3rd Quarter of fiscal 2025 Performance Briefing (Speech Text)

Q3, FY March 2025 Results Highlights

FY March 2025 Projections

Tetsuji Yamanishi

Senior Executive Vice President & CFO

Hello, I am Tetsuji Yamanishi. Thank you for taking the time to attend TDK’s performance briefing for the third quarter on a YTD (year-to-date) basis of FY March 2025. I would like to explain the highlights of our consolidated results and FY March 2025 projections.

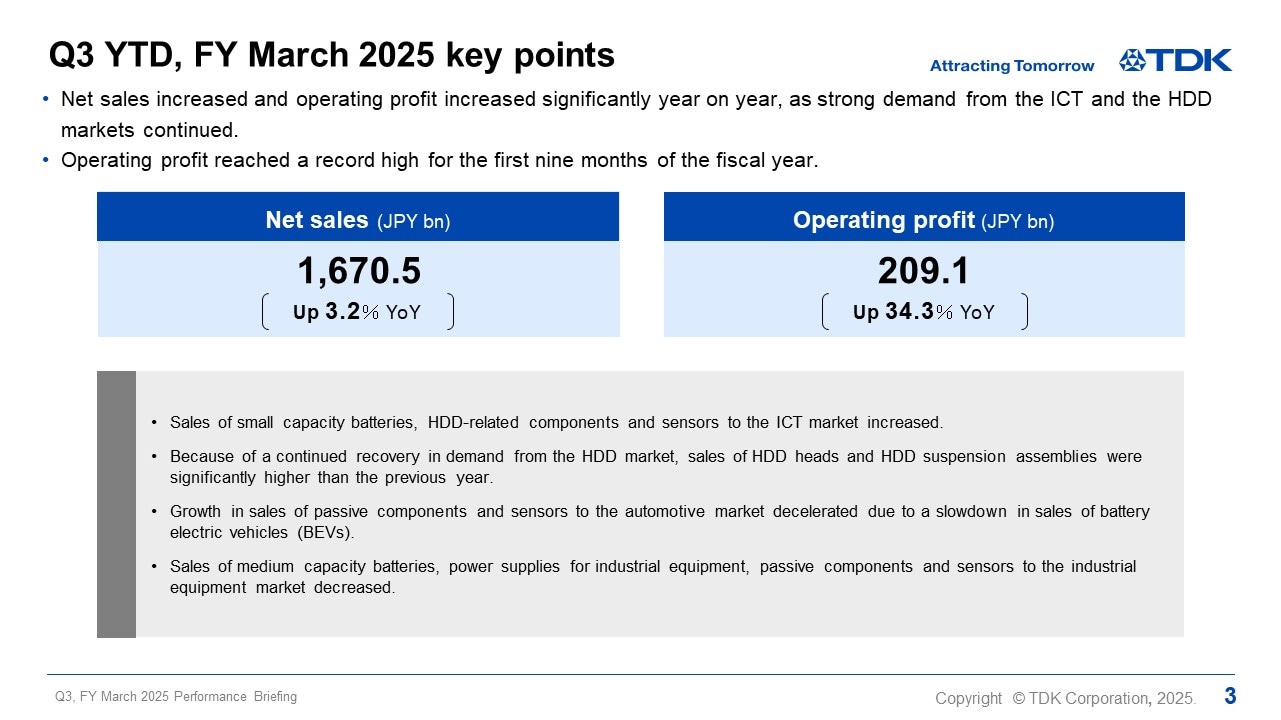

Q3 YTD, FY March 2025 key points

I would like to start with the key points of the first nine months of FY March 2025. During the first nine months of fiscal 2025, the global economy remained unstable with regional variances due to the growing tensions in the Middle East on top of the continued economic slowdown in Europe and China, although North America remained robust. In terms of exchange rates, the yen continued to weaken against the dollar and the euro.

Looking at the electronics market, which has a large bearing on TDK’s consolidated business results, an increase in replacement demand, the launch of new models and other factors resulted in growth in the production of products related to ICT on a year-on-year basis. Demand for smartphones, notebook PCs, and tablets was robust. Demand for nearline HDDs for data centers also recovered sharply. On the other hand, in the industrial equipment market, capital investment demand remained weak in general. In the automotive market, demand for battery electronic vehicles (BEVs) remained sluggish, resulting in lower component demand than we had expected at the beginning of the period.

In this business environment, during the first nine months of fiscal 2025, sales of small capacity batteries, HDD-related components and sensors to the ICT market increased sharply, and because of a continued recovery in demand from the HDD market, sales of HDD heads and HDD suspension assemblies were significantly higher than in the previous year.

On the other hand, growth in sales of passive components and sensors to the automotive market decelerated due to a slowdown in sales of BEVs, and sales of medium capacity batteries, power supplies for industrial equipment, passive components and sensors to the industrial equipment market decreased. Consequently, net sales increased 3.2% year on year.

Operating profit increased 34.3% year on year due to the sharp depreciation of the yen, an increase in sales of products to the ICT market, as well as rationalization and reaping the benefits of the restructuring implemented in the previous fiscal year, setting a new record for operating profit for the first nine-month period.

