[ 1st Quarter of fiscal 2019 Performance Briefing ]Consolidated Results for 1Q of FY March 2019

Mr. Tetsuji Yamanishi

Senior Vice President

Hello, I’m Tetsuji Yamanishi, Senior Vice President of TDK. Thank you for taking the time to attend TDK’s performance briefing for the first quarter (April to June) of the fiscal year ending March 2019. I will be presenting an overview of our consolidated results.

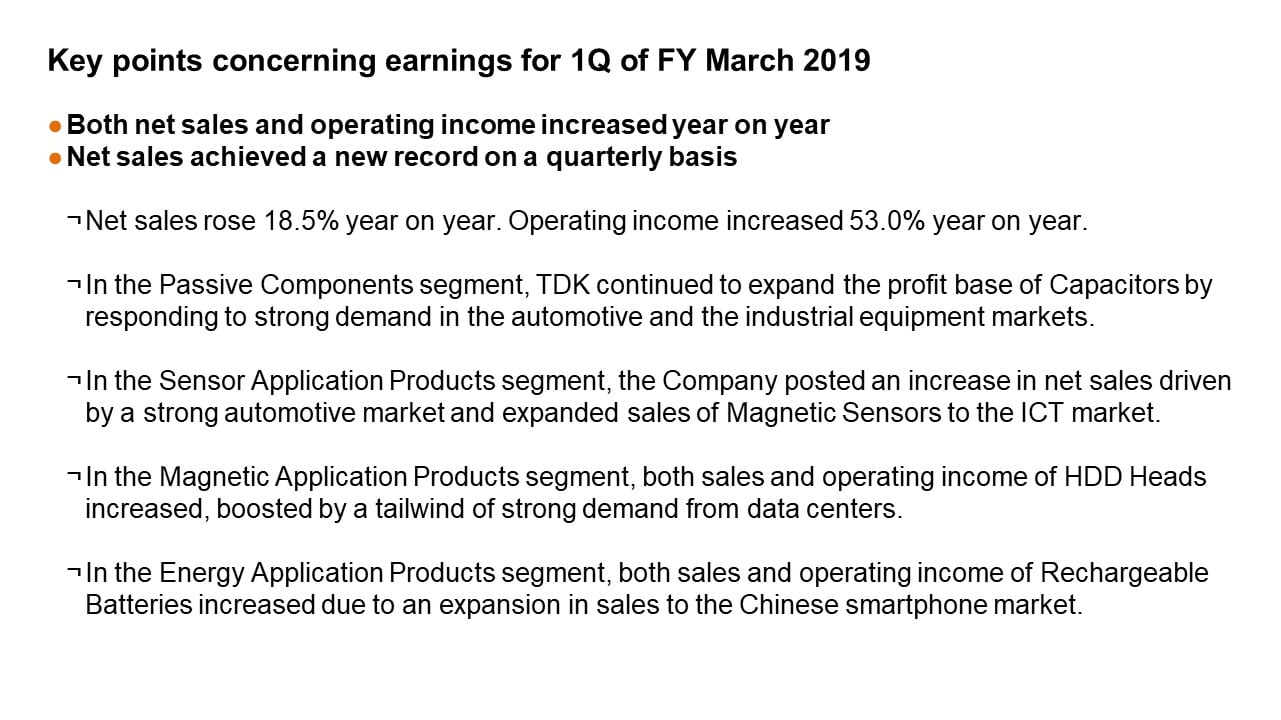

Key points concerning earnings for 1Q of FY March 2019

First, let’s take a look at the key points concerning earnings. Net sales rose 18.5% year on year, and operating income increased sharply by 53.0%. Net sales achieved a new record on a quarterly basis, surpassing the previous record set in the third quarter of the previous fiscal year.

In the Passive Components segment, sales of Capacitors continued to increase favorably in the automotive and industrial equipment markets, where demand has remained strong. Notably, in MLCCs, TDK saw continued growth in earnings owing to an increase in application products with high reliability and redundancy characteristics for automotive use. This contributed immensely to enhancing the profitability of the Passive Components segment as a whole.

In the Sensor Application Products segment, the Company posted an increase in net sales atop higher sales of Magnetic Sensors to the ICT market, as well as firm sales of Temperature and Pressure Sensors and Magnetic Sensors to the automotive market.

