1st Quarter of fiscal 2024 Performance Briefing

1st Quarter Fiscal 2024 Results Highlights

Mr. Tetsuji Yamanishi

Executive Vice President

Hello, I am Tetsuji Yamanishi, Executive Vice President of TDK. Thank you for taking the time to attend TDK’s performance briefing for the first quarter of the fiscal year ended March 2024. I will be presenting an overview of our consolidated results.

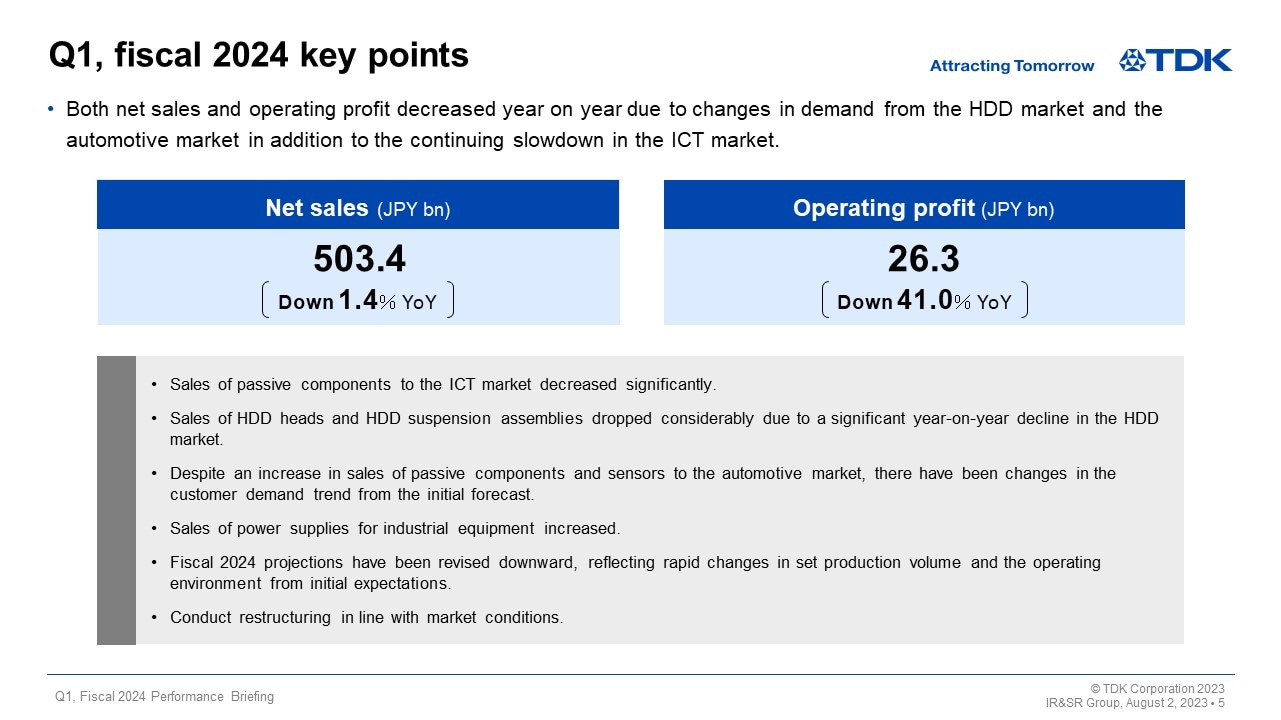

Q1, fiscal 2024 key points

First, let’s take a look at the key points concerning the earnings for the first quarter. Prolonged inflation and continued tight monetary policy in Europe and the United States have slowed the pace of global economic growth, leaving the world economy in a very unstable situation. As for foreign exchange rates, the depreciation of the yen continued especially against the U.S. dollar and the euro.

Under such an operating environment, in the electronics market, which has a large bearing on the consolidated performance of TDK, the prolonged slump in final demand resulted in a slowdown in the ICT market, and there were changes in demand from the HDD market and the automotive market. As a result, net sales were down 1.4% year on year, and operating profit plunged by 41.0% year on year.

In the ICT market, sales of passive components decreased significantly particularly for smartphone applications. Sales of HDD heads and HDD suspension assemblies also dropped considerably due to a 31% year-on-year decline in HDD related demand. In the automotive market, despite an increase in sales of passive components and sensors, sales remained lower than TDK’s initial forecast due to the effect of adjustment of inventories for automotive components by customers. Sales of power supplies for industrial equipment remained firm.

Demand for ICT related devices, which has been sluggish, is expected to further decrease from the second quarter onward compared to the initial forecast. The production volume of HDDs for data centers, in particular, is anticipated to drop sharply. In addition, there have been changes in demand trends related to passive components for the automotive market due to the adjustment of components inventories by some customers among other factors. As a result of a review of the order outlook by taking into account such demand prospects, TDK forecasts that sales of HDD heads, HDD suspension assemblies, and passive components, in particular, will be lower than its initial forecast. Consequently, TDK has revised downward the previous projections announced on April 28.

Meanwhile, on the assumption that it will take a bit longer for HDD demand to pick up, the revised projections reflect restructuring aimed at optimizing production systems for HDD heads and HDD suspension assemblies.

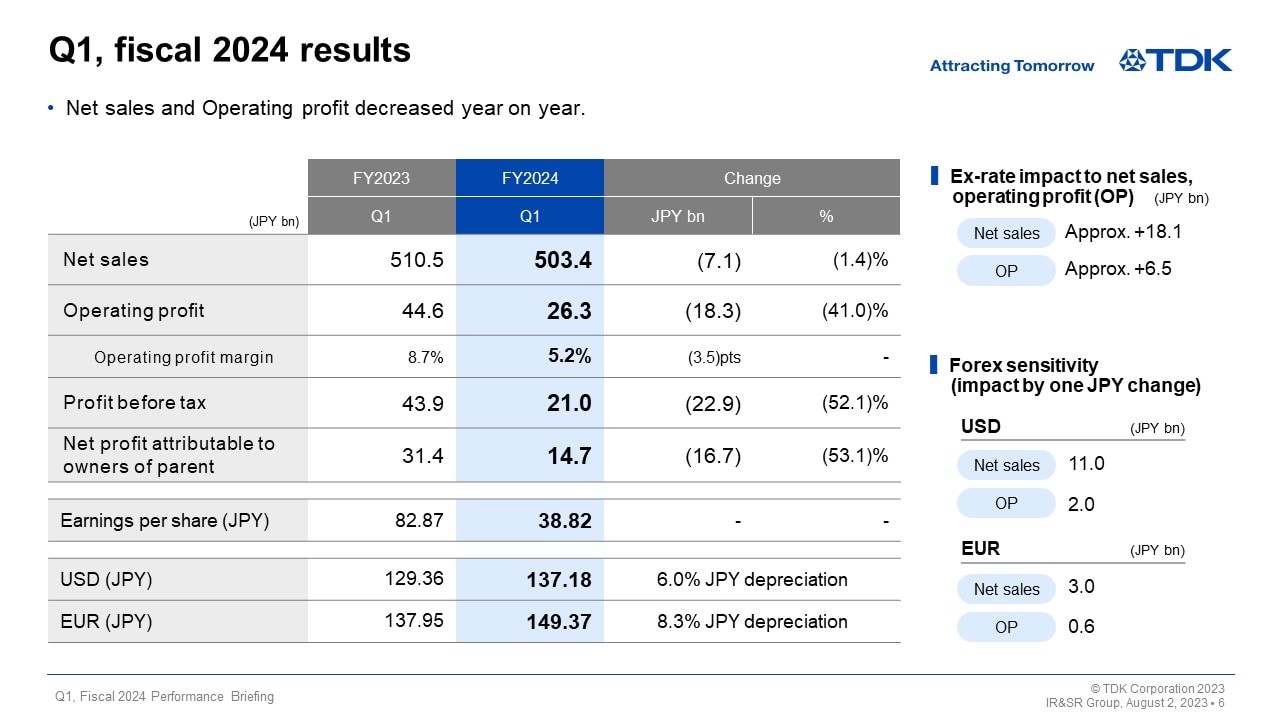

Q1, fiscal 2024 results

Next, I would like to present an overview of our results.

