progress on key points of the Medium-term Plan

Next is the topic of progress made on the three key points of our Medium-term Plan.

As I mentioned earlier regarding the first point – strengthening management focusing on cash flows – we have exceeded our initial projections and achieved our targets.

For the third point, – evolving the Ferrite Tree, and specifically, the strengthening of pre-financial capital – you can see here that we have made various strides.

In addition to these efforts, we will continue enhancing our sustainability initiatives and digital transformation (DX) efforts to significantly advance the Ferrite Tree.

As for the second point, proactive business portfolio management, I will explain the details in the following slides, as I did last time.

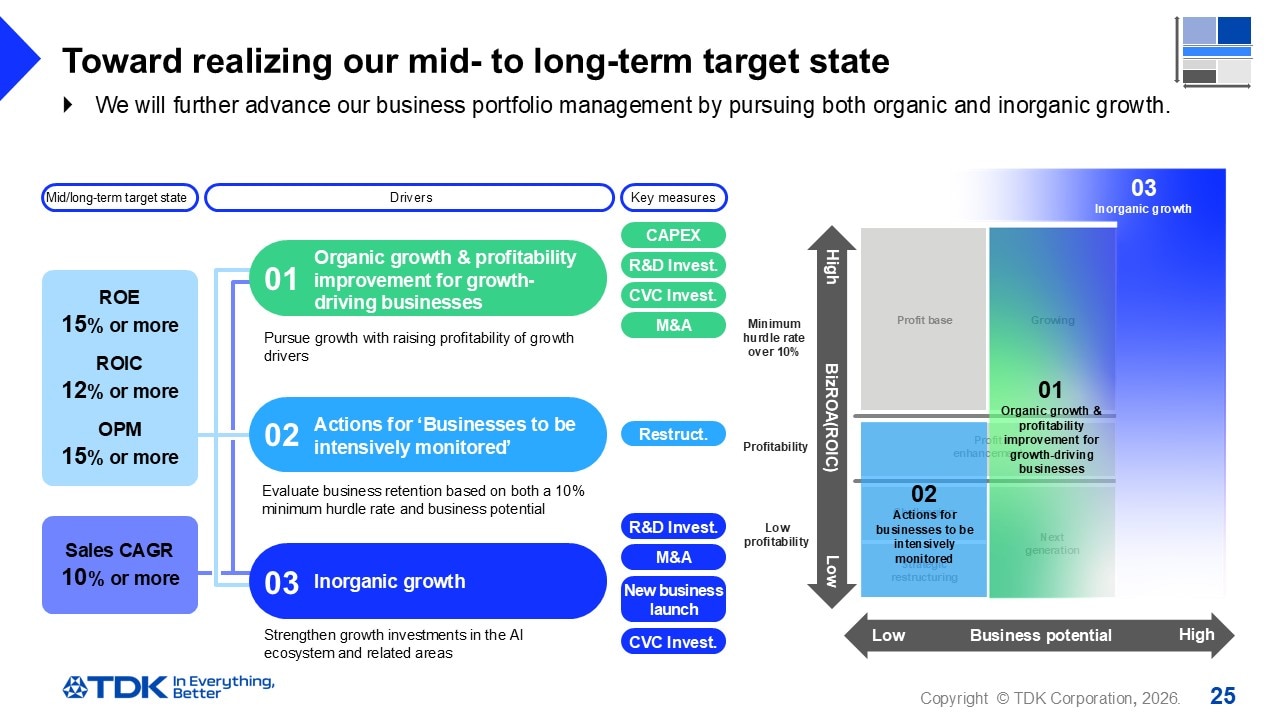

Toward realizing our mid- to long-term target state

As I mentioned in the Investor Day held in November 2025, we are upgrading, accelerating, and advancing our proactive business portfolio management to achieve our medium- to long-term targets of an ROE of 15% or higher and an ROIC of 12% or higher.

To reiterate, the primary objective of our business portfolio management is to drive our growth strategy.

There are three key points:

- Organic growth in our growth-driving businesses.

- Actions for ‘Businesses to be intensively monitored’.

- Inorganic growth, including R&D investment, CVC investment, and M&A.