In the Magnetic Application Products segment, total HDD market demand decreased by approximately 3% year on year. In this business environment, sales volume of 2.5-inch HDD Heads for PCs decreased. Meanwhile, sales of Nearline HDD Heads increased, boosted by a tailwind of higher demand from data centers. As a result, the product mix improved and both sales and operating income of HDD Heads increased, despite a decline of around 7% in sales volume.

In the Energy Application Products segment, in Rechargeable Batteries, we firmly addressed an increase in orders and related needs due to the launch of new smartphone models by major Chinese customers and the launch of production after inventory adjustments. Sales for applications other than smartphones such as tablets, laptop PCs, and game consoles continued to trend favorably. Coupled with the benefits of higher capacity utilization due to increased production and cost savings, we posted sharp increases in both sales and operating income.

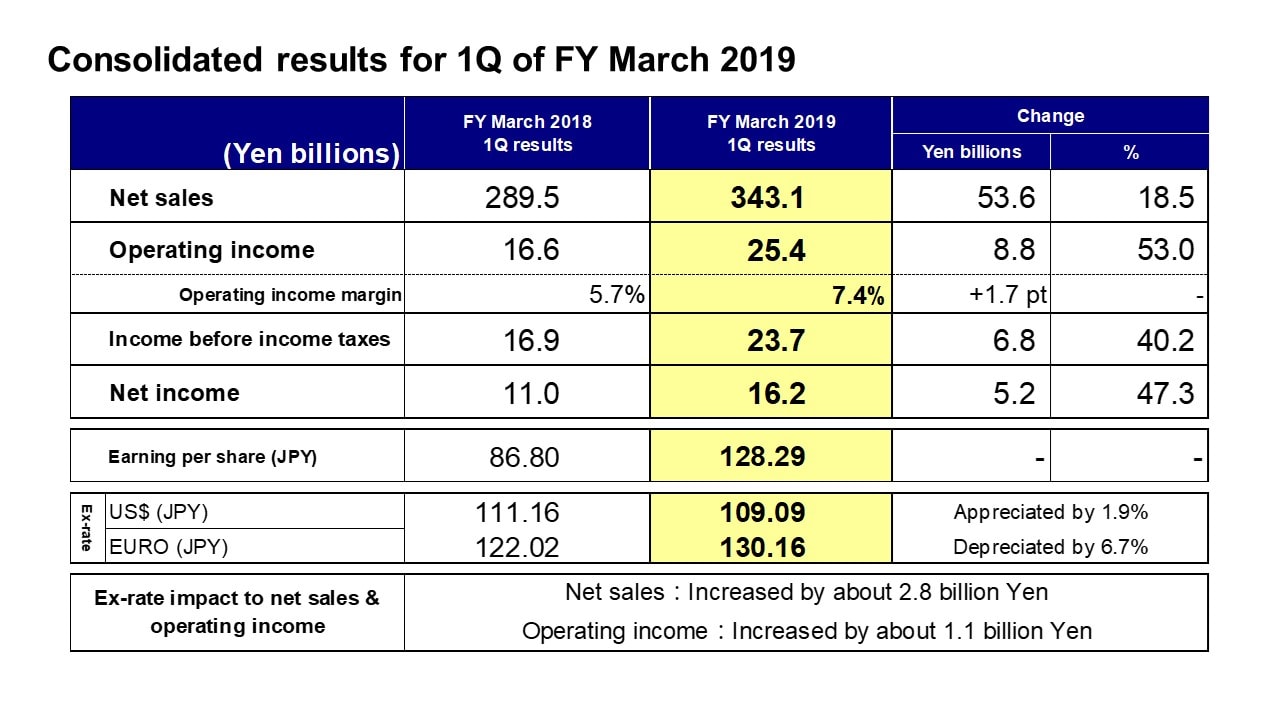

Consolidated results for 1Q of FY March 2019

Moving along, I would like to present an overview of our results. Net sales were 343.1 billion yen, an increase of 53.6 billion yen, or 18.5%, year on year. Operating income was 25.4 billion yen, up 8.8 billion yen, or 53.0%, year on year. Income before income taxes was 23.7 billion yen, net income was 16.2 billion yen, and earnings per share were 128.29 yen. In accordance with changes in U.S. accounting standards related to retirement benefit cost, a 964 million yen portion of the net benefit cost included in operating expense in profit/loss in the previous fiscal year was reclassified to other deductions. From the first quarter of the fiscal year ending March 2019, the amounts pertaining to the change in accounting standards have been recorded as other deductions.