Looking at exchange rate impact on net sales and operating profit, there was an increase of about 18.1 billion yen in net sales and an increase of about 6.5 billion yen in operating profit due to exchange rate fluctuations against the U.S. dollar and other currencies. Including this impact, net sales were 503.4 billion yen, a decrease of 7.1 billion yen, or 1.4%, year on year. Operating profit was 26.3 billion yen, a decrease of 18.3 billion yen, or 41.0%, year on year. Profit before tax was 21.0 billion yen, and net profit was 14.7 billion yen. Earnings per share were 38.82 yen.

With regard to exchange rate sensitivity, we maintain our estimate that a change of 1 yen against the U.S. dollar will affect operating profit by about 2.0 billion yen a year, while a 1 yen change against the euro will have an impact of about 0.6 billion yen a year.

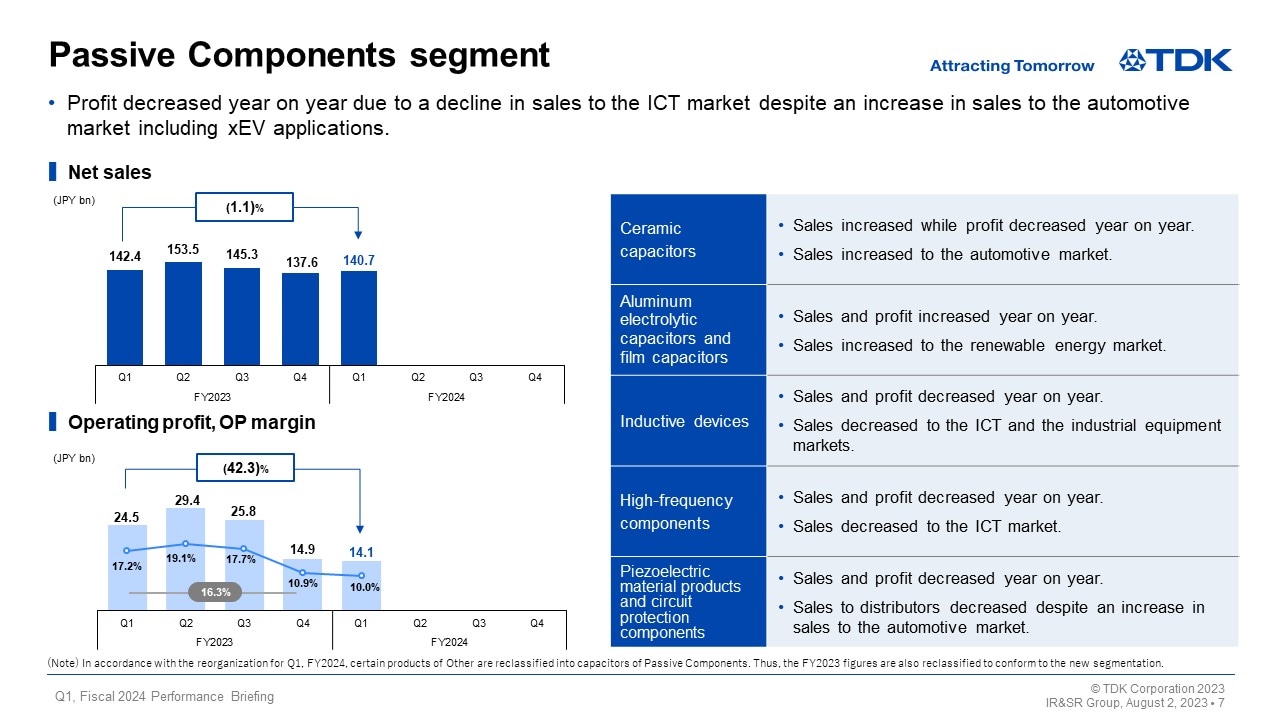

Passive Components segment

Net sales in the Passive Components segment were 140.7 billion yen, a decrease of 1.1% year on year. Operating profit was down 42.3% year on year due to a decline in sales to the ICT market despite an increase in sales to the automotive market, especially those related to xEVs.

Sales and profit of aluminum electrolytic capacitors and film capacitors, with robust sales to the automotive and renewable energy markets, increased year on year. While sales of ceramic capacitors increased to the automotive market, profit decreased slightly on a year-on-year basis due to a decline in the sales volume to distributors, among other factors. Sales and profit of high frequency components, which have a high ratio of sales for smartphone applications, decreased year on year. Sales and profit of inductive devices and piezoelectric material products and circuit protection components decreased year on year due to a decline in sales to the ICT and industrial equipment markets as well as to distributors, despite an increase in sales to the automotive market.

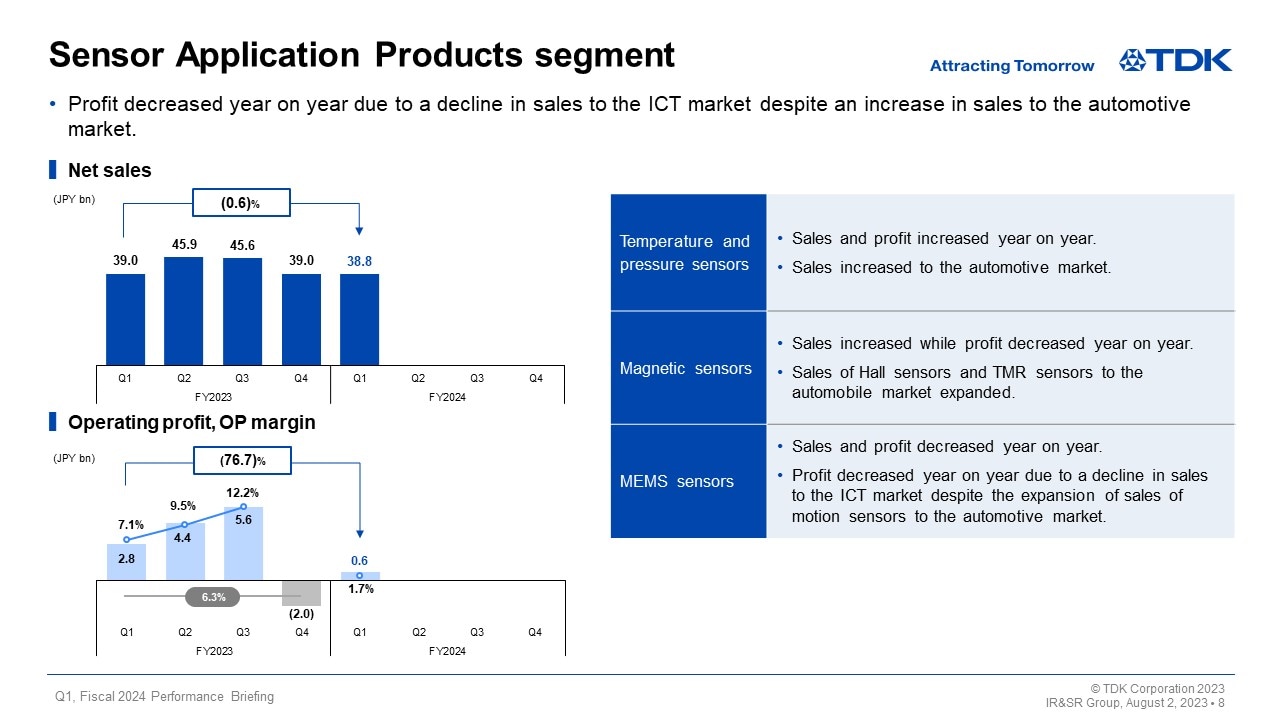

Sensor Application Products segment

Net sales in the Sensor Application Products segment amounted to 38.8 billion yen, virtually unchanged from the same period of the previous fiscal year. Operating profit was 0.6 billion yen, down 76.7% year on year.

Sales of temperature and pressure sensors increased year on year reflecting a rise in sales to the automotive market. In magnetic sensors, while sales increased year on year as sales of Hall sensors and TMR sensors increased to the automotive market and those for smartphone applications remained at the virtually same level as in the same period of the previous fiscal year, profit decreased slightly year on year due to the recording of fixed expenses related to advanced investment aimed at increasing production. Sales and profit of MEMS sensors decreased year on year due to a drop in sales to the ICT market, despite an expansion of sales of motion sensors to the automotive market.