(Reference) TDK Investor Day 2025: Medium-term Plan Update

https://www.tdk.com/en/ir/ir_events/strategy/20251128/index.html

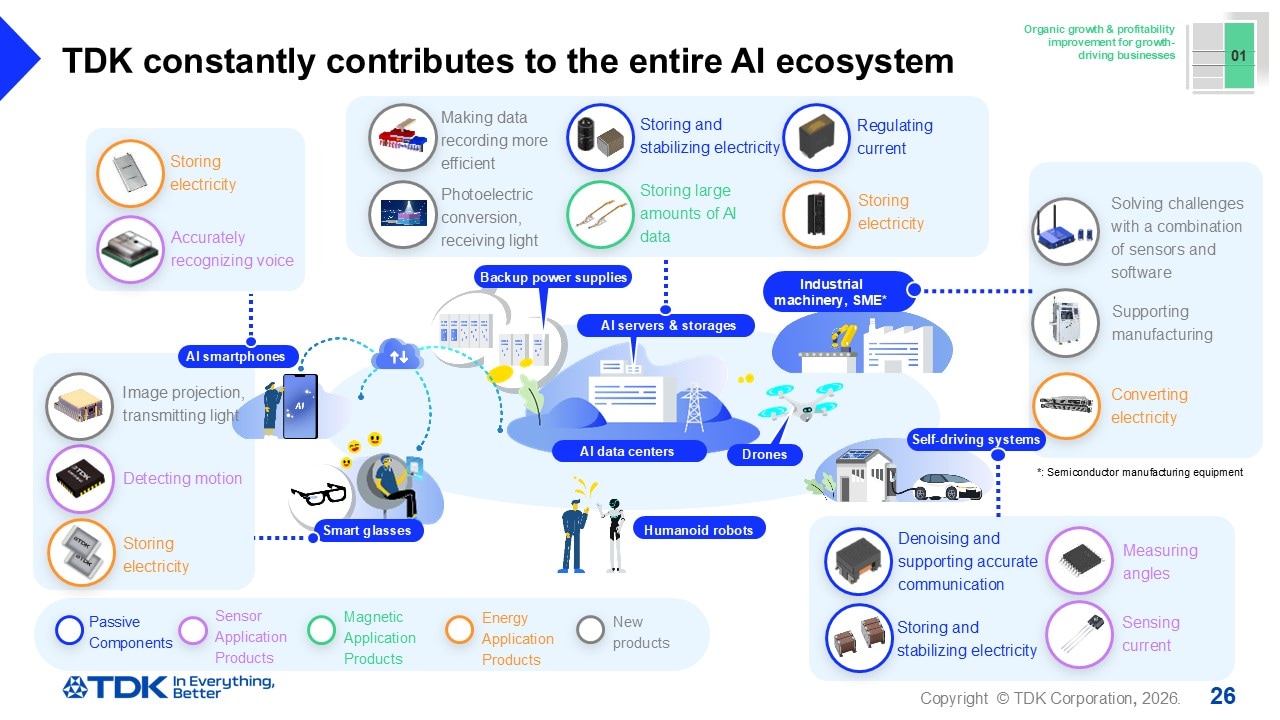

TDK constantly contributes to the entire AI ecosystem

As I noted earlier, our company views the various applications related to AI as the AI ecosystem market.

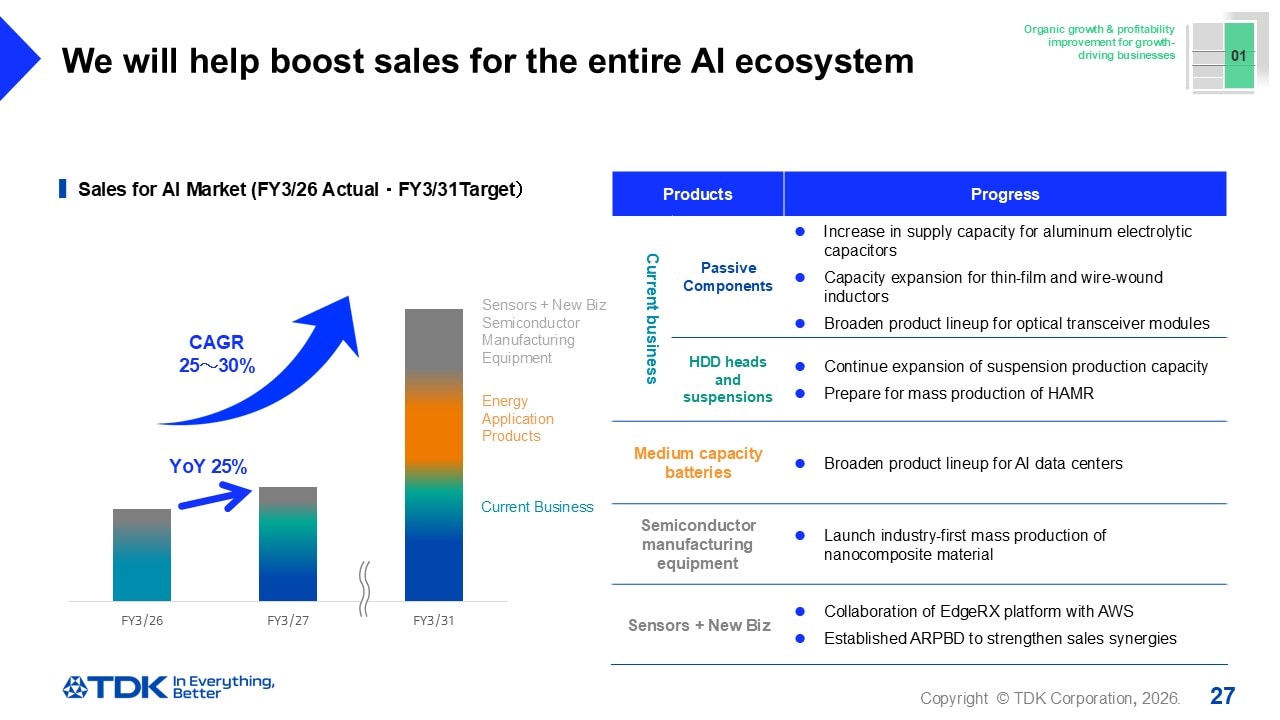

We will help boost sales for the entire AI ecosystem

Here are the actual results and projections for net sales growth in the AI ecosystem market, as explained in the full-year performance briefing in April of last year.