The average exchange rates for the first quarter of the fiscal year ending March 2019 were 109.09 yen against the U.S. dollar, an appreciation of 1.9%, and 130.16 yen against the euro, a depreciation of 6.7%. In terms of the impact of these exchange rate movements, net sales and operating income were pushed up by around 2.8 billion yen and around 1.1 billion yen, respectively.

With regard to exchange rate sensitivity, as with our previous estimate, we estimate that a change of 1 yen against the U.S. dollar would have an impact of approximately 1.2 billion yen on operating income, while a change against the euro would have an impact of approximately 0.2 billion yen.

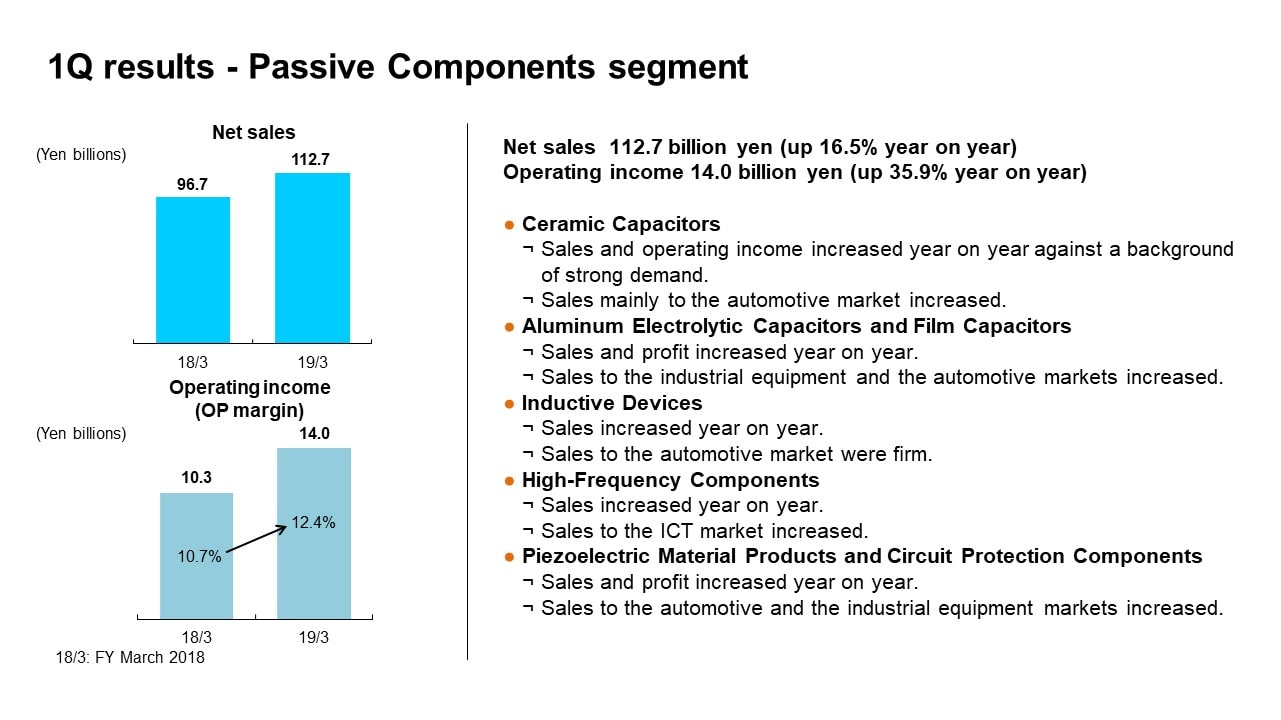

1Q results - Passive Components segment

Next, I would like to explain our business segment performance.

In the first quarter of the fiscal year ending March 2019, we reclassified certain products such as Camera Module Actuators and therefore we regrouped results for the same period of the previous fiscal year. In the Passive Components segment, this change reduced net sales for the first quarter of the fiscal year ended March 2018 by 6.8 billion yen and increased operating income by 0.1 billion yen.