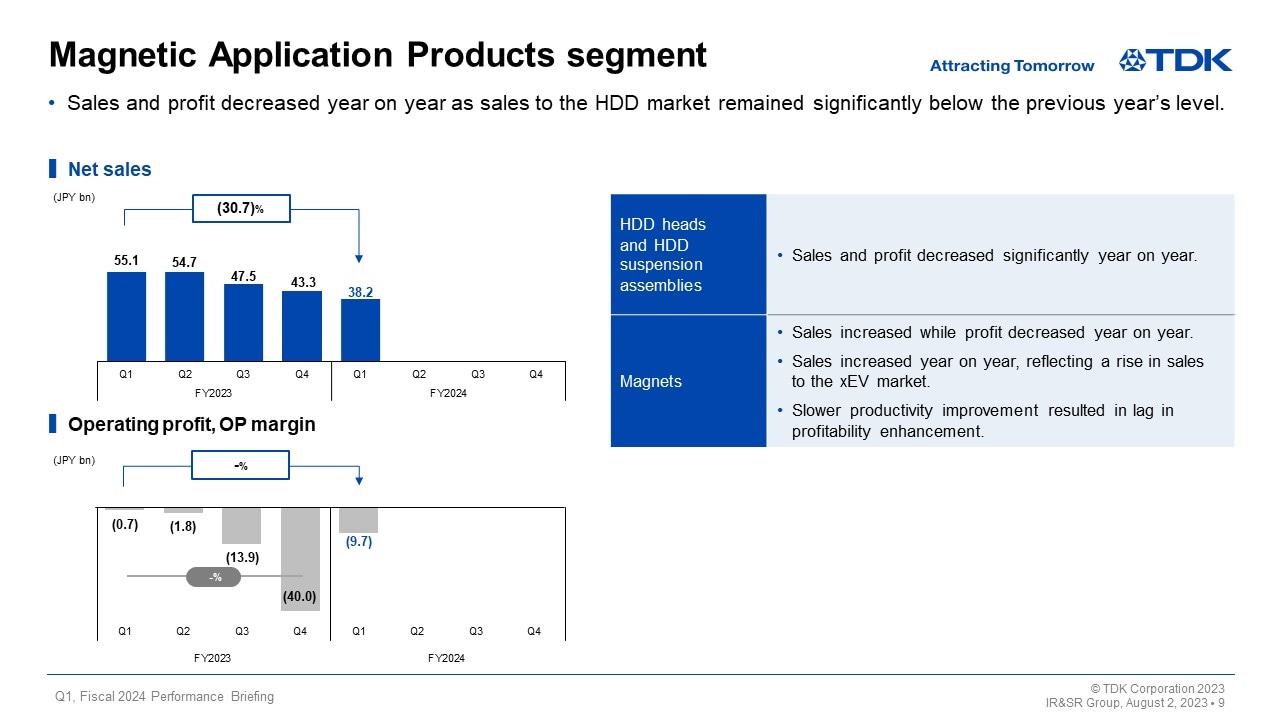

Magnetic Application Products segment

In the Magnetic Application Products segment, net sales plunged 30.7% year on year to 38.2 billion yen, and a significant operating loss of 9.7 billion yen was posted.

Sales of HDD heads and HDD suspension assemblies declined significantly compared to the same period of the previous fiscal year, posting a loss. This is attributable to a substantial decrease in the sales volume of both HDD heads and HDD suspension assemblies as a result of a drop in data center investment due to the effect of economic slowdown which affected demand related to nearline HDD heads, as well as a 31% year-on-year decline in total demand for HDDs owning to protracted HDD inventory adjustment.

While sales of magnets increased year on year reflecting a rise in sales related to xEVs, slower productivity improvement resulted in a lag in profitability enhancement.

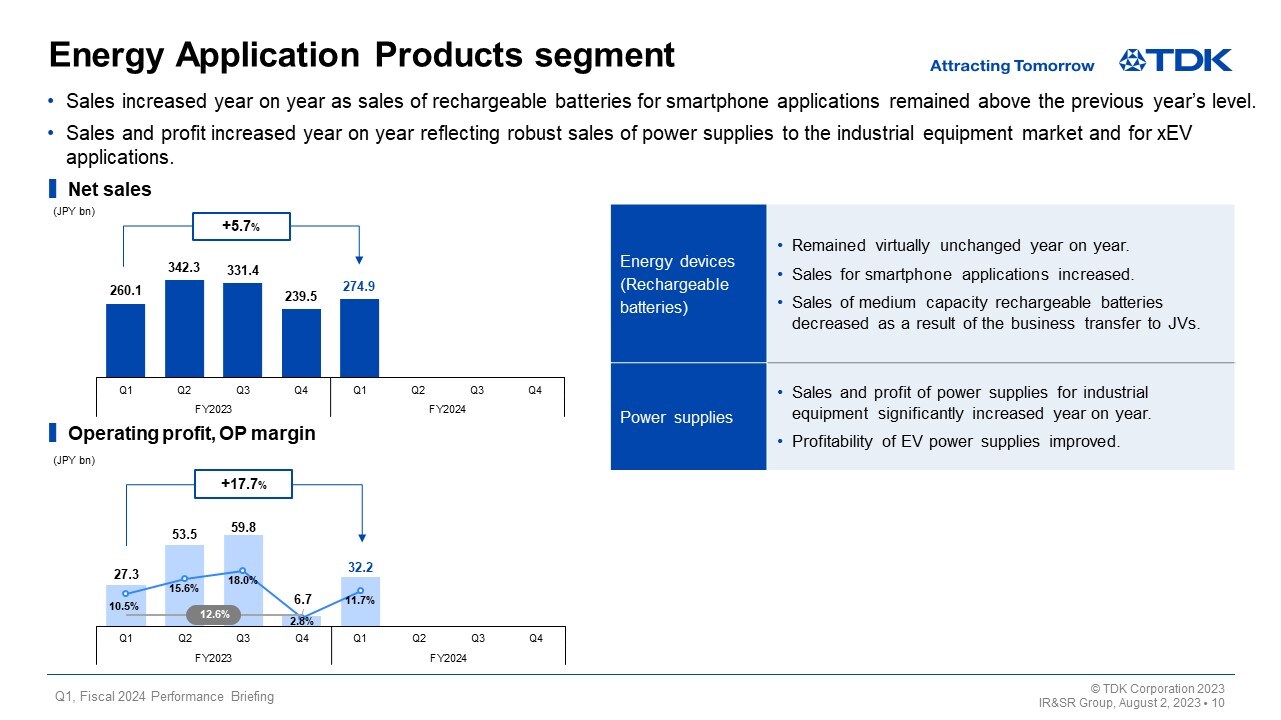

Energy Application Products segment

In the Energy Application Products segment, net sales increased 5.7% year on year to 274.9 billion yen and operating profit rose 17.7% year on year to 32.2 billion yen.

In energy devices (rechargeable batteries), sales and profit remained virtually unchanged on the whole from the same period of the previous fiscal year due to a decline in sales of medium capacity rechargeable batteries as a result of the business transfer to JVs, despite an increase in sales of small capacity rechargeable batteries for smartphone applications.

In power supplies for industrial equipment, demand related to industrial equipment, such as semiconductor manufacturing equipment, as well as medical equipment applications remained robust, resulting in year-on-year increases in both sales and profit. Profitability also improved considerably. Sales of EV power supplies grew year on year and profitability has been improving reflecting the benefits from restructuring at the end of the previous fiscal year among other factors.