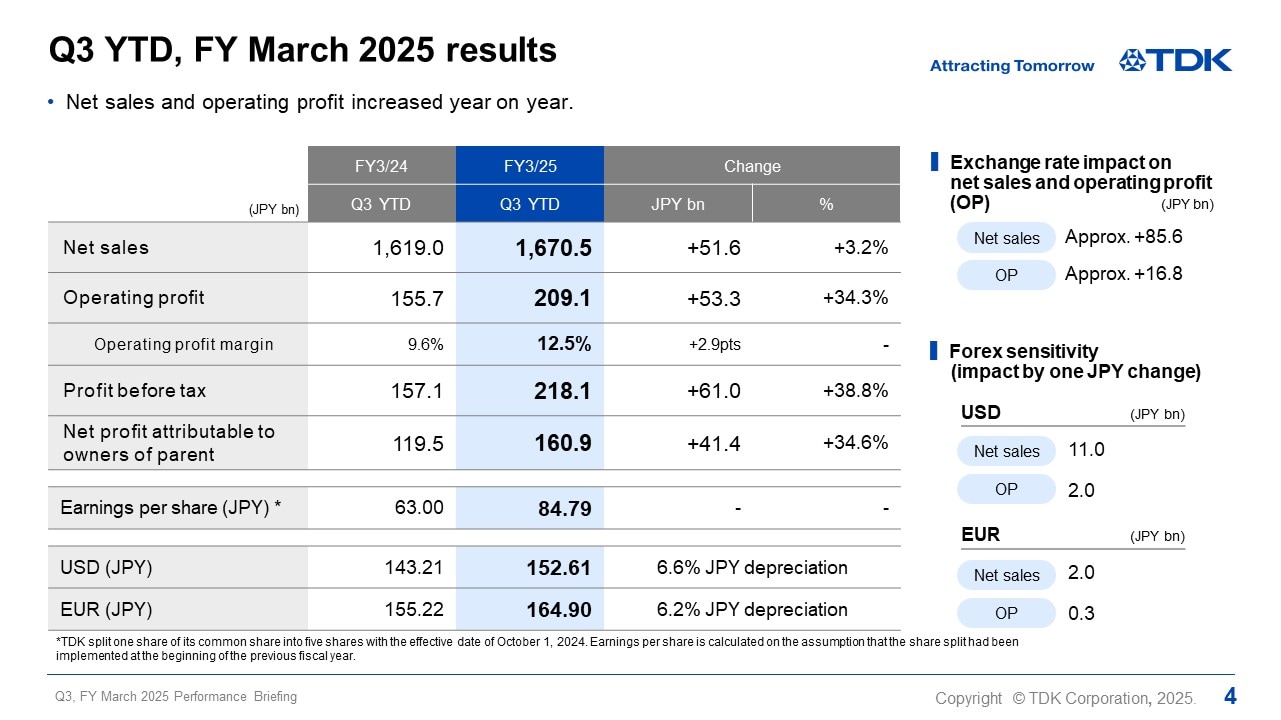

Q3 YTD, FY March 2025 results

I would like to present an overview of our results for the third quarter on a YTD basis of FY March 2025.

There was an increase of about JPY 85.6 billion in net sales and an increase of about JPY 16.8 billion in operating profit due to exchange rate fluctuations against the U.S. dollar and other currencies. Including this impact, net sales were JPY 1,670.5 billion, an increase of JPY 51.6 billion, or 3.2%, year on year, and operating profit was JPY 209.1 billion, an increase of JPY 53.3 billion, or 34.3%, year on year. Profit before tax was JPY 218.1 billion, an increase of JPY 61.0 billion, or 38.8%, year on year. Net profit attributable to owners of parent was JPY 160.9 billion, an increase of 34.6% year on year. In summary, TDK set record highs in operating profit and all other profit items. Earnings per share amounted to JPY 84.79. In terms of exchange rate sensitivity, we estimate that a change of JPY 1 against the U.S. dollar will affect operating profit by about JPY 2 billion a year, the same as our previous estimate, while a JPY 1 change against the euro will have an impact of about JPY 0.3 billion a year.

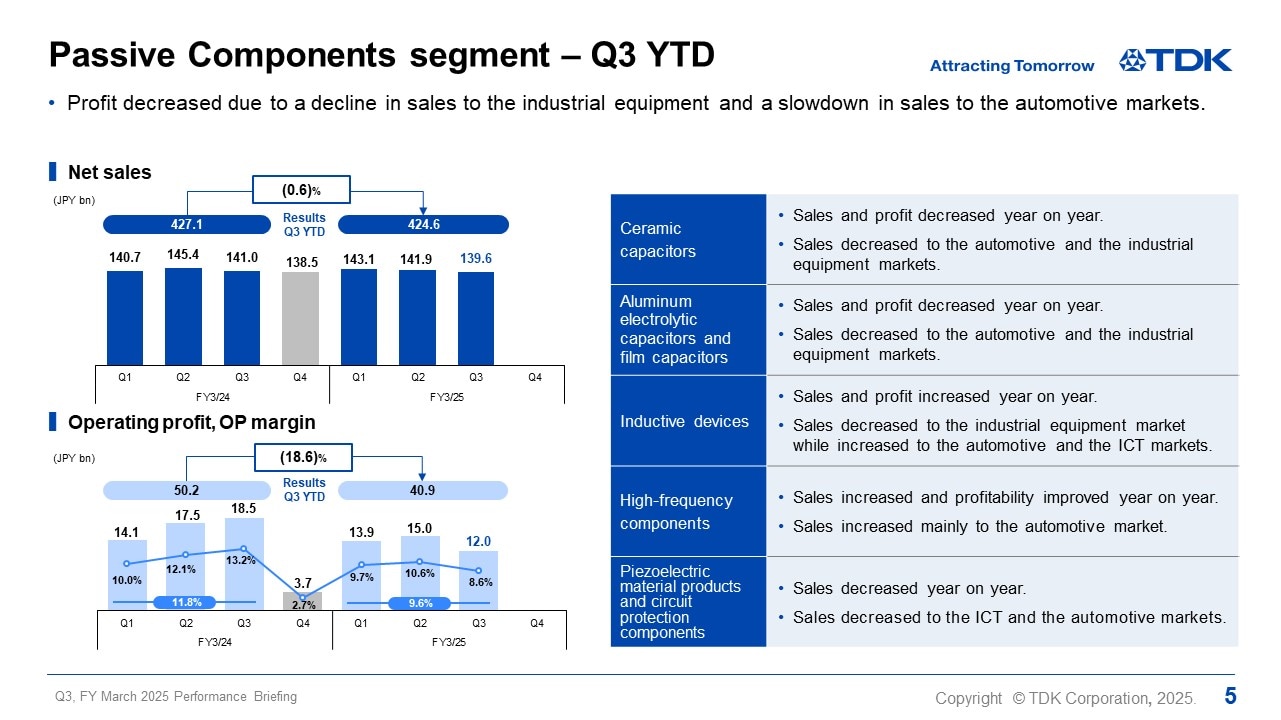

Passive Components segment – Q3 YTD

I will now move on to segment results for the third quarter on a YTD basis of FY March 2025.

First, in the Passive Components segment, demand from the industrial equipment market remained sluggish, and sales to the automotive market, such as for BEVs, slowed down. As a result, net sales were JPY 424.6 billion, a decrease of 0.6% year on year. Operating profit was JPY 40.9 billion, a decrease of 18.6% year on year.