This segment accounted for just over 10% of total company sales last fiscal year, but we expect the segment to grow by 25% year-over-year in the FY March 2027 and be responsible for approximately 15% of total company sales.

Today, I will be providing a more detailed explanation of our existing products (indicated here in blue and green) and our new business ventures (marked here in gray), particularly those related to semiconductor manufacturing equipment.

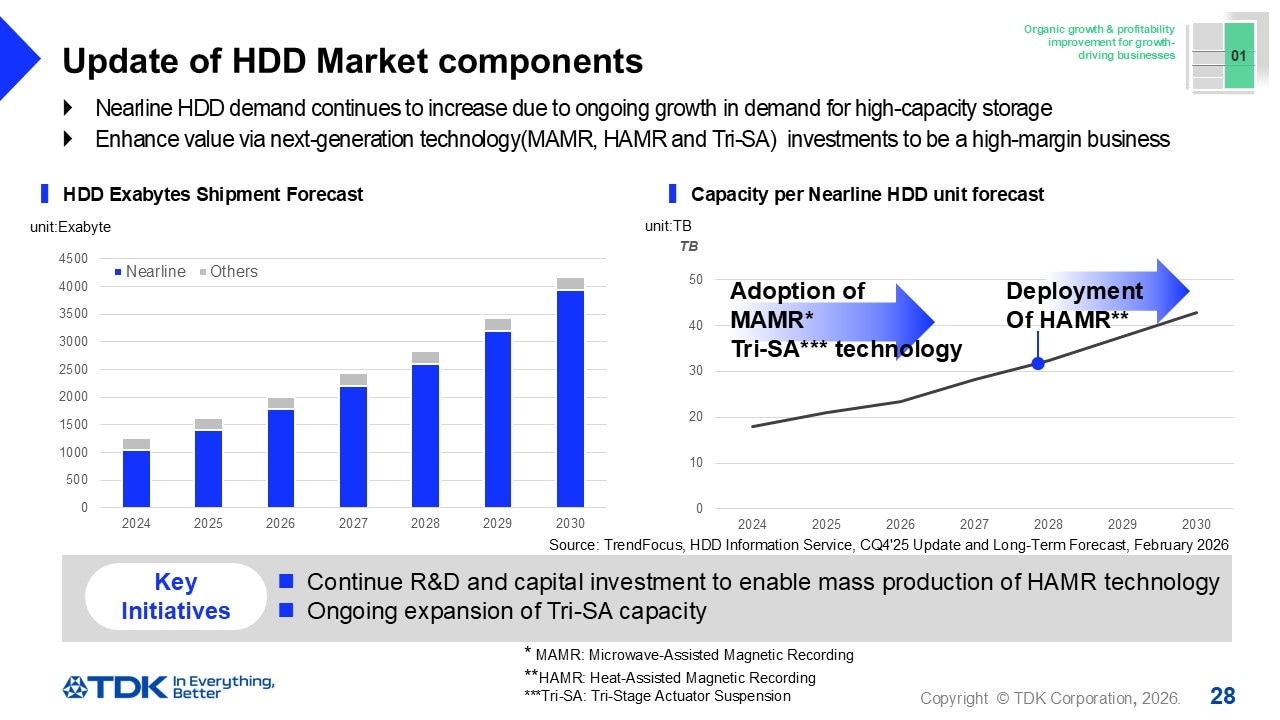

Update of HDD Market components

Among our existing products, let me begin specifically with the HDD heads and suspension assemblies businesses for the HDD market.

Demand for storage capacity in the HDD market is now expected to grow more strongly than initially anticipated. Rather than responding by increasing the number of units produced, HDD manufacturers are seeking to meet this demand by increasing the storage capacity per unit.

This presents a significant business opportunity for us, and our mass production of MAMR heads capable of high-density magnetic recording dates back to 2021.

In two years, we will begin mass production of HAMR heads, further increasing the proportion of high-value-added products and transforming our HDD head business into a highly profitable one.