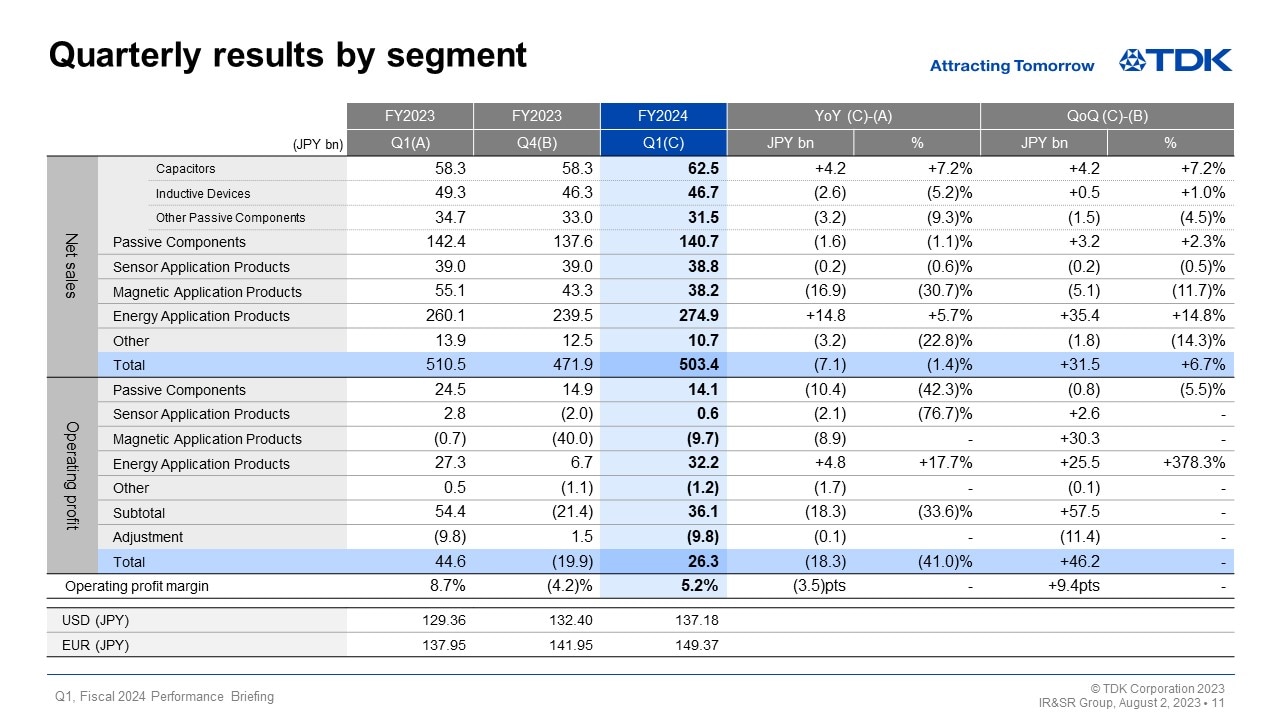

Quarterly results by segment

Now, I will explain some of the factors behind the changes in segment net sales and operating profit from the fourth quarter of the fiscal year ended March 2023 to the first quarter of the fiscal year ending March 2024.

First, in the Passive Components segment, net sales increased by 3.2 billion yen, or 2.3%, from the fourth quarter of the previous fiscal year, and operating profit dropped by 0.8 billion yen, or 5.5%, from the fourth quarter. While sales of ceramic capacitors increased to the automotive market and sales of aluminum electrolytic capacitors and film capacitors rose to the industrial equipment market including those to the renewable energy market, other sales decreased from the fourth quarter on an actual basis, excluding the effect of fluctuations in foreign exchange rates. As a result, segment profit decreased on the whole from the fourth quarter.

In the Sensor Application Products segment, net sales decreased slightly by 0.2 billion yen from the fourth quarter, while operating profit increased slightly from the fourth quarter, when excluding the effect of one-time expenses of 2.5 billion yen recorded during the fourth quarter of the fiscal year ended March 2023. Sales and profit of temperature and pressure sensors increased from the fourth quarter thanks to an increase in sales to the automotive market.

Sales of magnetic sensors remained virtually unchanged from the fourth quarter and profit increased slightly from the fourth quarter reflecting an increase in sales to the automotive market, despite a drop in sales related to smartphone applications. Both sales and profit of MEMS sensors decreased from the fourth quarter due to sluggish sales to the ICT market, despite an increase in sales to the automotive market.

In the Magnetic Application Products segment, net sales decreased by 5.1 billion yen, or 11.7%, from the fourth quarter, while operating profit increased by 3.7 billion yen from the fourth quarter on an actual basis, when excluding the effect of one-time expenses of 26.9 billion yen recorded during the fourth quarter of the fiscal year ended March 2023. The sales volume of HDD heads decreased 35% from the fourth quarter of the fiscal year ended March 2023 due mainly to a further decline in total demand for nearline HDDs, and the sales volume of HDD suspension assemblies also decreased from the fourth quarter, resulting in a substantial drop in sales of HDD heads on the whole. In terms of operating profit, profitability improved as a result of the benefits from restructuring and cost reduction efforts, despite a loss being posted. The profitability of magnets also improved while sales decreased slightly from the fourth quarter.

In the Energy Application Products segment, net sales increased by 35.4 billion yen, or 14.8%, from the fourth quarter, and operating profit rose 6.0 billion yen from the fourth quarter on an actual basis, when excluding the effect of one-time expenses of 17.0 billion yen recorded during the fourth quarter of the fiscal year ended March 2023. Both sales and profit of rechargeable batteries increased on the whole from the fourth quarter as sales of small capacity rechargeable batteries increased to the ICT market, despite a decline in sales of medium capacity rechargeable batteries as a result of the business transfer to JVs. Sales of power supplies for industrial equipment rose, resulting in quarter-on-quarter increases in both sales and profit. Sales of EV power supplies increased from the fourth quarter and profitability improved due partly to the benefits from restructuring.

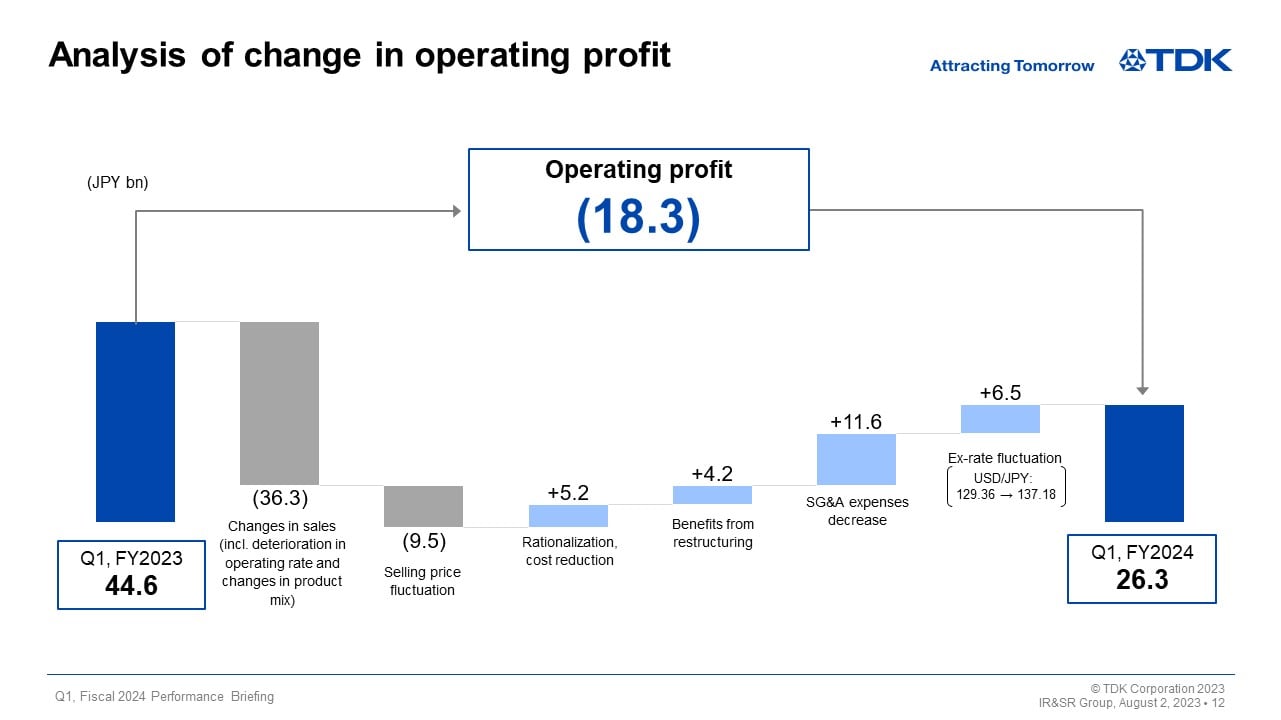

Analysis of change in operating profit

Next is an analysis of changes in operating profit. Let’s take a look at the main factors behind the 18.3 billion yen year-on-year decrease in operating profit. First, operating profit decreased 36.3 billion yen due to changes in sales, reflecting a decline in the sales volume of HDD heads, HDD suspension assemblies and passive components. There was also a decrease in profit of 9.5 billion yen due to selling price fluctuations. On the other hand, there were positive effects on operating profit including the yen’s depreciation amounting to 6.5 billion yen, rationalization and cost reduction efforts mainly for rechargeable batteries and passive components amounting to 5.2 billion yen, benefits from restructuring during the previous fiscal year of 4.2 billion yen, and streamlining of SG&A expenses of 11.6 billion yen. However, these positive effects were not enough to offset the negative impact of the decrease in sales volume.