In the first quarter of the fiscal year ending March 2019, net sales were 112.7 billion yen, an increase of 16.5% year on year, and operating income was 14.0 billion yen, an increase of 35.9% year on year. The operating income margin was 12.4%. We made progress on expanding sales and improving profitability.

In Ceramic Capacitors, against the backdrop of surging demand in the automotive market, sales to the automotive market remained solid, increasing year on year. Substantial sales growth was driven by contributions from an improved product mix, including products with high reliability and redundancy characteristics, and from productivity enhancements, which also led to a large improvement in profitability. In Aluminum Electrolytic Capacitors and Film Capacitors, sales and profit increased year on year, underpinned by growth in sales to the industrial equipment market, including renewable energy applications, as well as solid sales to the automotive market. In Inductive Devices, sales increased firmly on the back of a higher sales mix to the automotive market against the backdrop of rising demand from the automotive market.

In High-Frequency Components, sales increased year on year atop favorable sales of ceramic filters for Chinese smartphones. In Piezoelectric Material Products and Circuit Protection Components, sales to the automotive and industrial equipment markets trended favorably, leading to higher sales and profits with improved profitability.

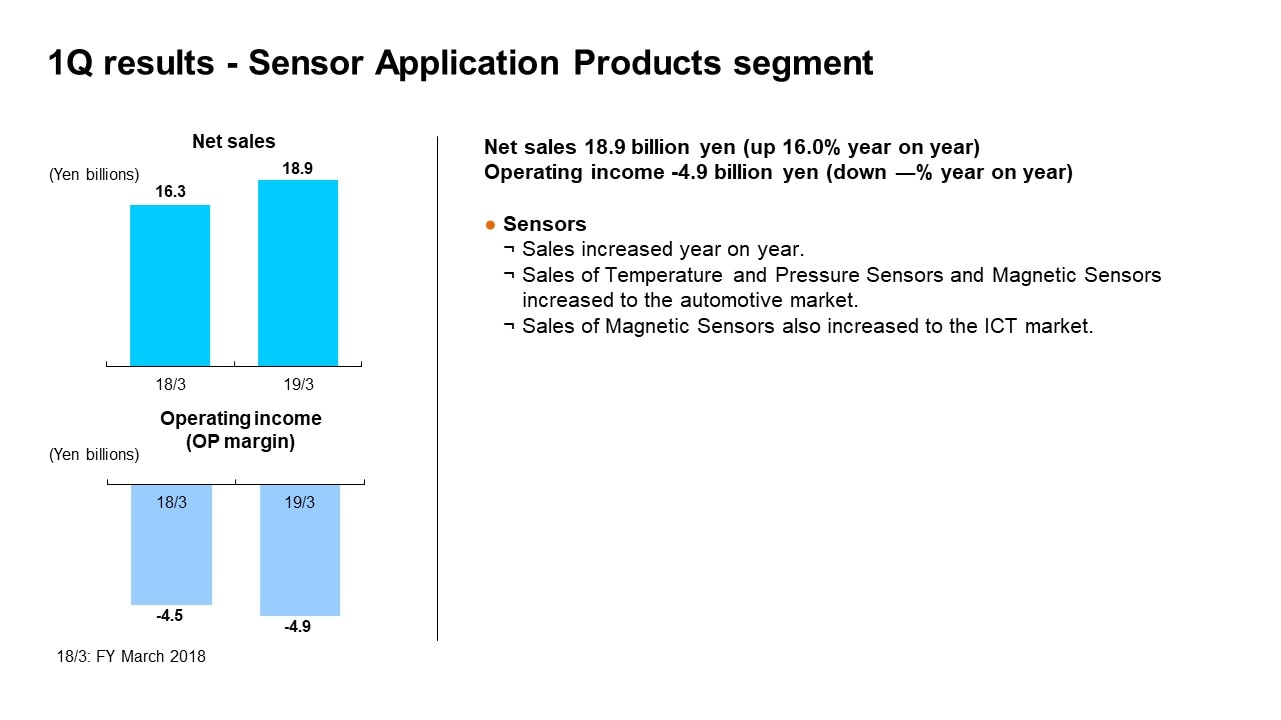

1Q results - Sensor Application Products segment

In the Sensor Application Products segment, the reclassification of certain products reduced net sales for the first quarter of the fiscal year ended March 2018 by 0.1 billion yen and increased operating income by 0.1 billion yen.