Sales and profit decreased year on year for ceramic capacitors and aluminum electrolytic capacitors and film capacitors, which have a high ratio of sales to the automotive and industrial equipment markets. Sales and profit of inductive devices increased year on year on the back of a rise of sales to the ICT and automotive markets, among other factors, despite a decline in sales to the industrial equipment market. Sales of high-frequency components increased year on year due mainly to growth in sales to the automotive market, resulting in an improvement in profitability. Sales of piezoelectric material products and circuit protection components decreased year on year reflecting a decline in sales to the ICT and automotive markets.

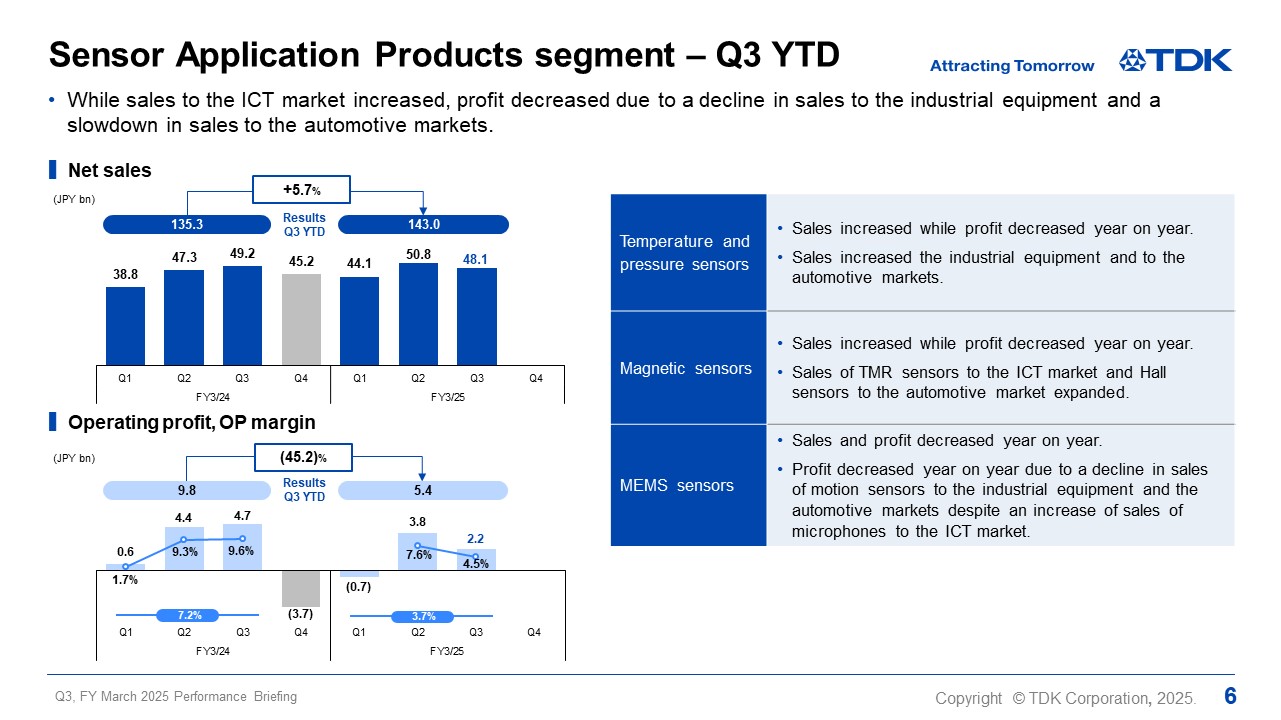

Sensor Application Products segment – Q3 YTD

In the Sensor Application Products segment, net sales increased 5.7% year on year to JPY 143.0 billion, while operating profit decreased 45.2% year on year to JPY 5.4 billion.

Sales of temperature and pressure sensors increased year on year reflecting a rise in sales to the industrial equipment and automotive markets, while profit decreased year on year as a one-time gain from the sale of assets had been included in the previous year. In magnetic sensors, sales increased year on year due to a rise in sales of TMR sensors for smartphone applications as well as an expansion of sales of Hall sensors to the automotive market, while profit decreased year on year mainly reflecting a rise in depreciation and other expenses due to capital investment to increase production capacity.

In MEMS sensors, the profitability of microphones improved as sales to the ICT market increased, while profit of motion sensors decreased due to a decline in sales to the automotive and industrial equipment markets. This resulted in a year-on-year decrease in sales and profit of MEMS sensors on the whole.