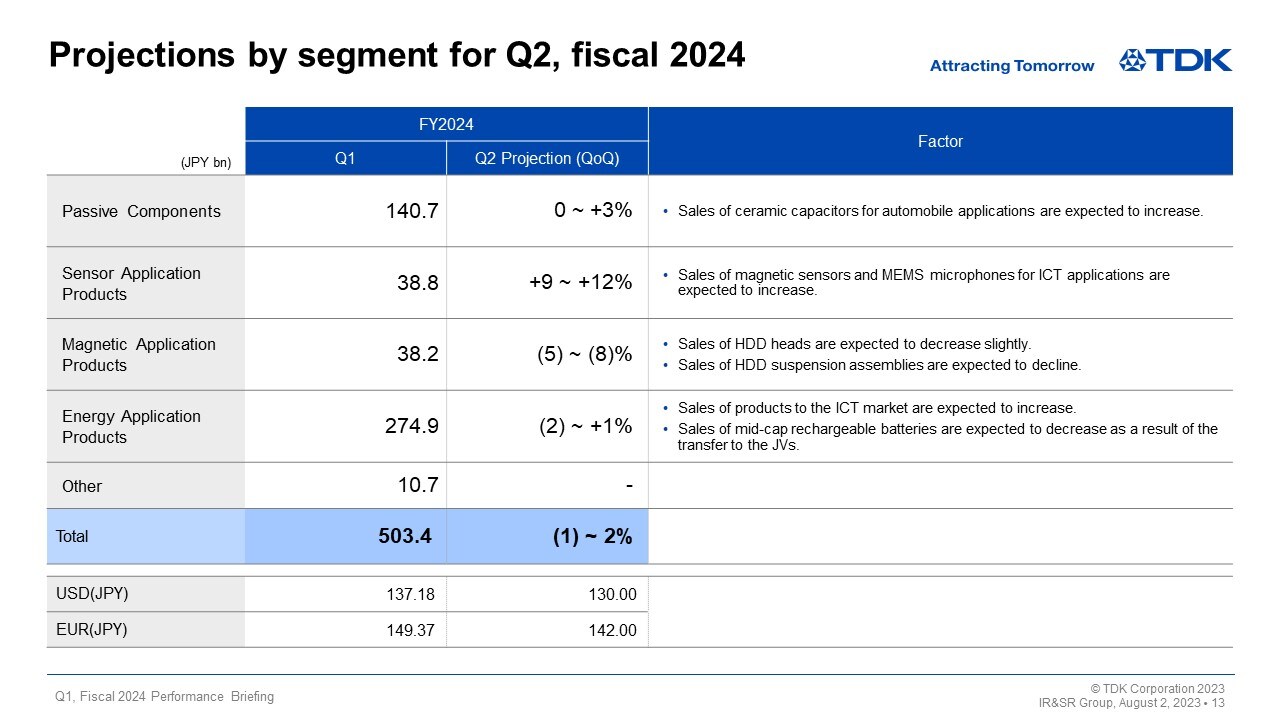

Projections by segment for Q2, fiscal 2024

I would now like to discuss our projection regarding changes in net sales for the second quarter of the fiscal year ending March 2024.

In the Passive Components segment, we are projecting that net sales will increase by 0-3% from the first quarter on the whole due mainly to an increase in sales of ceramic capacitors for automotive applications.

In the Sensor Application Products segment, we are projecting that net sales will increase by 9-12% from the first quarter reflecting a rise in sales of magnetic sensors and MEMS microphones for ICT applications in addition to robust sales to the automotive market.

In the Magnetic Application Products segment, we are projecting that net sales will decrease by 5-8% from the first quarter on the whole as sales of HDD heads are expected to decline slightly due to exchange rate fluctuations, despite an increase in sales volume by about 20%, and the sales volume of HDD suspension assemblies is expected to drop by about 14%.

In the Energy Application Products segment, we are projecting that net sales will remain in a range between -2% and +1% compared with the first quarter on the whole due to the transfer of medium capacity rechargeable batteries to JVs, despite an increase in sales volume of small capacity rechargeable batteries as a result of the launch of new smartphone models.

In light of the above, we are projecting that overall net sales will be within a range between -1% and +2% (increase by 3-6% excluding the negative effect of exchange rate fluctuations on sales) in the second quarter compared to the first quarter.

That concludes my presentation. Thank you very much for your attention.

Fiscal 2024 Projections

Noboru Saito

President & CEO

Hello, I am Noboru Saito, President and CEO of TDK. Thank you for joining us today. I would like to go over our full year projections for the fiscal year ending March 2024.

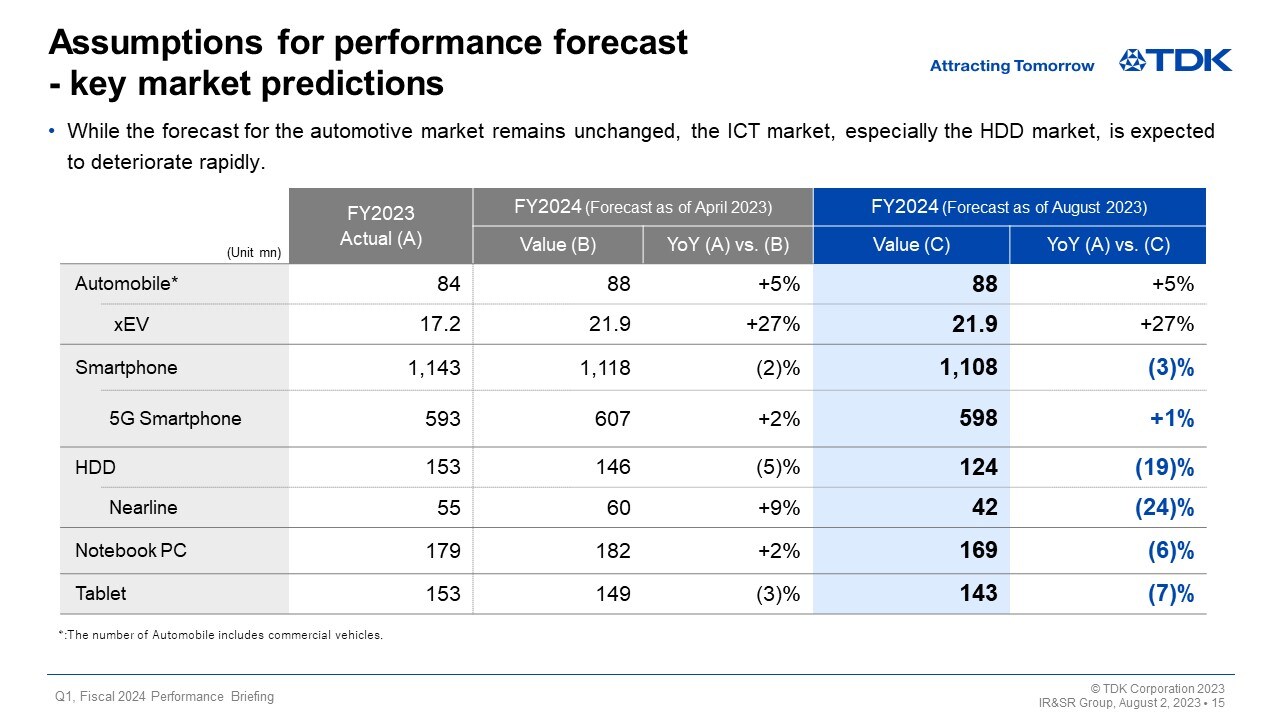

Assumptions for performance forecast - key market predictions

First, as for the assumptions for the performance forecast, I will talk about the revision of key market predictions.