In the first quarter of the fiscal year ending March 2019, net sales were 18.9 billion yen, up 16.0% year on year. There was a decrease of 0.4 billion yen in the operating loss from the first quarter of the previous fiscal year, despite a decrease of 2.1 billion yen in acquisition-related costs for InvenSense.

Sales to the automotive market rose around 19% centered on sales of Temperature and Pressure Sensors as well as Magnetic Sensors to the European and Japanese markets. Sales to the ICT market increased by around 4% mainly due to growth in sales of Magnetic Sensors, and the profitability of Magnetic Sensors improved. MEMS motion sensors saw an increase in sales to the industrial equipment market, particularly drones. Meanwhile, there was a larger operating loss due to the cost burden imposed by development resources reflecting the acceleration of application development for newly developed products such as ultrasonic authentication sensors, as well as initiatives to expand the customer base, along with an anticipated decrease in sales to core customers in the ICT market.

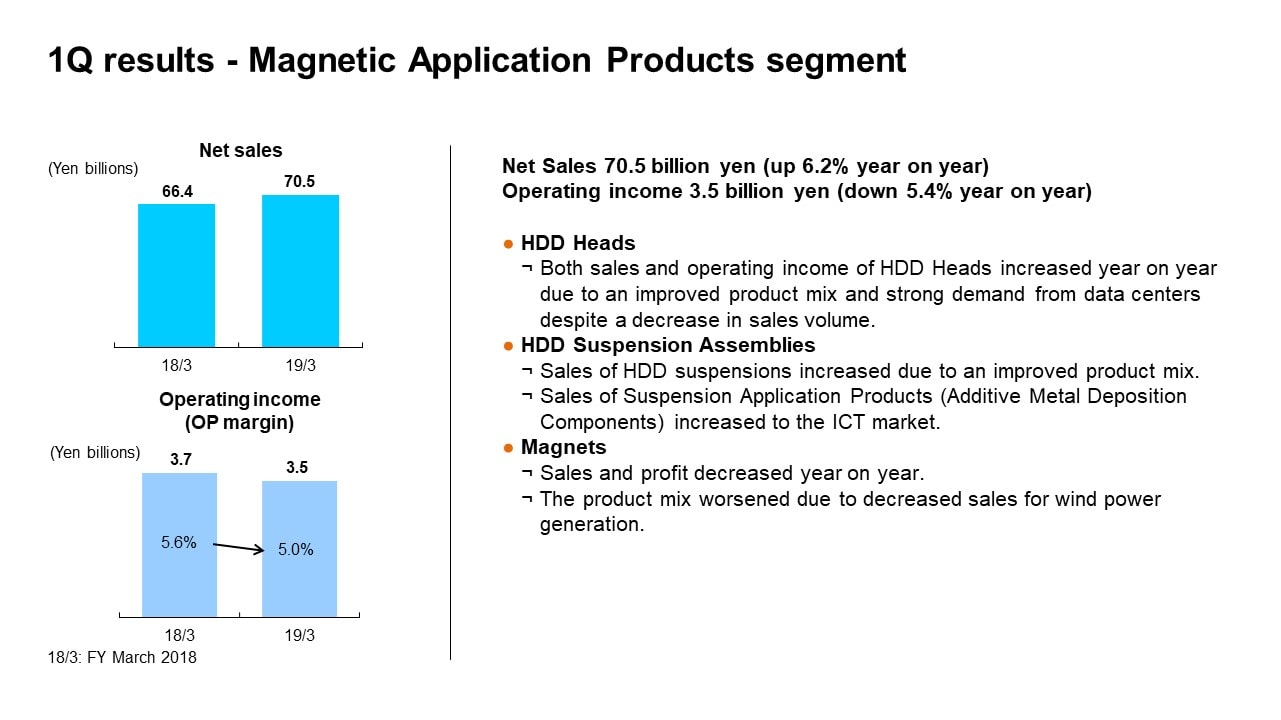

1Q results - Magnetic Application Products segment

In the Magnetic Application Products segment, the reclassification of businesses in connection with a reorganization reduced net sales and operating income for the first quarter of the fiscal year ended March 2018 by 13.6 billion yen and 1.1 billion yen, respectively.