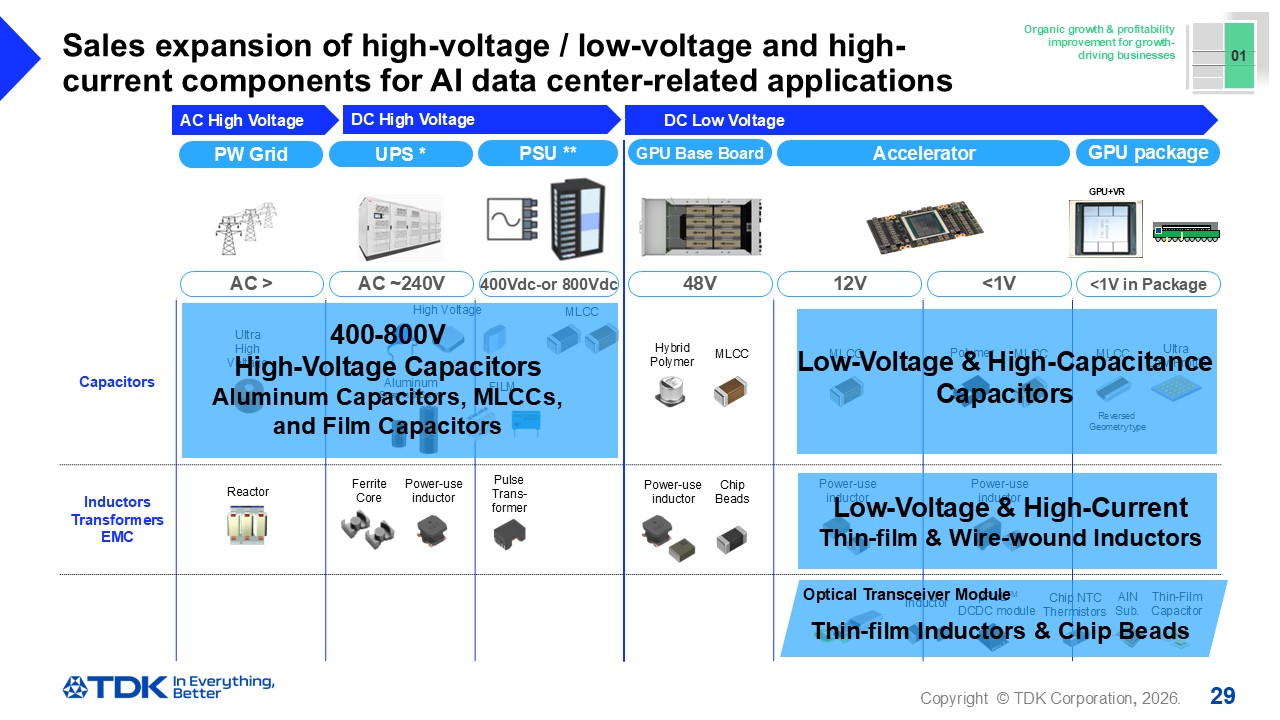

Sales expansion of high-voltage / low-voltage and highcurrent components for AI data center-related applications

Next, we offer a wide range of passive components designed to support the infrastructure of AI data centers.

Power unit voltages in data centers will increase to 400–800V in future. We view this shift toward high voltage as an opportunity for further growth in products where we hold a competitive advantage in the automotive market, especially for xEV applications, such as high-voltage aluminum electrolytic capacitors, MLCCs, and film capacitors. We will be strengthening our capabilities not only in the high-voltage components but in the low-voltage components as well.

We announced the establishment of a joint venture with Nippon Chemical Industrial Co., Ltd. on April 2. Through this joint venture, we hope to accelerate the development of MLCC materials and the development of low-voltage and highcapacity MLCCs used in data centers.

We will be reinforcing our inductor business as well as our capacitor business. The challenges facing the inductor market present an opportunity for us; the overall power consumption of data centers can be reduced by adopting vertical power supply technology for low-voltage and high-current inductors. We offer a variety of inductors, including wire-wound, multilayer, and thin-film type, and we are planning specifically to accelerate capacity expansion for thin-film inductors derived from our thin-film HDD head process technology ahead of our initial schedule to boost this fiscal year’s performance.

Demand for thin-film inductors for optical transceivers and chip beads also remains strong, and these products will begin contributing to sales starting this fiscal year.