We have not revised our predictions for the production volume in the automotive market from the initial forecast as the semiconductor shortage and other issues are on the way to being resolved and the production volume of xEVs has been robust. However, we predict that demand for passive components and sensors in the automotive market will be lower than our initial forecast as components inventory adjustments by some customers and other developments are expected to become more pronounced.

Meanwhile, we have revised downward our prediction for the production volume of smartphones, which represents the ICT market, from the initial forecast of 1,118 million units to 1,108 million units due to the uncertain macroeconomic environment and longer consumer replacement cycle, among other factors. We have also revised downward our prediction for the production volume of 5G smartphones from the initial forecast of 607 million units to 598 million units.

In the HDD market, we have assumed that the environment surrounding data center investment will change rapidly and that HDD inventory liquidation by customers will take longer than the initial forecast. Due to such factors, the production volume of nearline HDDs for data centers, which had been predicted to increase 9% year on year to 60 million units in the initial forecast, has turned out to be significantly lower than the initial forecast. Therefore, we have revised our prediction to 42 million units, down 19% year on year. We have also revised downward our prediction for the production volume of notebook PCs and tablets from the initial forecast.

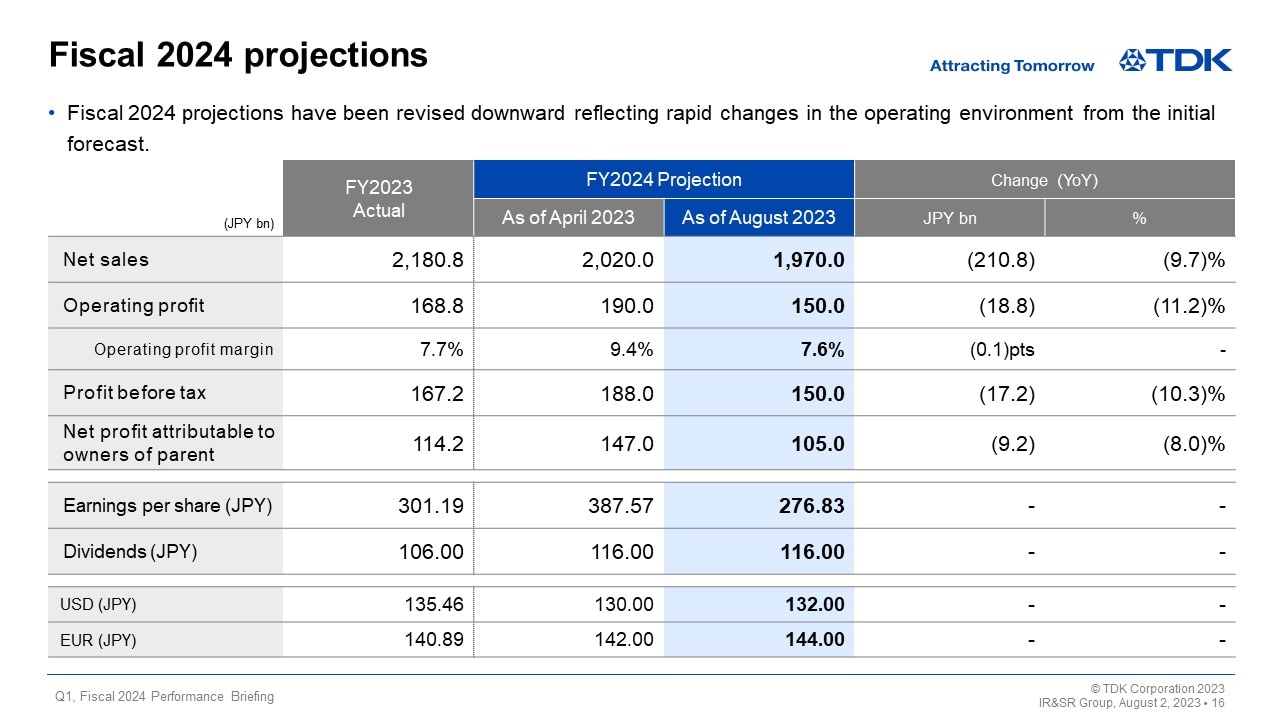

Fiscal 2024 projections

Under such circumstances, our projections for the fiscal year ending March 2024 have been revised from the initial forecast to net sales of 1,970.0 billion yen, operating profit of 150.0 billion yen, and net profit attributable to owners of parent of 105.0 billion yen.

We have kept our initial dividend forecast unchanged.

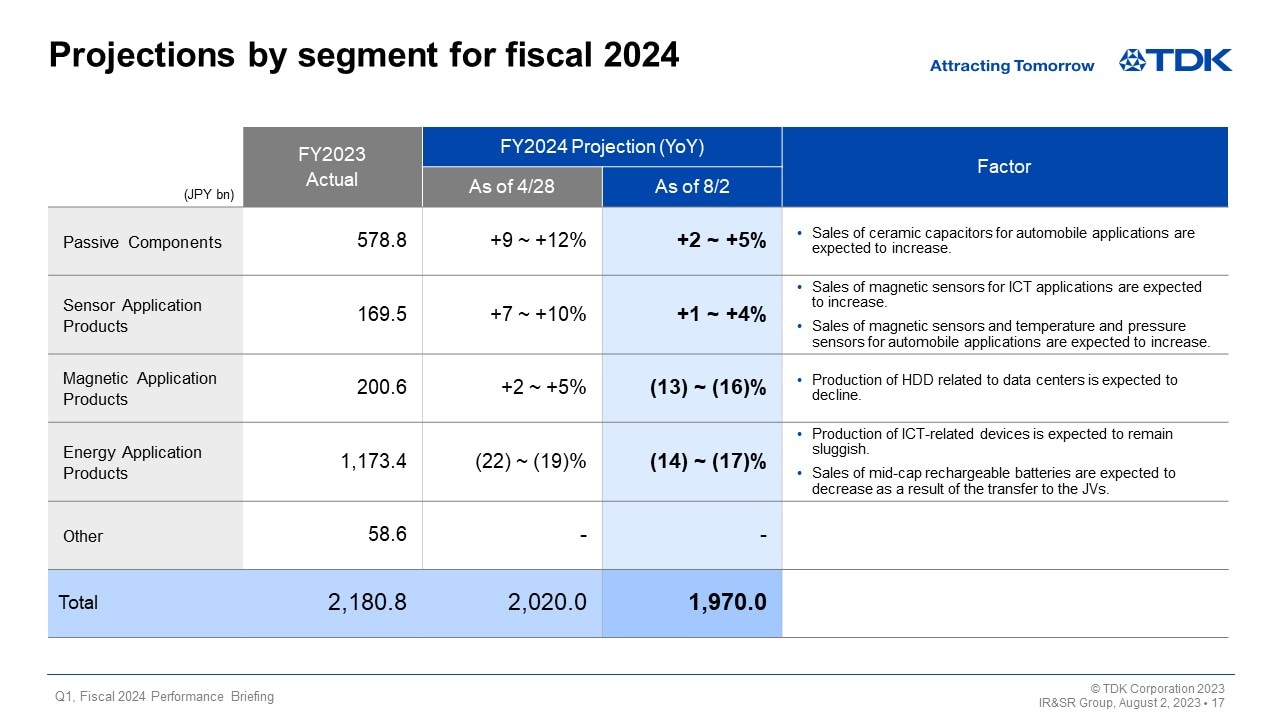

Projections by segment for fiscal 2024

Now, I would like to discuss our projection regarding changes in net sales by segment for the fiscal year ending March 2024.