In the first quarter of the fiscal year ending March 2019, net sales rose 6.2% year on year to 70.5 billion yen, operating income decreased by 5.4% to 3.5 billion yen, and the operating income margin was 5.0%.

Sales volume of HDD Heads decreased by around 7%. However, sales of Nearline HDD Heads increased due to higher HDD demand from data centers. Sales increased by around 7%, along with an improvement in profitability, owing to the benefits of a higher average sales price in line with an improved product mix. Sales volume of HDD Suspensions were mostly flat. However, sales of Suspension Application Products (Additive Metal Deposition Components) increased to the ICT market, leading to an overall increase of 9% in sales. However, operating income was impacted by product launch losses on Suspension Application Products.

In Magnets, sales and profit decreased year on year, partly reflecting a worsening product mix due to decreased sales for wind power generation.

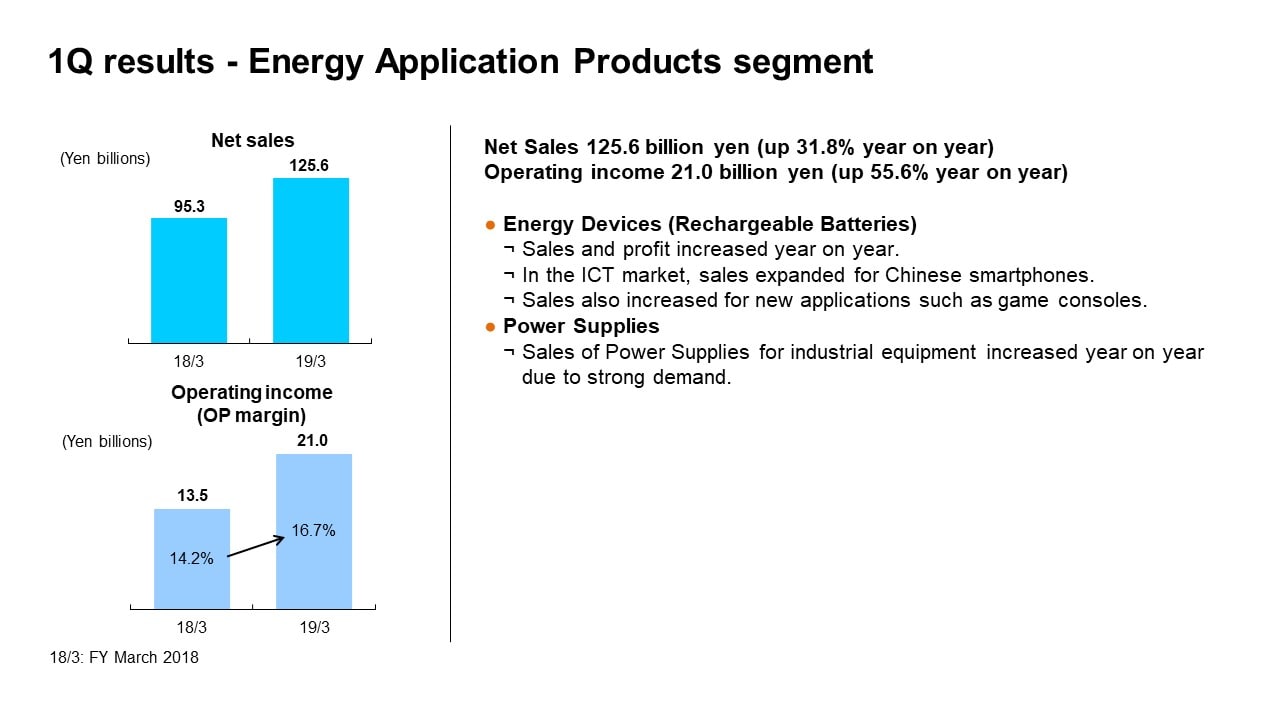

1Q results - Energy Application Products segment

In the Energy Application Products segment, the Power Supply business for industrial equipment and the automotive Power Supply business were integrated into the segment as Energy Application Products, in addition to the existing Rechargeable Battery business. This integration increased net sales for the first quarter of the fiscal year ended March 2018 by 15.6 billion yen and operating income by 0.8 billion yen.

