[ 2nd Quarter of fiscal 2023 Performance Briefing ]

Consolidated Full Year Projections for FY March 2023

Mr. Noboru Saito

President & CEO

I am Noboru Saito. I would like to go over our full-year earnings projections for the fiscal year ending March 2023.

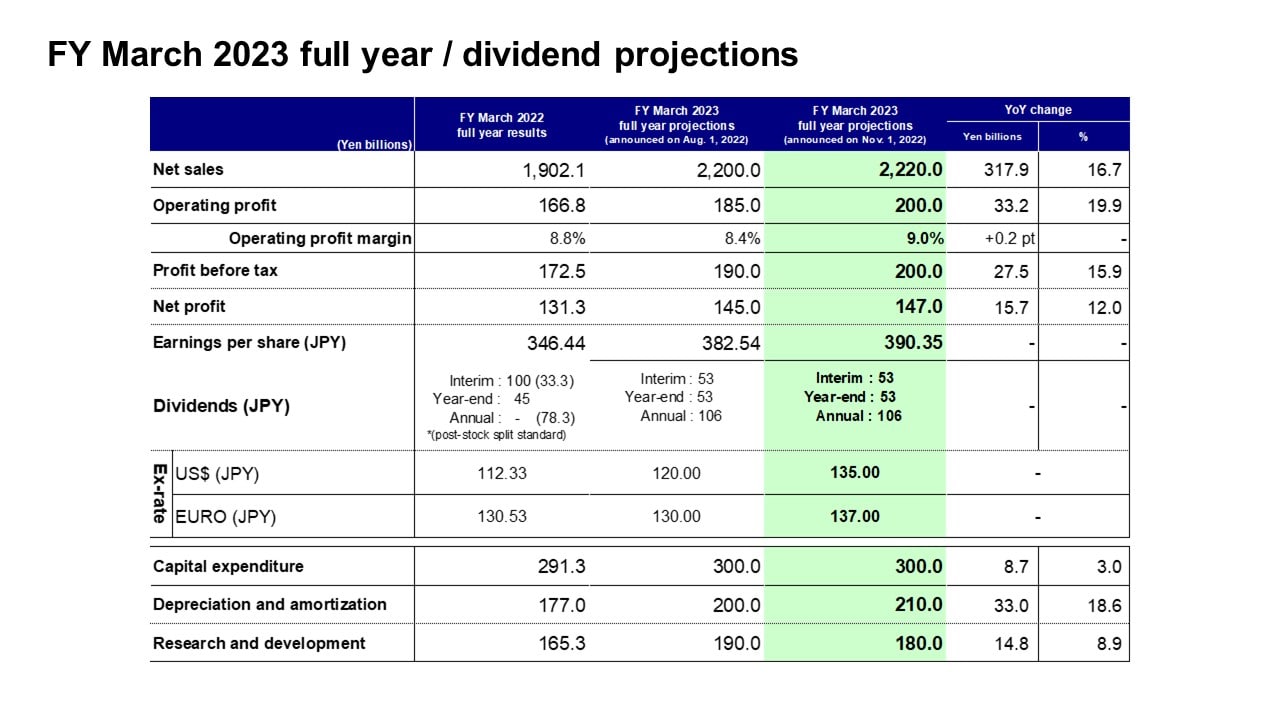

FY March 2023 full year / dividend projections

First, I would like to discuss our projections for consolidated financial results and dividends for the fiscal year ending March 2023 and the underlying market conditions.

The global economic growth forecast (announced by the IMF), as a basis for our market forecast, was revised downward to 3.6% in April and to 3.2% in October.

As for production activities, while there have been signs of moderate recovery from the lockdowns imposed in China due to the resurgence of COVID-19, ongoing geopolitical risks resulting from Russia’s invasion of Ukraine and interest rate hikes at a pace exceeding expectations have increased concerns over global economic slowdown.

Amid such macro-economic environment, we have revised our projections on demand for and production volume of major devices related to TDK’s businesses.

In light of the current order status, our projections have been revised upward from the previous projections as follows: net sales of 2,220.0 billion yen: operating profit of 200.0 billion yen; profit before tax of 200.0 billion yen; and net profit of 147.0 billion yen.

Our exchange rate assumptions for the second half of the fiscal year ending March 2023 are 135 yen against the U.S. dollar and the euro.