In the Passive Components segment, while sales of ceramic capacitors and other products are expected to increase to the automotive market, mainly those related to xEVs, sales to the ICT and industrial equipment markets as well as to distributors are expected to be lower than the initial forecast. As a result, the segment sales are forecast to grow by 2-5% overall on a year-on-year basis.

In the Sensor Application Products segment, while sales of magnetic sensors and temperature and pressure sensors are expected to increase to the automotive market, the growth in sales of MEMS motion sensors and microphone to the ICT market is expected to remain lower than the initial forecast. As a result, the segment sales are forecast to grow by 1-4% overall on a year-on-year basis.

In the Magnetic Application Products segment, the production volume of nearline HDDs to data centers is expected to remain significantly lower than the initial forecast, resulting in a substantial decline in sales of HDD heads and HDD suspension assemblies compared to the initial forecast. As a result, the segment sales are forecast to decrease by 13-16% overall on a year-on-year basis.

In the Energy Application Products segment, sales of medium capacity rechargeable batteries are expected to be lower than the initial forecast as the transfer of the medium capacity rechargeable battery business to JVs has been progressing faster than the initial plan. On the other hand, sales of small capacity rechargeable batteries are expected to remain above the initial forecast due mainly to an increase in market share. As a result, the segment sales are forecast to decrease by 14-17% overall on a year-on-year basis.

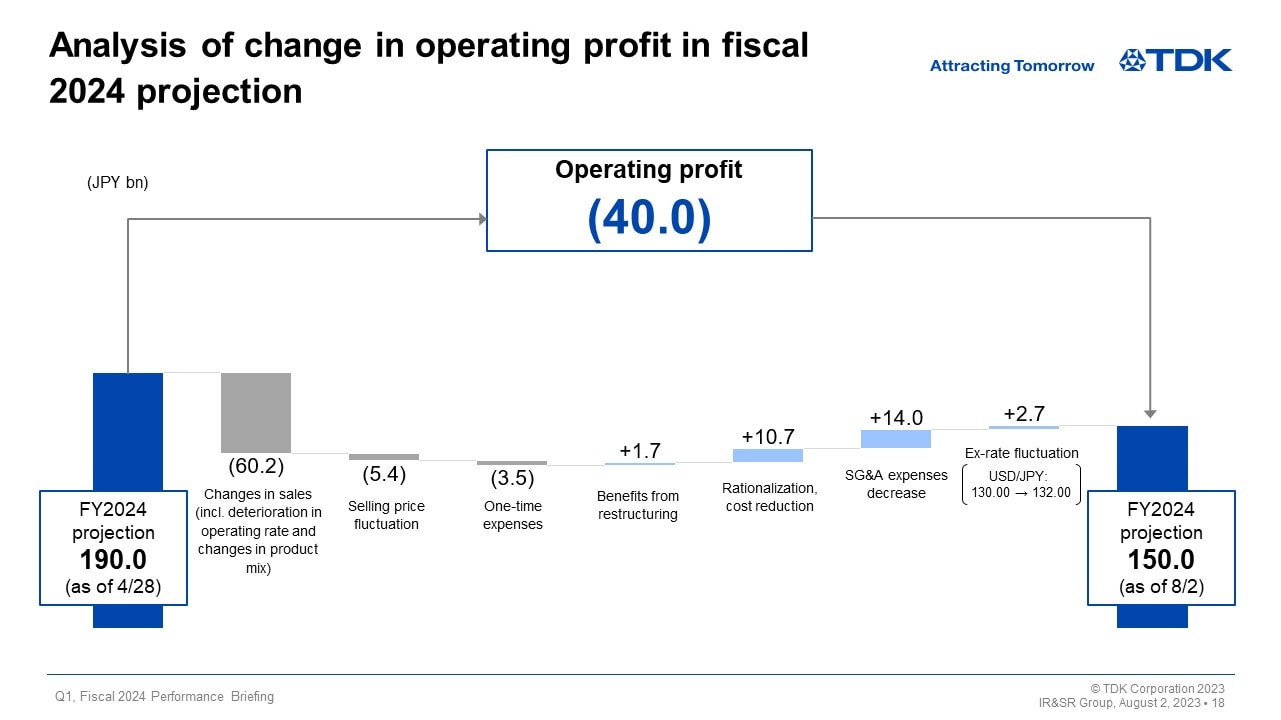

Analysis of change in operating profit in fiscal 2024 projection

Next is an analysis of changes in the operating profit forecast for the fiscal year ending March 2024. Let’s take a look at the main factors behind the 40.0 billion yen year-on-year decrease in operating profit forecast from the previous forecast of 190.0 billion yen announced on April 28. Operating profit is expected to decrease by 60.2 billion yen due to changes in sales, including a decline in sales of passive components and other products in addition to a decrease in the sales volume of HDD heads and HDD suspension assemblies. On the other hand, operating profit is expected to increase by 1.7 billion yen due to benefits from restructuring as a result of one-time expenses of 3.5 billion yen which will be recorded as part of restructuring expenses for HDD heads and HDD suspension assemblies. Other positive effects on operating profit will include the effects of rationalization and cost reduction efforts amounting to 10.7 billion yen and the reduction of SG&A expenses including R&D expenses amounting to 14.0 billion yen.

As for exchange rate impact on operating profit, we expect that profit will be boosted by 2.7 billion yen based on our exchange rate assumptions for the second quarter and thereafter of 130 yen against the U.S. dollar and 142 yen against the euro (the average exchange rate assumptions on a full-year basis are 132 yen against the U.S. dollar and 144 yen against the euro) in light of the exchange rate fluctuations in the first quarter.

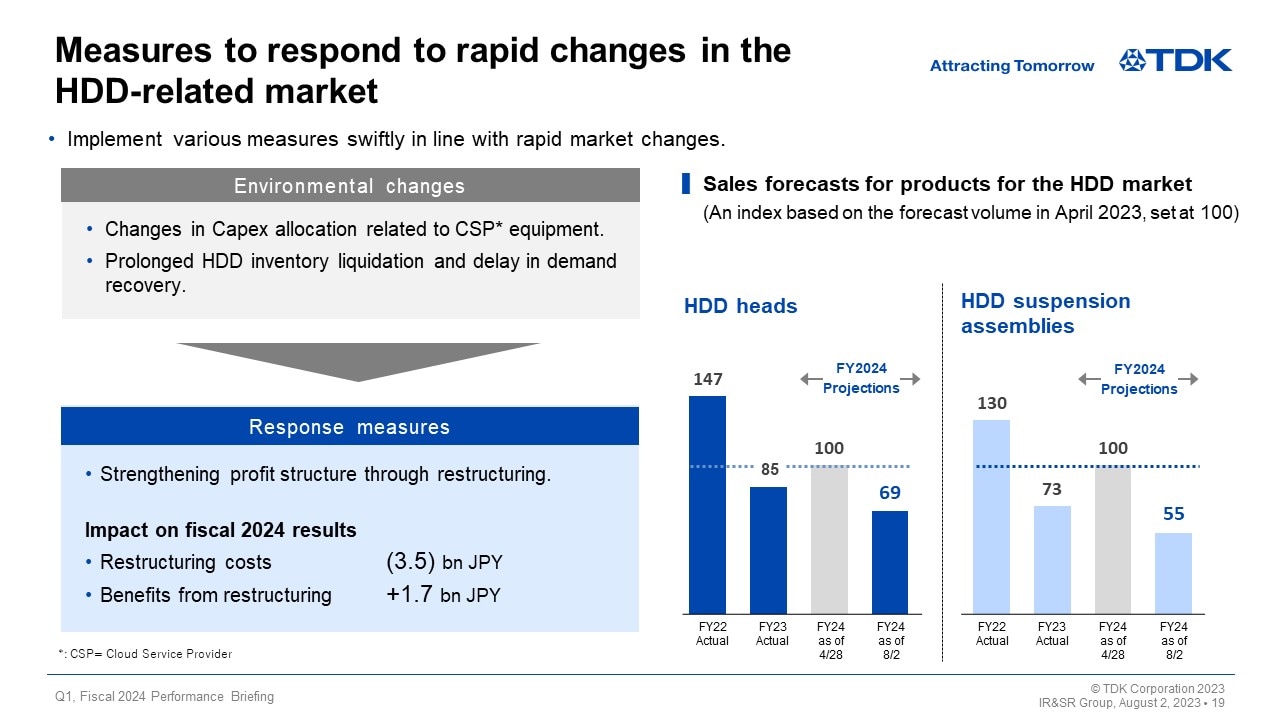

Measures to respond to rapid changes in the HDD-related market

Now, I would like to talk about our measures to respond to rapid changes in the HDD market.