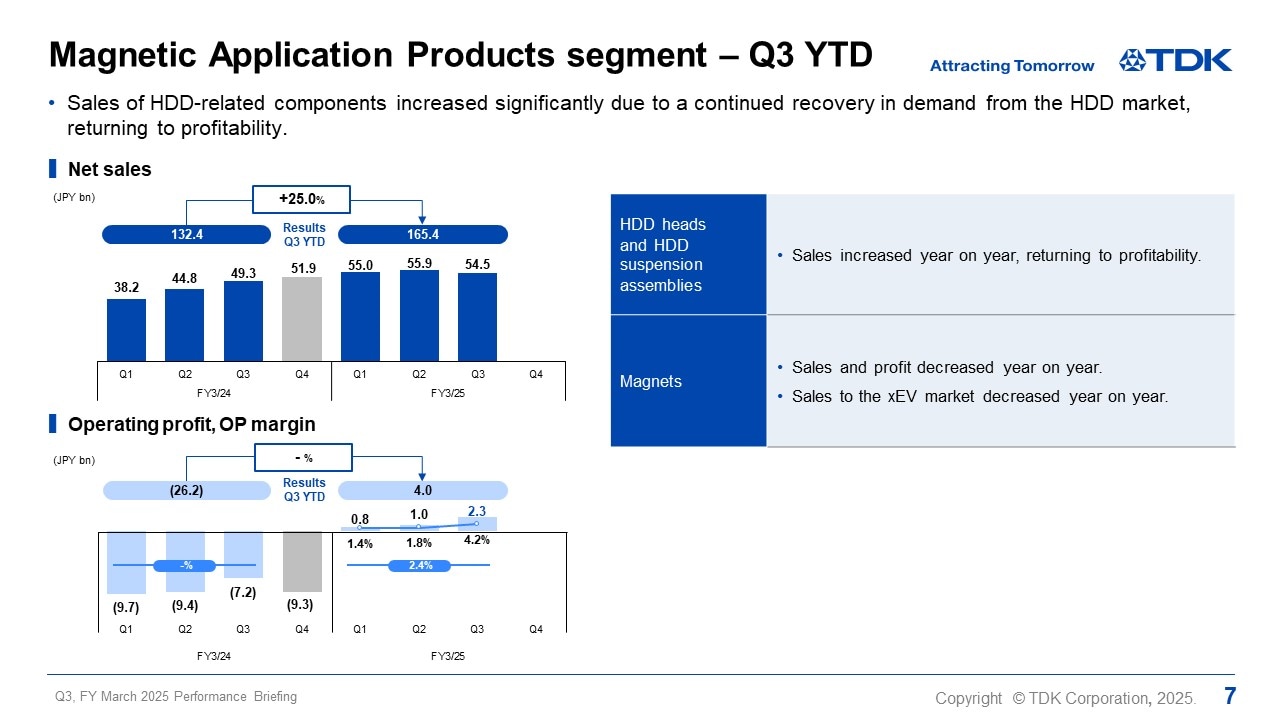

Magnetic Application Products segment – Q3 YTD

In the Magnetic Application Products segment, net sales rose sharply by 25.0% year on year to JPY 165.4 billion, and operating profit returned to the black.

In HDD heads and HDD suspension assemblies, demand for nearline HDDs for data centers increased 1.6 times year on year, resulting in a return to profitability for both HDD heads and HDD suspension assemblies. The sales volume of HDD heads increased 37% year on year, and the sales volume of nearline HDD heads, in particular, nearly doubled on a year-on-year basis. While still slightly below the break-even point after the restructuring, HDD heads returned to profitability due to an improved product mix and an increase in utilization rate. The sales volume of HDD suspension assemblies exceeded the break-even point, remaining profitable.

Both sales and profit of magnets decreased year on year due to lower sales to the automotive market.

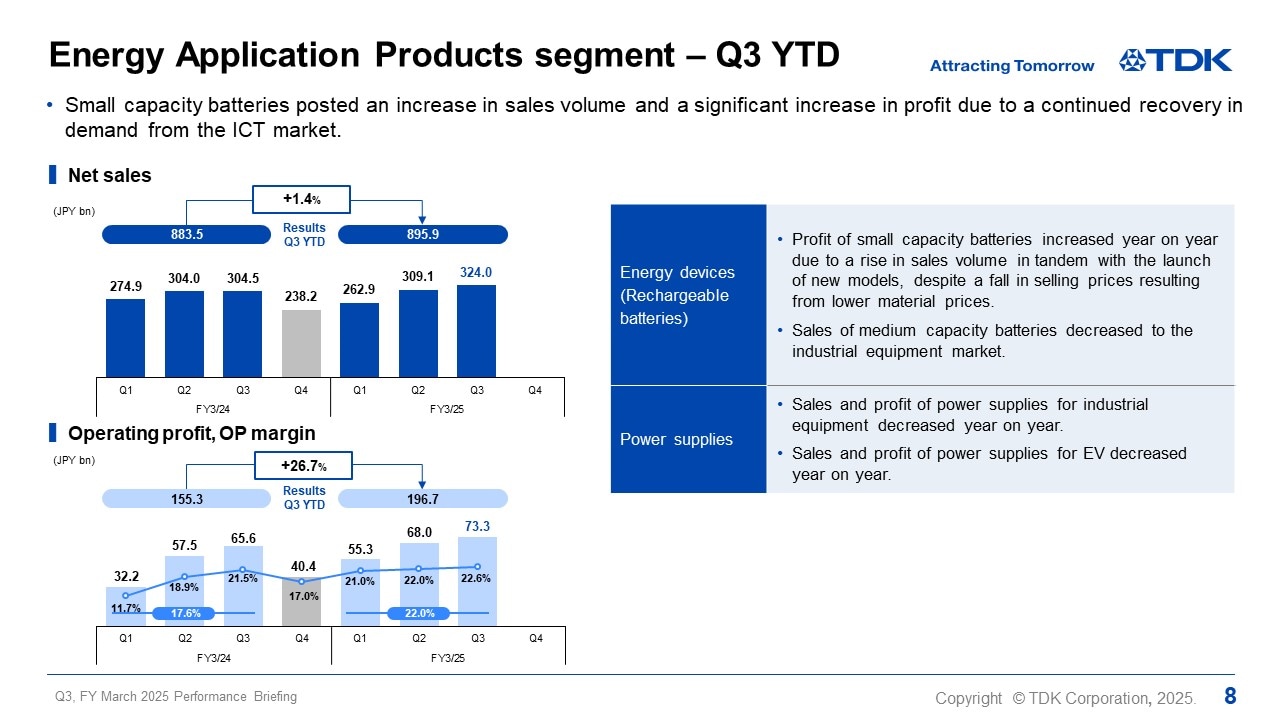

Energy Application Products segment – Q3 YTD

In the Energy Application Products segment, net sales amounted to JPY 895.9 billion, up by 1.4% year on year, while operating profit rose strongly by 26.7% year on year to JPY 196.7 billion.

Profit of rechargeable batteries increased significantly due to a rise in sales volume on the back of the launch of new smartphone models as well as an improved product mix, despite the impact of a decline in selling prices resulting from lower material prices.

Power supplies for industrial equipment saw a year-on-year decline in terms of both sales and profit as demand for industrial equipment applications failed to recover, and both sales and profit of power supplies for EVs, such as BEVs, also decreased year on year due to a slowdown in automobile sales.