There have been no changes in the dividend projections announced at the beginning of the current fiscal year. We expect the interim dividend to be 53 yen, year-end dividend to be 53 yen, and annual dividend to be 106 yen.

While we have reviewed capital expenditure in light of the macro economy and demand trends, there have been no changes from the initial projections due to the effect of the depreciation of the yen. Research and development expenses are projected to decrease from 190.0 billion yen to 180.0 billion yen, and depreciation and amortization is projected to be 210.0 billion yen.

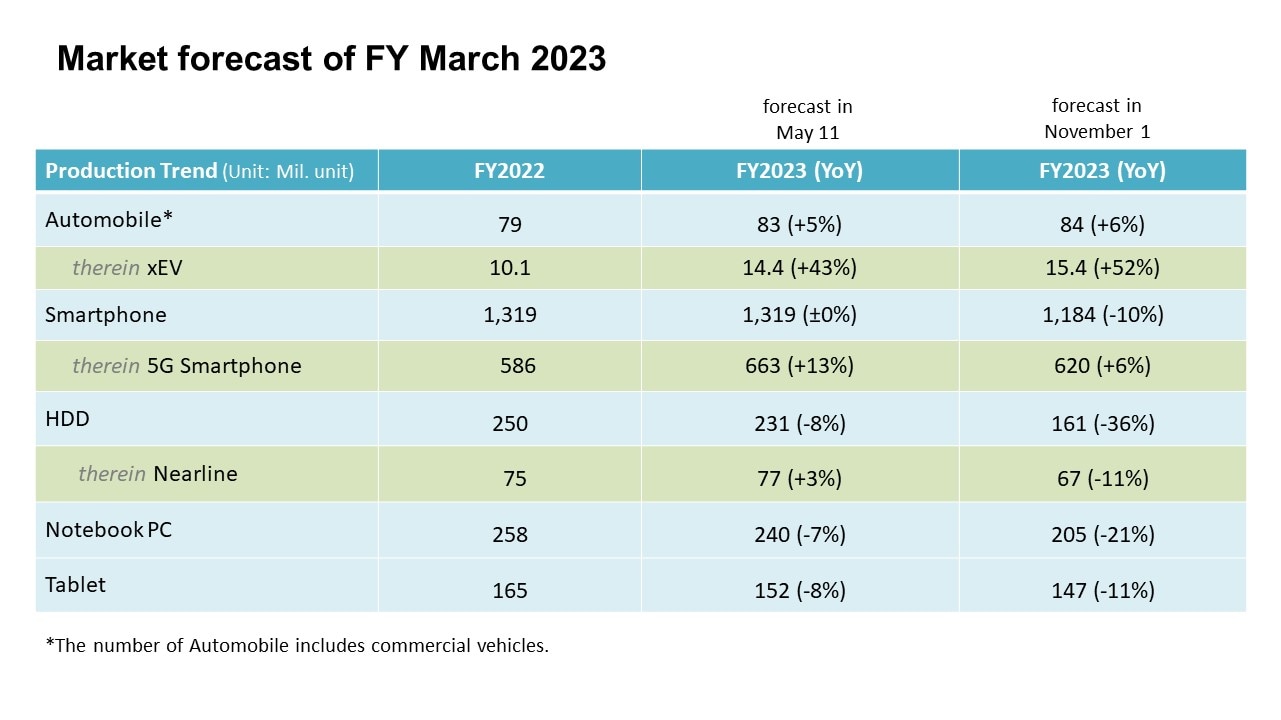

Market forecast of FY March 2023

Next, I will explain demand and production volume in the major markets related to TDK as a basis for our full-year projections.

We have assumed that automobile production volume will slightly increase from our initial projection to 84 million units on the back of an increase in xEV production volume amid the easing of component shortages.

On the other hand, while we had initially predicted that production volume for smartphones, which represent the ICT market, would remain virtually flat from the previous year, it is now projected to be 1,184 million units, down 10% year on year.

We have revised our projections for PC and tablet production volume significantly downward. Production volume is assumed to decrease by 21% year on year to 205 million units for PCs and to decrease by 11% year on year to 147 million units for tablets. Consequently, while we had initially predicted that production volume for HDDs would decrease by 8% year on year, it is now assumed to decrease by 36% year on year to 161 million units due to a rapid decline in demand related to PCs and data centers.