While there has been a prominent increase in AI-related Capex allocation to Cloud Service Provider (CSP) equipment since April, the storage usage rate has also been rising due to a longer replacement cycle for general-purpose servers and storage systems. In addition, prolonged HDD inventory liquidation has resulted in a substantial decline in the sales volume of HDDs. Consequently, demand for HDD heads and HDD suspension assemblies turned out to be significantly lower than the initial forecast.

In line with such rapid changes in the market environment, we will take measures to rebuild the profit structure. Specifically, we will endeavor to cut fixed expenses through personnel reduction and consolidation of business bases in order to build a structure to achieve a break-even point based on the latest demand level for the second half of the current fiscal year.

In tandem with this, we will record restructuring costs of 3.5 billion for the current fiscal year, which is expected to generate benefits from restructuring amounting to 1.7 billion yen for the current fiscal year.

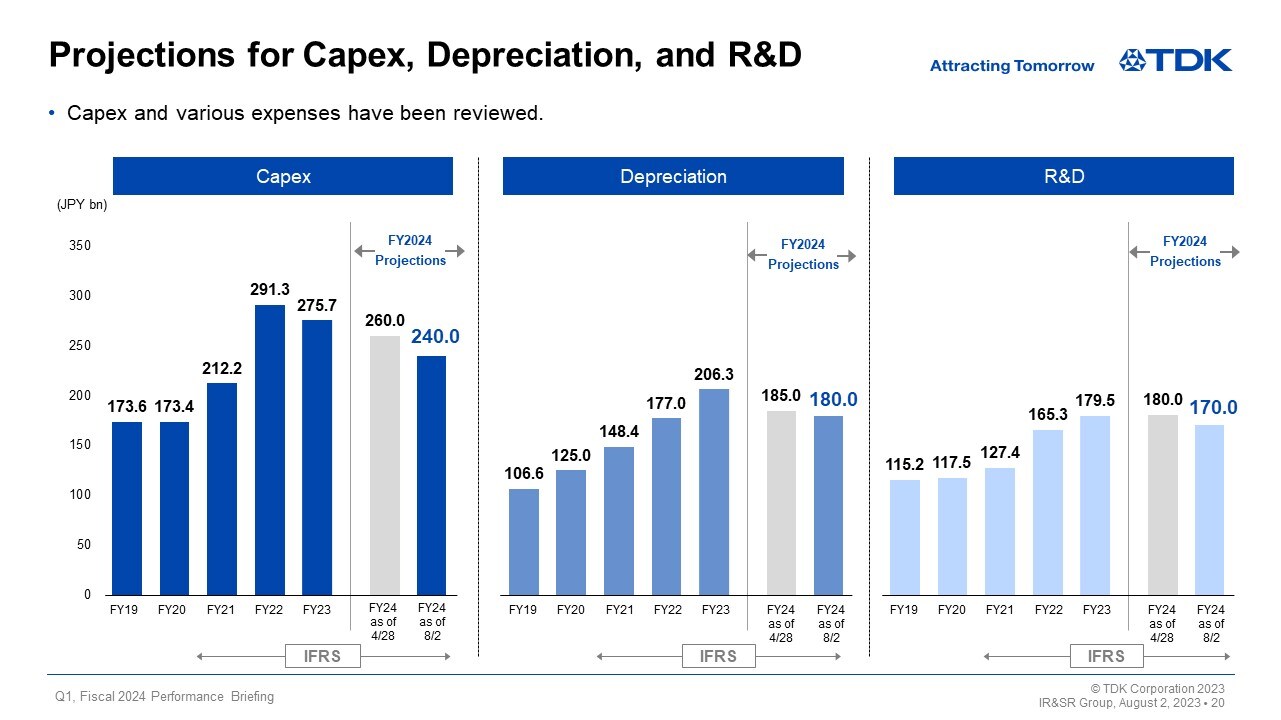

Projections for Capex, Depreciation, and R&D

We have reviewed our projections for Capex, depreciation and R&D expenses in line with changes in the operating environment. We have revised downward our projections for Capex from 260.0 billion yen to 240.0 billion yen, depreciation from 185.0 billion yen to 180.0 billion yen, and R&D expenses from 180.0 billion yen to 170.0 billion yen.

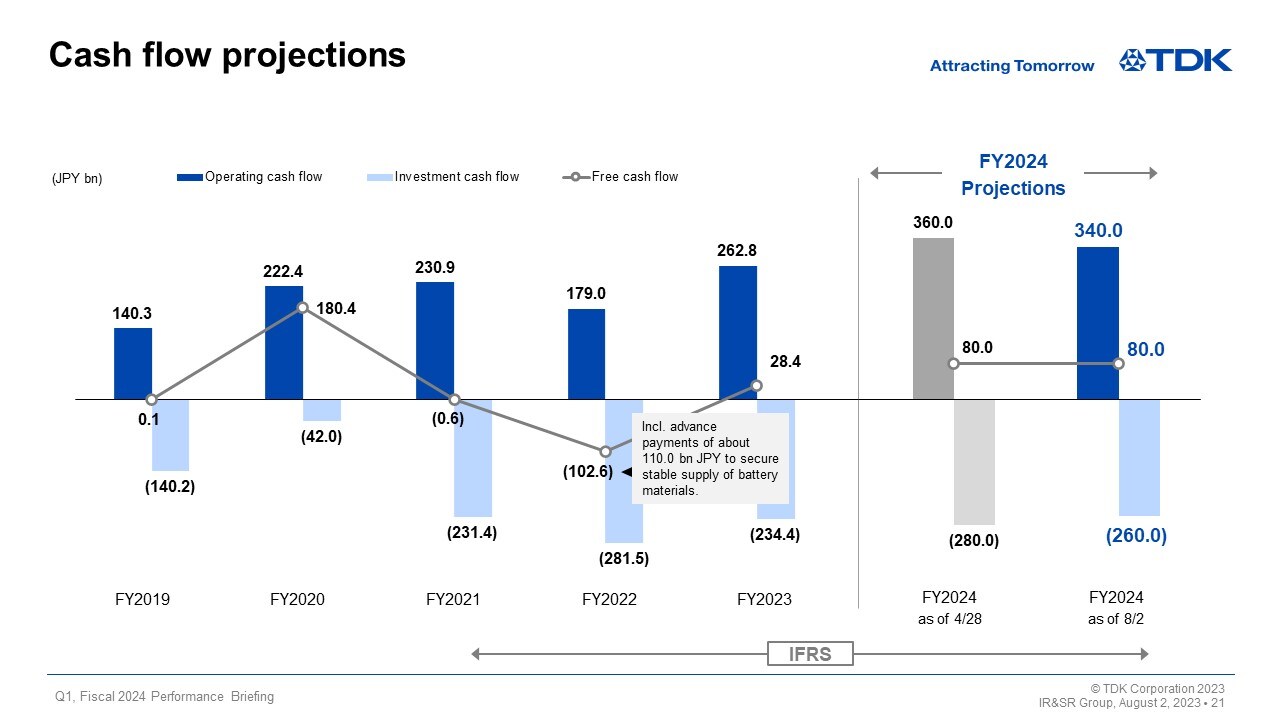

Cash flow projections

Lastly, I would like to talk about our cash flow projections.

We expect to achieve free cash flow of 80.0 billion yen in line with our initial plan through the review of Capex and inventory reduction efforts.

While we will take additional measures to respond to rapid changes in the operating environment, we will continue to thoroughly capture demand related to EVs, decarbonization including renewable energy, and sensors indispensable for a data-oriented society, with the aim of maximizing our sustainable corporate value.

That concludes my presentation. Thank you very much for your attention.