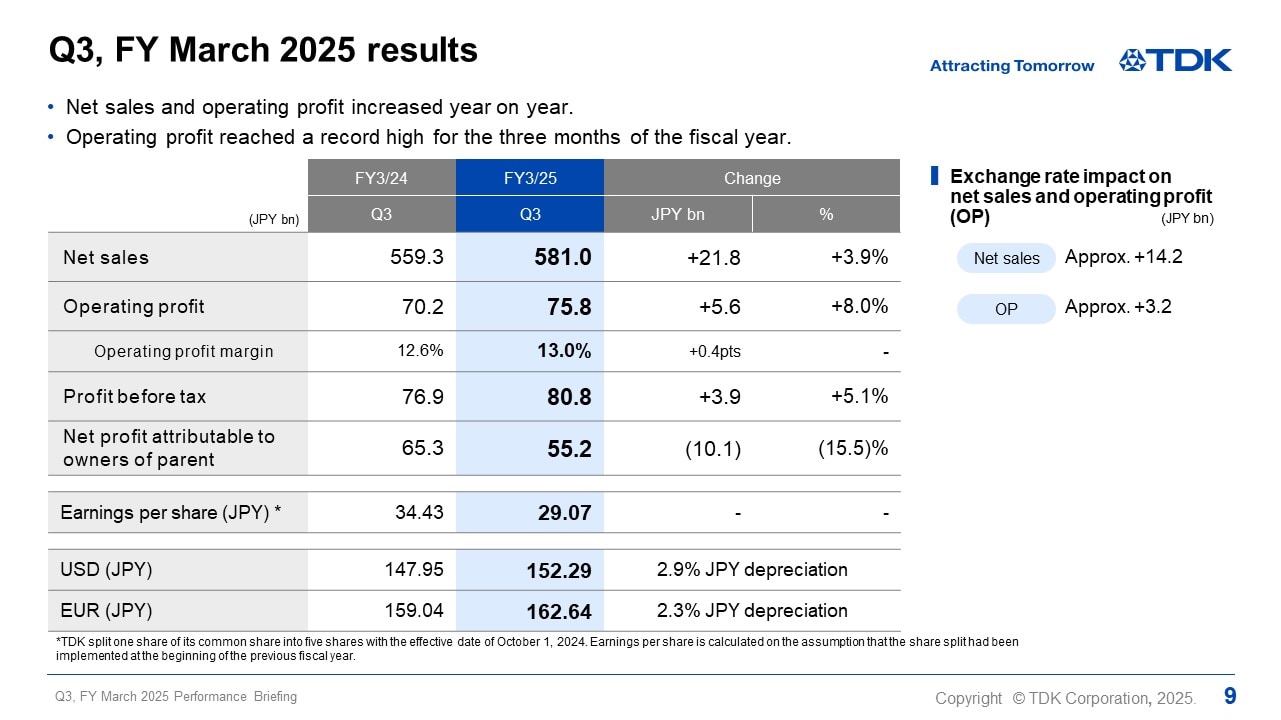

Q3, FY March 2025 results

I would like to present an overview of our third quarter results.

There was an increase of about JPY 14.2 billion in net sales and an increase of about JPY 3.2 billion in operating profit due to exchange rate fluctuations against the U.S. dollar and other currencies. Including this impact, net sales were JPY 581.0 billion, an increase of JPY 21.8 billion, or 3.9%, year on year, and operating profit was JPY 75.8 billion, an increase of JPY 5.6 billion, or 8.0%, year on year. Profit before tax was JPY 80.8 billion, an increase of JPY 3.9 billion, or 5.1%, year on year. Net profit attributable to owners of parent was JPY 55.2 billion. TDK set a new record high in operating profit on a quarterly basis.

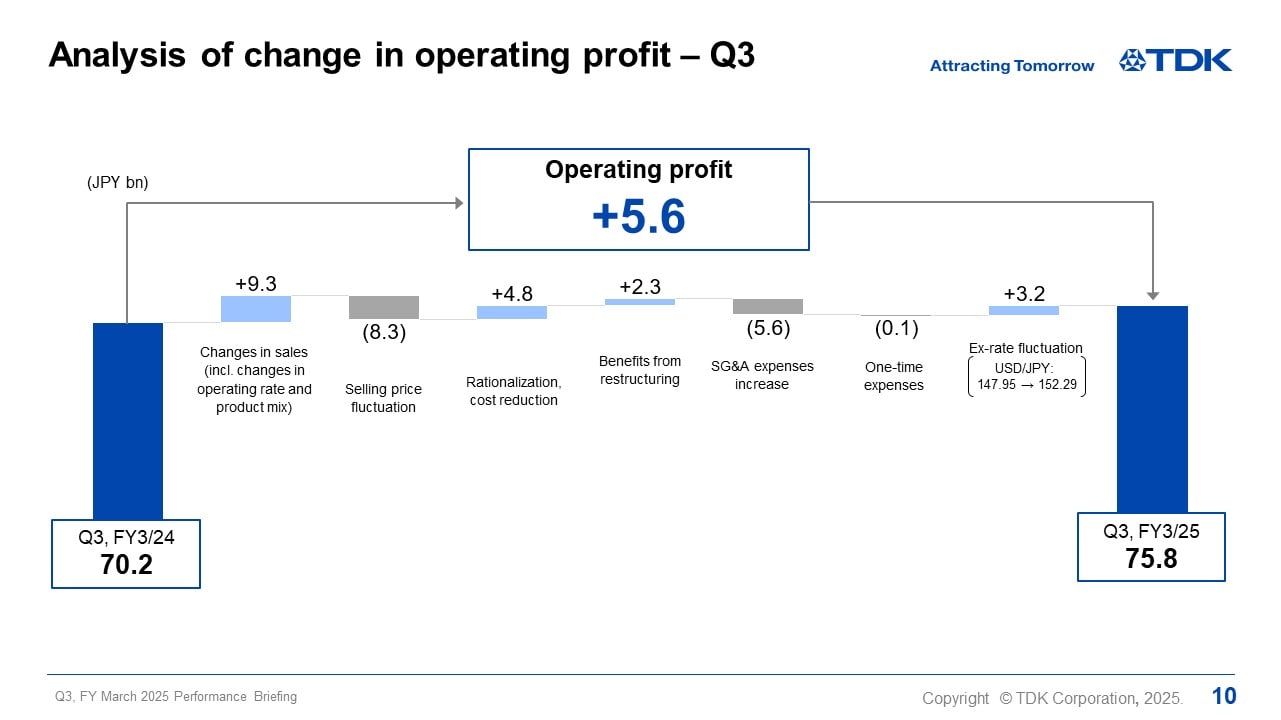

Analysis of change in operating profit – Q3

Next is an analysis of the JPY 5.6 billion year-on-year increase in operating profit for the third quarter. Operating profit increased JPY 9.3 billion due to changes in sales, reflecting an increase in the sales volume of rechargeable batteries, HDD heads and HDD suspension assemblies, although there was a negative effect on profit due to a decline in the sales volume of passive components and sensors. The effects of rationalization of JPY 4.8 billion and benefits from restructuring of JPY 2.3 billion almost absorbed the JPY 8.3 billion decline in profit caused by selling price fluctuation. SG&A expenses increased by JPY 5.6 billion reflecting an increase in R&D expenses related to rechargeable batteries for which TDK has been accelerating the development of new products. These factors, including the positive effect of the lower yen amounting to JPY 3.2 billion, contributed to the JPY 5.6 billion increase in operating profit.