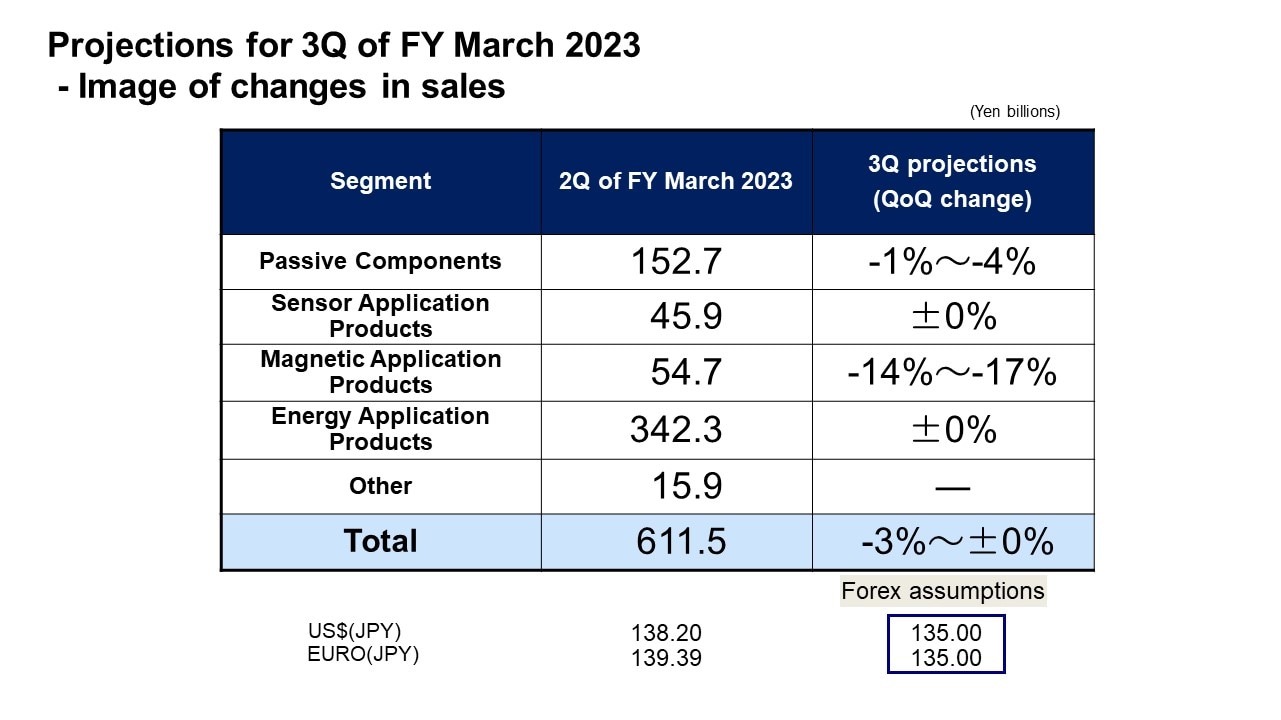

Projections for 3Q of FY March 2023 - Image of changes in sales

Now, I would like to discuss our projection regarding changes in net sales for the third quarter by segment.

We anticipate that overall sales for the third quarter will be somewhere between 3% down from the second quarter and at the same level as the second quarter, based on the assumption of the aforementioned macro-economic environment and the exchange rate assumption of 135 yen against the U.S. dollar and the euro for the second half of the fiscal year ending March 2023.

In the Passive Components segment, sales are expected to decrease by between 1-4% from the second quarter in light of seasonal factors, despite the recovery trend in automobile production and solid demand as a result of the spread of EVs and ADAS.

In the Sensor Application Products segment, sales are predicted to be ±0% from the second quarter in light of current trends in the major markets.

In the Magnetic Application Products segment, sales are projected to decrease between 14-17% from the second quarter given sluggish HDD demand for PC and data center applications.

In the Energy Application Products segment, sales are assumed to be ±0% from the second quarter in light of the ICT market trends, despite robust sales of medium-sized rechargeable batteries.