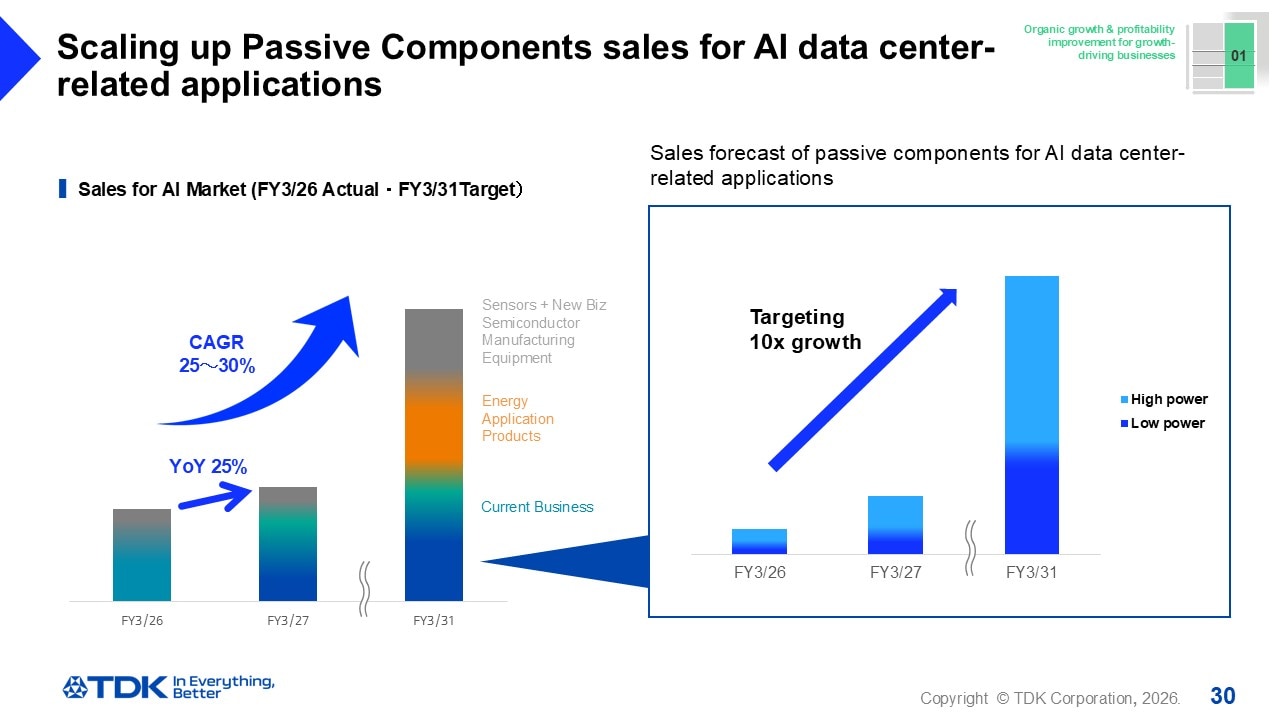

Scaling up Passive Components sales for AI data center-related applications

We plan to increase sales of passive components for AI data center-related applications by approximately tenfold through the initiatives I described earlier.

We will be further refining our competitive advantages in both the high-voltage and low-voltage components domains, and executing a variety of strategies, including aggressive investment, in a timely manner.

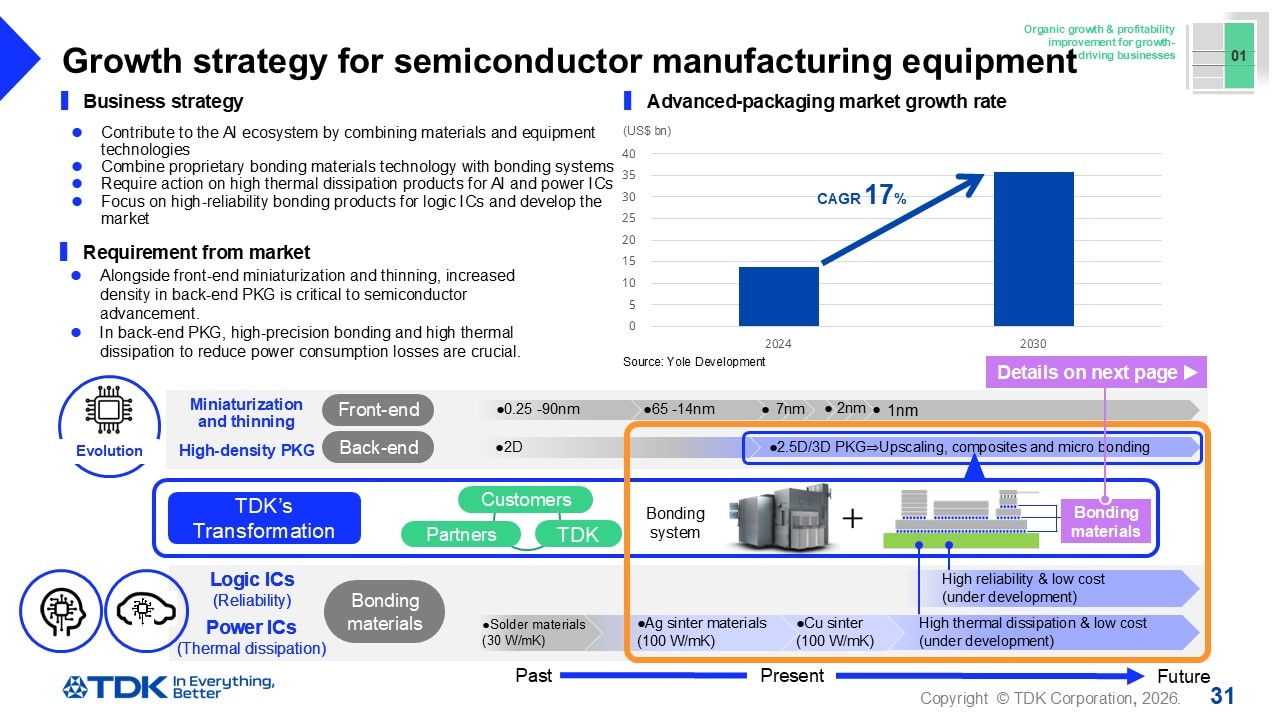

Growth strategy for semiconductor manufacturing equipment

Next, I will discuss the progress of our initiatives in the semiconductor manufacturing equipment business.

This slide was also presented at our Investor Day on November 28.