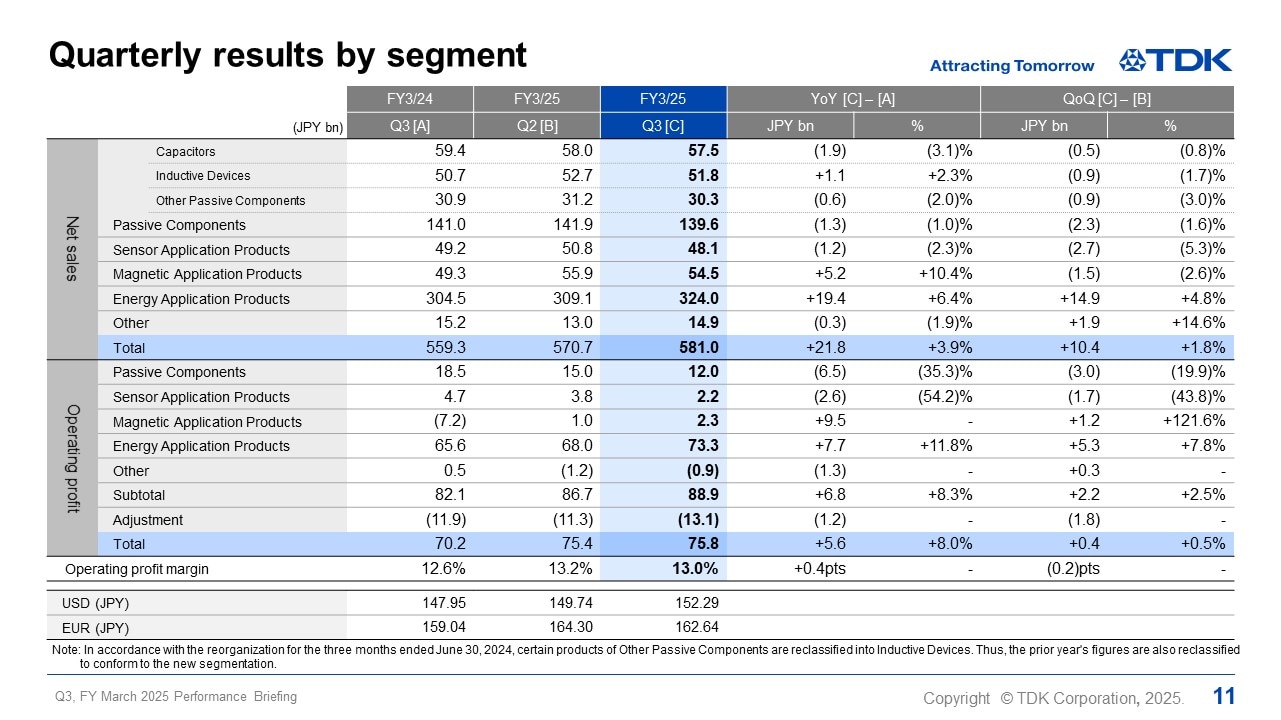

Quarterly results by segment

Now, I will explain some of the factors behind the changes in segment sales and operating profit from the second quarter to the third quarter of FY March 2025.

First, in the Passive Components segment, net sales decreased by JPY 2.3 billion, or 1.6%, from the second quarter, and operating profit decreased by JPY 3.0 billion, or 19.9%, from the second quarter. Sales of ceramic capacitors remained virtually unchanged from the second quarter as sales to the automotive market, for which sales had been anticipated to increase from the second quarter, continued to be sluggish. Demand related to the industrial equipment market also remained stagnant. In the ICT market, sales decreased from the second quarter mainly for inductive devices as sales declined in the third quarter following the seasonal peak demand for smartphones in the second quarter. In terms of operating profit, while sales of ceramic capacitors remained flat, profit declined due to a decrease in production volume and an increase in fixed costs. Profit of other businesses also declined as a result of lower sales related to smartphone applications.

Next, in the Sensor Application Products segment, net sales decreased by JPY 2.7 billion, or 5.3%, from the second quarter, and operating profit decreased by JPY 1.7 billion, or 43.8%, from the second quarter. Temperature and pressure sensors decreased in terms of both sales and profit due to a drop in demand related to the European automotive market. Magnetic sensors saw a decrease in sales and profit reflecting the front-loaded demand for TMR sensors for smartphone applications in the second quarter. Sales of MEMS sensors increased as a result of a rise in sales of motion sensors for gaming applications and growth in sales of new microphone models, which led to a reduction in operating loss.

In the Magnetic Application Products segment, net sales decreased by JPY 1.5 billion, or 2.6%, from the second quarter, while operating profit rose by JPY 1.2 billion from the second quarter. Amid a demand environment where demand for nearline HDD remained robust, the sales volume declined 16% as expected in reaction to the front-loaded shipment of HDD heads to major customers in the second quarter, but a positive profit was secured on the back of improved utilization rate. The sales volume of HDD suspension assemblies increased about 20% as expected, remaining profitable. As for magnets, net sales remained virtually flat, while operating loss diminished including a JPY 1.5 billion decline in one-time expenses.

In the Energy Application Products segment, net sales increased by JPY 14.9 billion, or 4.8%, from the second quarter, and operating profit increased by JPY 5.3 billion, or 7.8%, from the second quarter. As for rechargeable batteries, sales of small capacity batteries to the ICT market, mainly those related to Chinese high-end smartphones, increased. As a result, both sales and profit of rechargeable batteries on the whole increased from the second quarter. Power supplies for industrial equipment decreased in terms of both sales and profit. Sales of power supplies for EVs decreased, while loss has diminished.