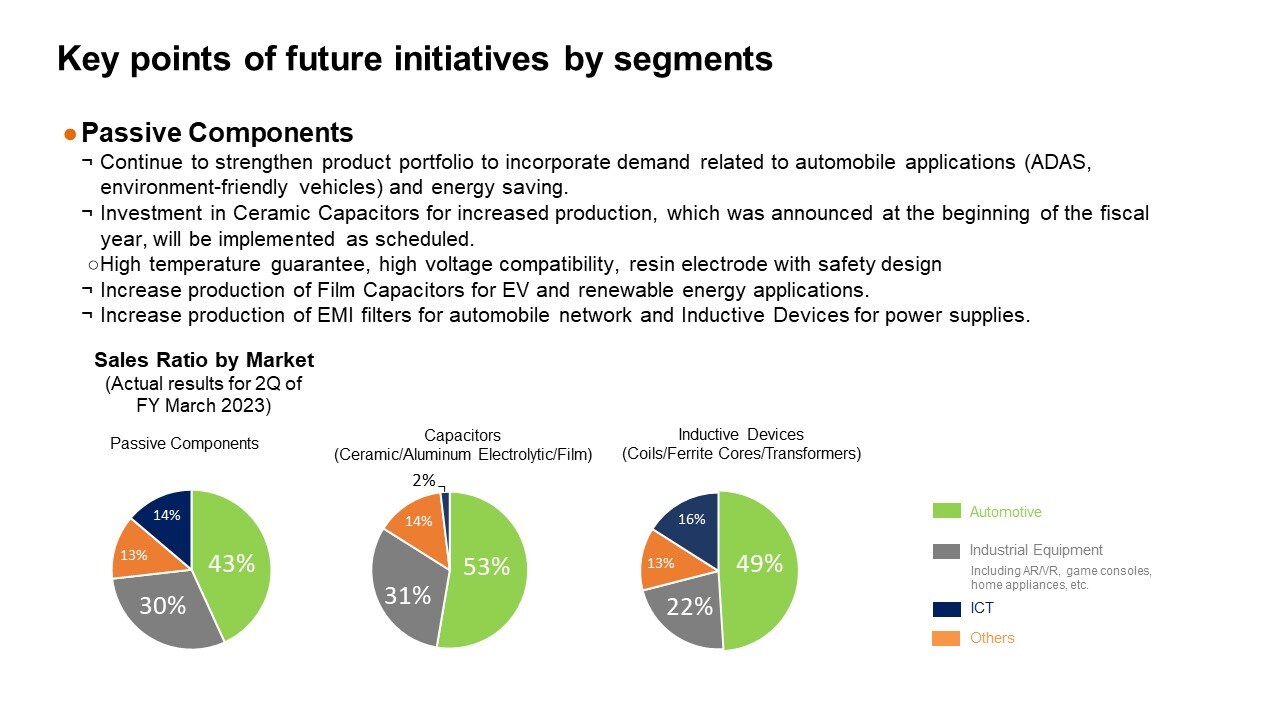

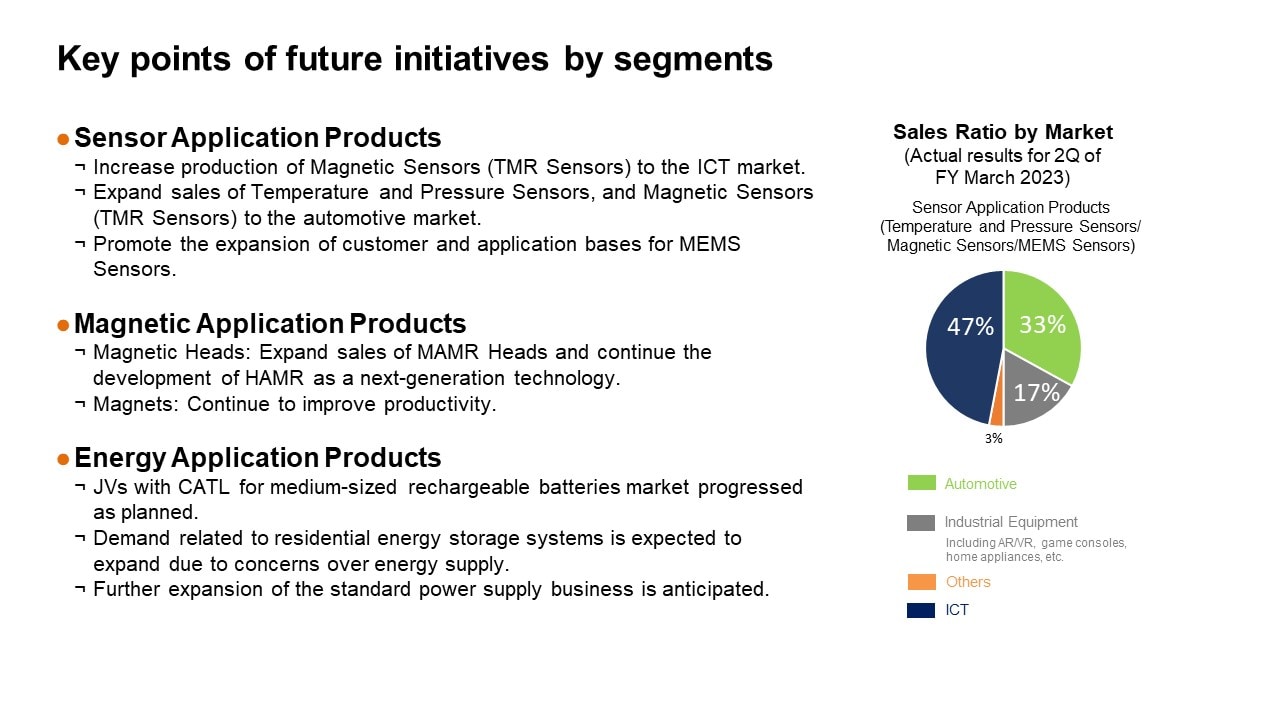

Key points of future initiatives by segments

Now, I would like to talk about key points of future initiatives by segment.

In the Passive Components segment, as a result of the acquisition of EPCOS, business structure reforms with the main focus on Ceramic Capacitors, investment in development and sales expansion efforts mainly for automobile and industrial equipment applications, the automotive market accounts for 43% and the industrial equipment market accounts for 30% in the ratio of Passive Components sales. While we recognize that we have already established a global supply system with a product portfolio that can respond to demand related to the automotive market, with a focus on EVs which are expected to grow rapidly amid the shift toward a decarbonized society, as well as renewable energy and energy-saving applications, it is our policy to continue to strengthen our system in the future.

As for Ceramic Capacitors, we will continue to enhance product capabilities, such as high temperature guarantee and high voltage compatibility, while implementing the investment for increased production announced at the beginning of the fiscal year as scheduled in order to respond to growing demand.

We will also invest in Film Capacitors to increase production while continuing the development of products with high voltage compatibility, as demand is expected to grow for EV and renewable energy applications.

In the field of Inductive Devices, by combining our product development capabilities based on ferrite and other materials with our accumulated manufacturing capabilities such as winding, layering and thin film technologies, we will continue our investment for development and increased production to respond to markets needs related to EVs and ADAS as in the case with Capacitors.

Key points of future initiatives by segments

In the Sensor Application Products segment, the ICT markets accounts for 47%, the automotive market accounts for 33%, and the industry equipment market accounts for 17% of net sales.