We sell equipment for semiconductor manufacturing, such as load ports and flip-chip bonders.

Going forward, we plan to supplement our high-density, high-precision mounting technologies by combining high-reliability and high-thermal-dissipation materials to contribute to reduced power consumption, thereby establishing a unique competitive advantage and expanding our business.

Here, I would like in particular to explain the progress made with respect to our semiconductor bonding materials.

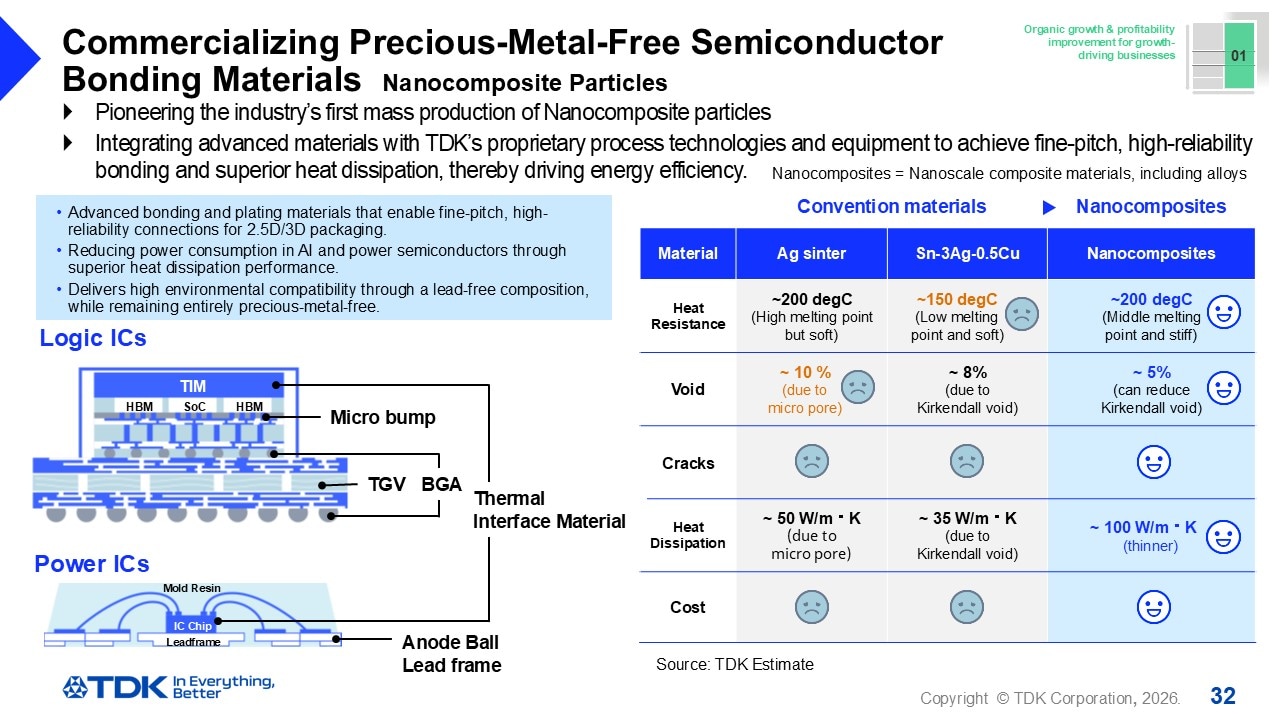

Commercializing Precious-Metal-Free Semiconductor Bonding Materials Nanocomposite Particles

We have acquired material technology from Napra Co., Ltd. relevant to nanocomposite materials used as bonding materials for logic ICs and power ICs, which offer higher thermal conductivity than silver and other precious metals in current use.

As noted on this slide, this material technology has been confirmed to offer numerous benefits, including heat resistance, reliability, and superior heat dissipation properties.

We thus decided to acquire this technology with the aim of being the first in the industry to achieve mass production.

We plan to begin mass production for select customers within the next fiscal year.

Given the advantages outlined above, we have already received numerous inquiries and are simultaneously exploring ways to incorporate this technology into our own product lineup.

This material holds significant potential for reducing power consumption in highdensity packages, and we expect it to find applications in many markets beyond semiconductors.

We intend to expand this materials business in the future through collaboration with our partners and other means, so please look forward to further news.