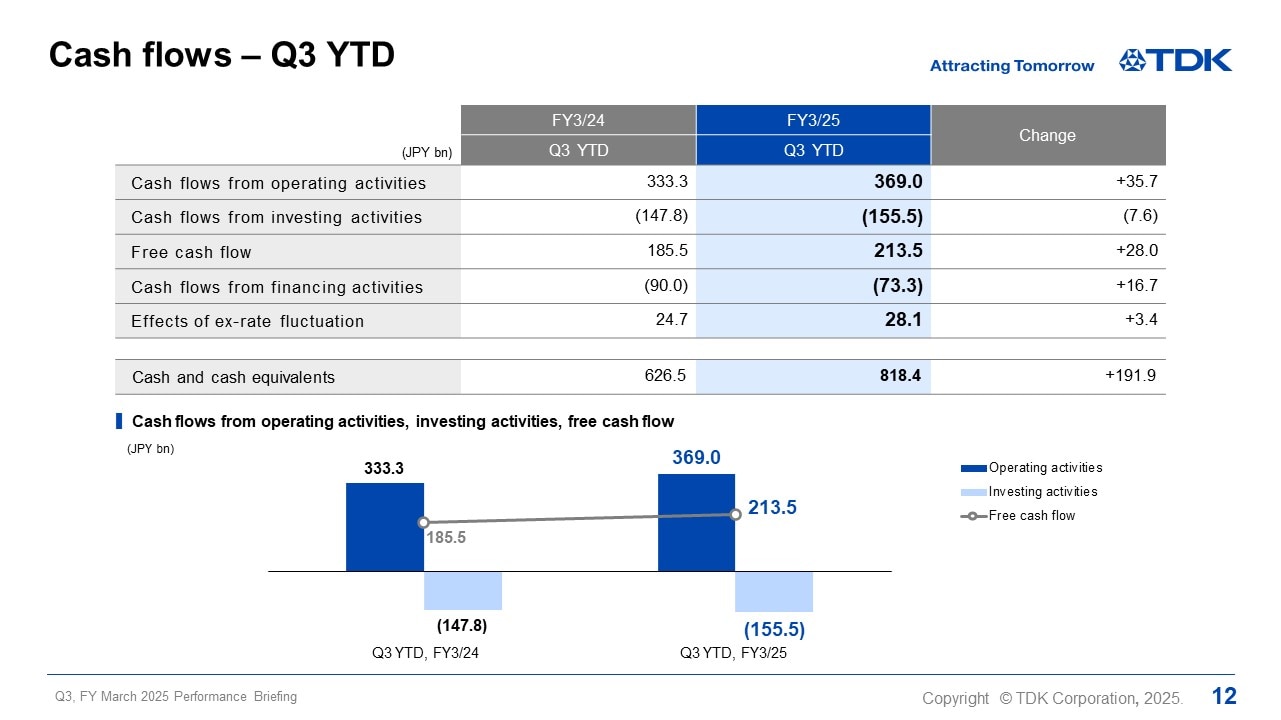

Cash flows – Q3 YTD

I would like to present an overview of cash flows.

In the third quarter on a YTD basis of FY March 2025, operating cash flow amounted to JPY 369.0 billion, investing cash flow—such as CAPEX—amounted to JPY 155.5 billion, and free cash flow amounted to JPY 213.5 billion, exceeding the JPY 185.5 billion of free cash flow in the same period of the previous fiscal year. Free cash flow was significantly above the initial forecast level due to a decline in CAPEX and an increase in profit, on top of our ongoing efforts to maintain an adequate inventory level as in the previous year. While it is already significantly above our full-year free cash flow target announced at the beginning of the current fiscal year, we aim to further increase free cash flow through expanding profits and enhancing capital efficiency.

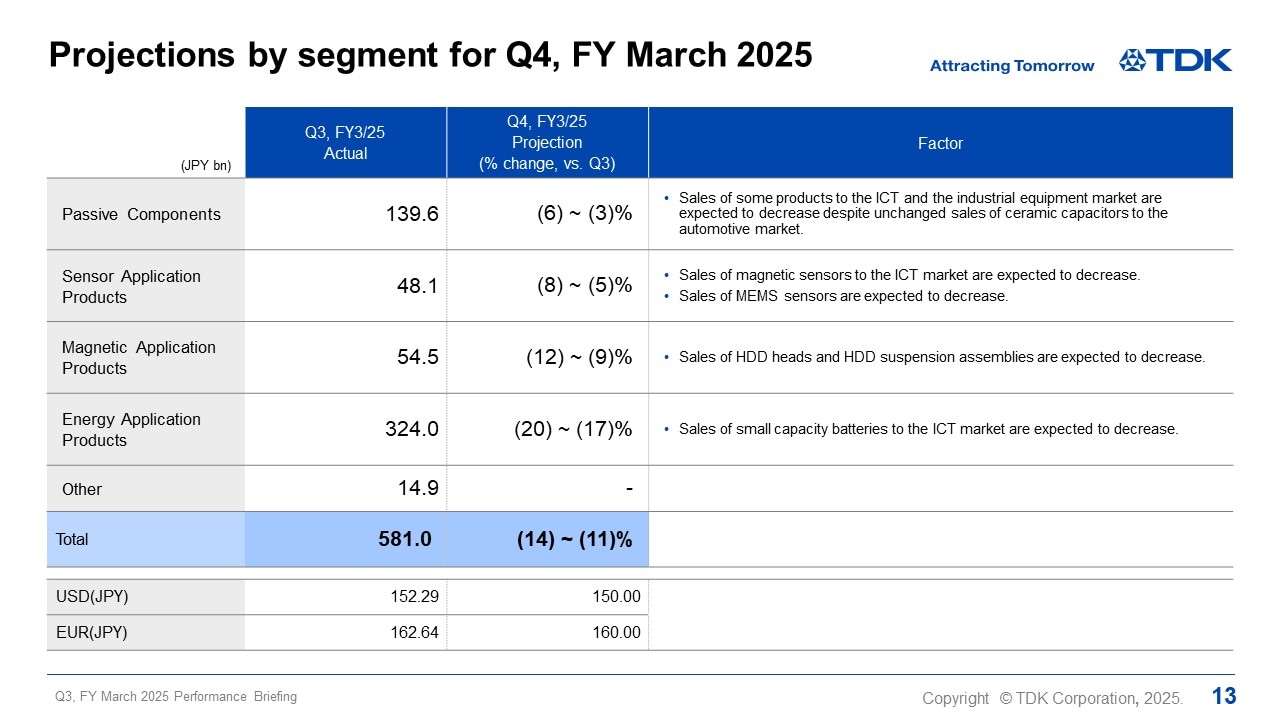

Projections by segment for Q4, FY March 2025

I would now like to discuss our projections regarding changes in segment net sales for the fourth quarter.