In Magnetic Sensors, sales of TMR sensors increased for smartphone applications, and whose demand is expected to continue to grow in the future as cameras become more sophisticated. TMR Sensors have been adopted not only for smartphone applications but also as angle sensors and current sensors used for motors, such as electric power steering, brakes, etc., in automotive applications. In order to respond to growing demand for these applications, we will continue to make aggressive investment for increased production.

Since demand for Temperature and Pressure Sensors and Hall Sensors in Magnetic Sensors is expected to increase in line with the evolvement of EVs, vehicle electrification and automated driving technologies, we will continue to expand sales in the future. We will also continue to promote the expansion of the customer base and applications for MEMS Motion Sensors and MEMS Microphones as in the past.

In the Magnetic Application Products segment, the production volume of HDD Heads has been sluggish in the short term. However, looking ahead to business growth over the medium to long term, we will expand the production of MAMR Heads and continue the development of HAMR as a next-generation technology. In the Magnet business, which is a business with problems, we will continue to improve productivity.

In the Energy Application Products segment, JVs with CATL in the medium-sized rechargeable batteries market have progressed as planned. Recently, demand related to residential energy storage systems has been growing rapidly against the backdrop of concerns over power supply due to heightened geopolitical risks resulting from Russia’s invasion of Ukraine. We will also endeavor to incorporate demand which is expected to grow in the future, such as batteries for electric motorcycle and drone applications.

While there have been growing concerns over the slowdown of the global economy in the short term, we will aim to increase our corporate value over the medium to long term by thoroughly implementing the measures we have just explained.

This concludes my presentation. Thank you very much for your attention.