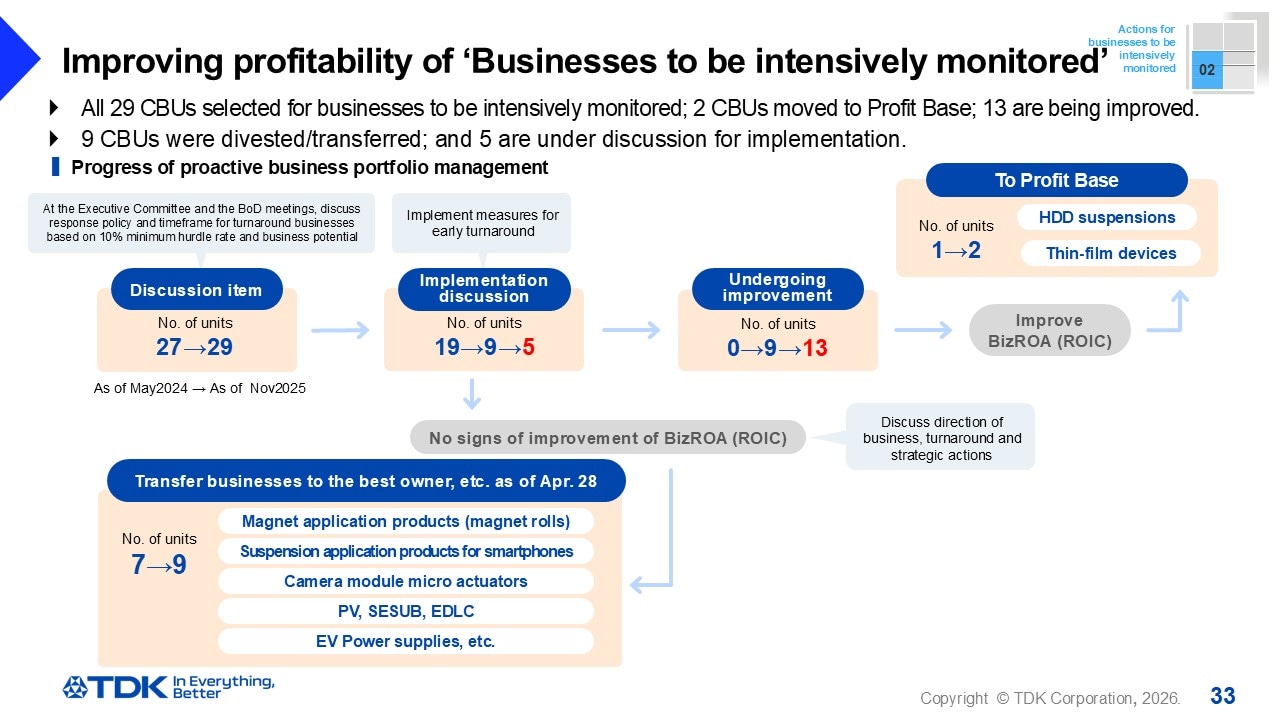

Improving profitability of ‘Businesses to be intensively monitored

I want to go on now to discuss the progress made in business portfolio management, as I explained in our Investor Day in November 2025.

Of our 29 CBUs selected for “businesses to be intensively monitored,” two have been moved to Profit Base. The number of business units currently undergoing improvement, with a path to Profit Base now coming into sight, has increased from nine last time to 13 at present. These are primarily business units dealing with the Passive Components segment.

Regarding the five CBUs currently under discussion, we plan to determine their direction by the end of this fiscal year, which is the final year of the Medium-term Plan.

As pointed out earlier, the cumulative improvement effect for the FY March 2026 to the FY March 2027 is approximately 32 billion yen, and we estimate that the amount under the current Medium-term Plan will reach approximately 90 billion yen.