For the fourth quarter, we have changed our exchange rate assumption to JPY 150 against the U.S. dollar from JPY 140, which we had made at the beginning of the fiscal year.

First, as for Passive Components, demand for MLCC in the automotive market is expected to remain flat amid expectations that vehicle production volume will decline. Sales in other businesses will likely decrease overall reflecting a decline in smartphone demand due to seasonal factors as well as the continued weak demand conditions in the industrial equipment market. As a result, segment sales are forecast to decrease by 3–6% overall on a quarter-on-quarter basis.

As for Sensor Application Products, sales of temperature and pressure sensors are expected to increase slightly on the back of a moderate increase in sales to the automotive market, while sales of magnetic sensors for smartphone applications are predicted to decrease due to a decline in demand due to seasonal factors. Meanwhile, sales of MEMS sensors, particularly those of new microphone products, will likely grow, although overall sales of MEMS sensors are expected to decline owing to the front-loaded shipment of motion sensors for gaming applications in the third quarter. As a result, segment sales are forecast to decrease by 5–8% overall on a quarter-on-quarter basis.

Next, in the Magnetic Application Products segment, we expect HDD production to decrease by approximately 9% and nearline HDD production to drop by approximately 6%. While the sales volume of HDD heads is anticipated to remain virtually flat from the third quarter, sales of HDD suspension assemblies are predicted to decrease by approximately 9%. As a result, segment sales are forecast to decrease by 9–12% overall on a quarter-on-quarter basis.

Lastly, as for Energy Application Products, while sales of small capacity batteries will likely decrease due to the seasonal nature of demand for smartphones, demand for power supplies for industrial equipment and power supplies for EVs is expected to recover moderately. As a result, segment sales are forecast to decrease by 17–20% overall on a quarter-on-quarter basis.

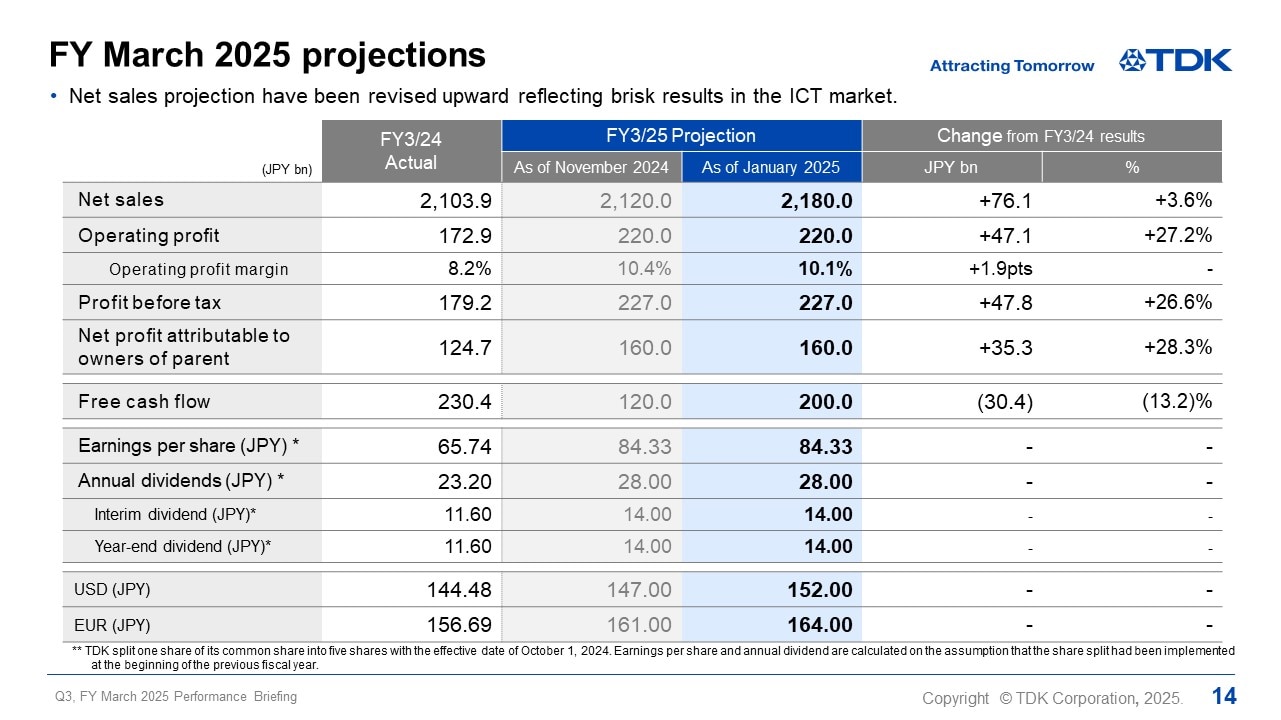

FY March 2025 projections

I would like to go over our full-year projections for FY March 2025.

The third quarter results significantly exceeded the previous projection due to robust sales of rechargeable batteries, HDD heads and HDD suspension assemblies on top of the positive effect of the lower yen. In the fourth quarter, a positive effect from a lower yen is anticipated, as can be seen from the change in our exchange rate assumption to JPY 150 against the U.S. dollar from JPY 140, but demand in the automotive and industrial equipment markets, including demand related to BEVs, has been slow to recover. Therefore, earnings of passive components and sensors in the fourth quarter are expected to be significantly lower than the level of the previous projection.

In addition, TDK will review its previously announced restructuring costs of approximately JPY 10.0 billion for FY March 2025, and is expected to recognize one-time expenses of approximately JPY 18.0 billion in total for fiscal 2025 in light of risks associated with the write-down of assets in the high-frequency components business under the Passive Components segment.

As for consolidated projections for FY March 2025, TDK has revised its projection for net sales upward from JPY 2,120.0 billion to JPY 2,180.0 billion based on the above assumptions. The projections for operating profit and all other profit items have not been revised from the previous projections in light of the recognition of the additional restructuring costs.

The projection for CAPEX has been revised downward by JPY 10.0 billion from JPY 250.0 billion to JPY 240.0 billion, and the projection for R&D expenses has been revised upward by JPY 10.0 billion from JPY 240.0 billion to JPY 250.0 billion.

We have kept our previous dividend forecast unchanged.

Based on these changes, our free cash flow projection has improved significantly from the previous projection of JPY 120.0 billion to JPY 200.0 billion.