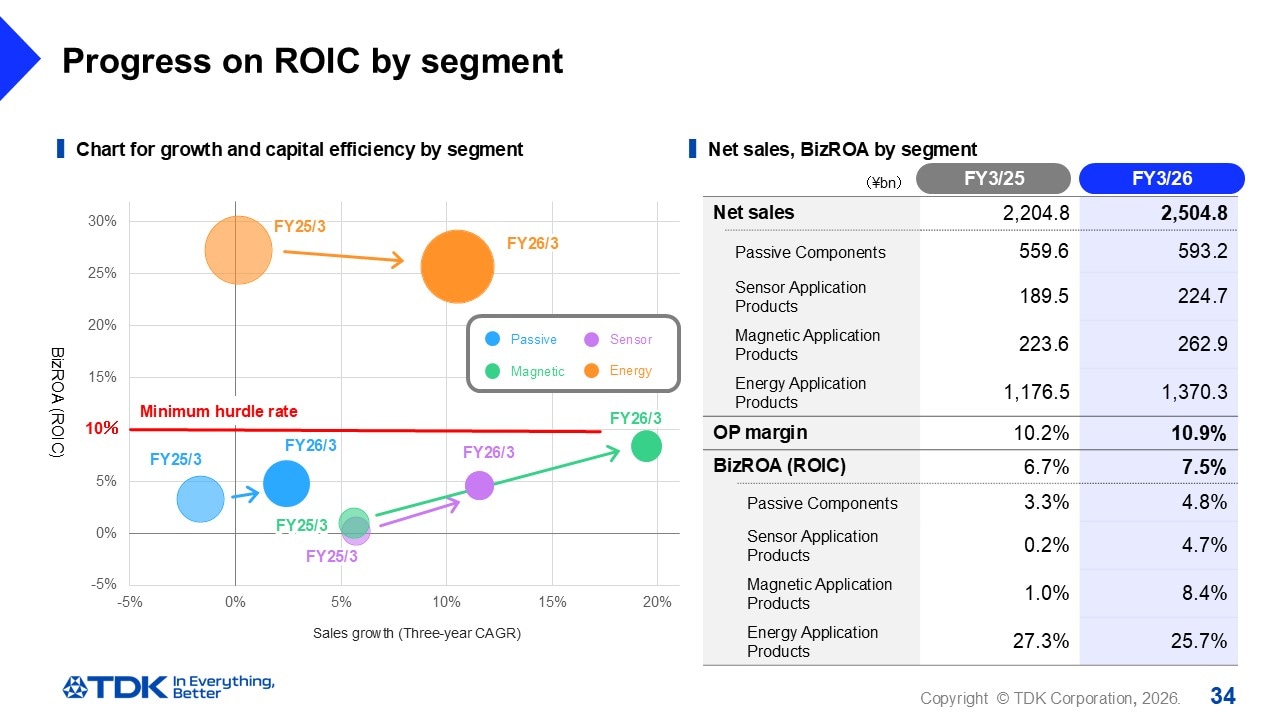

Progress on ROIC by segment

Reflecting the positive outcomes of this business portfolio management approach, ROIC by segment has improved and is still progressing as shown here.

Going forward, we will continue bolstering our business portfolio management strategy with a focus on capital efficiency, aiming to widen the ROIC-WACC spread and increase cash flow.

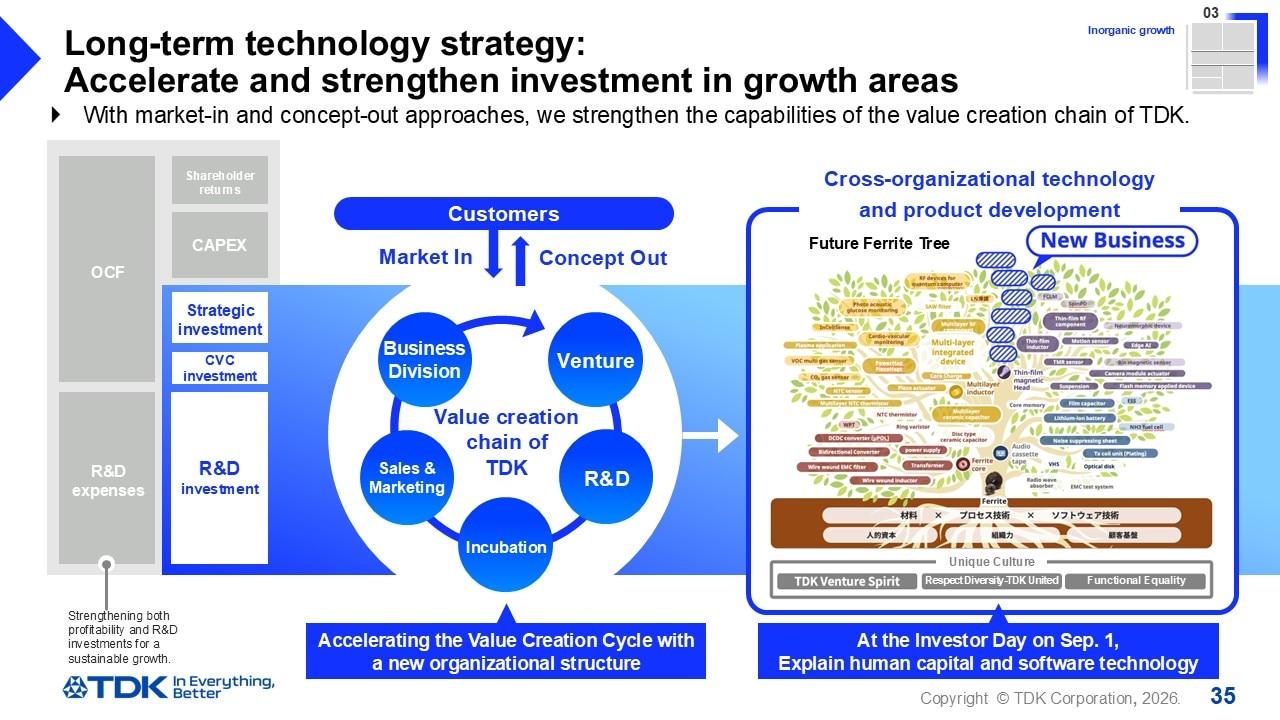

Long-term technology strategy: Accelerate and strengthen investment in growth areas

Finally, I would like to discuss the third pillar of our growth strategy: inorganic growth.

In April 2026, we dissolved the Corporate Marketing & Incubation HQ as part of a strategic realignment, integrated the Passive Components and Sensors sales teams, and established the Sales & Marketing HQ to oversee company-wide sales.

In addition, we will further strengthen our end-to-end new business creation activities by spinning off the Incubation Group and placing it within the R&D Center.

These organizational changes are designed to transform our Value Creation Cycle into an even more agile and efficient one.

On Investor Day in September 2026, we plan to explain our initiatives regarding the root of the Ferrite Tree – namely, our human capital as the pre-financial capital – as well as our software technologies such as SensEI and the AR Platform.

This transformation of our value creation chain will ensure the sustainable growth of our Ferrite Tree.

That concludes my presentation.

Thank you very much for your attention today.