In the first quarter of the fiscal year ending March 2019, net sales rose 31.8% year on year to 125.6 billion yen and operating income surged 55.6% to 21.0 billion yen. Profitability also stayed strong, with the operating income margin at 16.7%.

In Rechargeable Batteries, sales to the Chinese smartphone market increased sharply, and sales were also higher for applications other than smartphones, such as tablets, laptop PCs, and game consoles. By capturing synergies between growth in sales volume and increased productivity, we have effectively enhanced profits.

Power Supplies for industrial equipment generated steady profits due to strong demand.

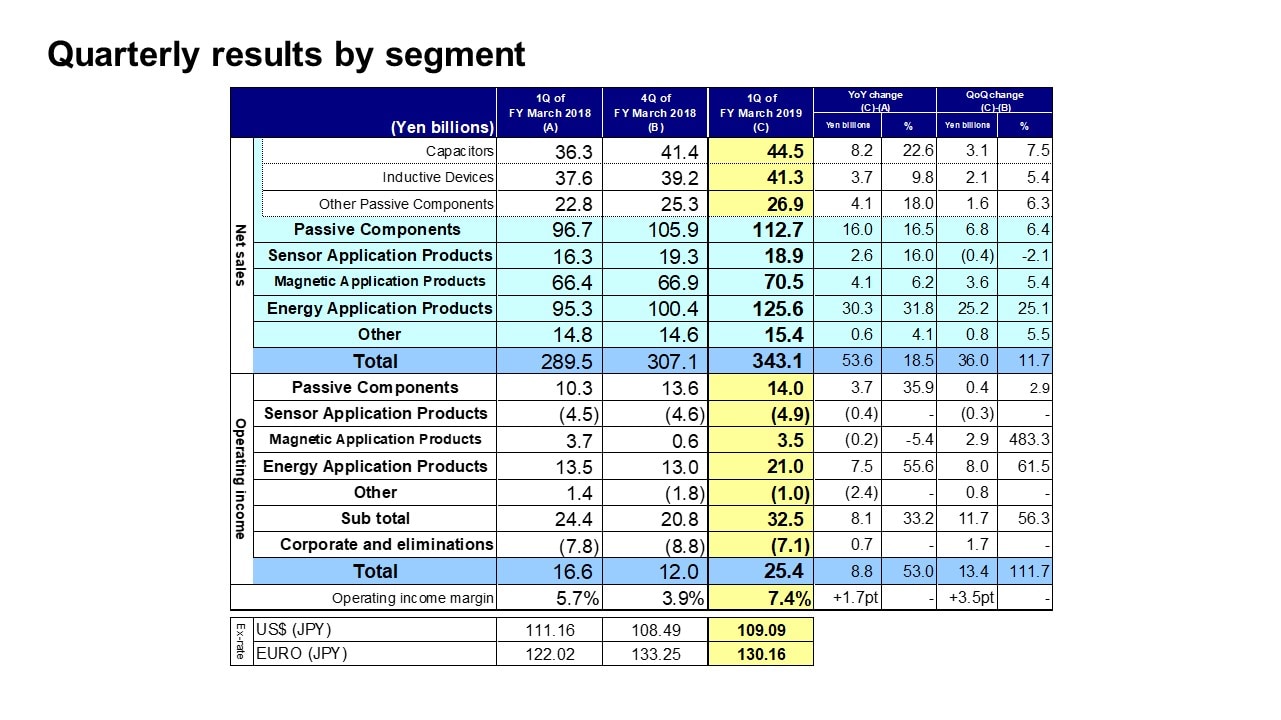

Quarterly results by segment

Next, I would like to explain the factors behind the changes in segment net sales and operating income from the fourth quarter of the fiscal year ended March 2018 to the first quarter of the fiscal year ending March 2019. As I explained earlier, we have reclassified net sales and operating income for the previous fourth quarter into the new reporting segment framework to reflect the establishment of the new segment and the reclassification of certain products.

Let’s begin with the Passive Components segment. In this segment, net sales in the first quarter increased by 6.8 billion yen, or 6.4%, from the fourth quarter. Ceramic Capacitor sales were strong to the automotive market. Also, Aluminum Electrolytic Capacitors and Film Capacitors drove higher sales for use in the renewable energy market. As a result, sales of Capacitors increased by 3.1 billion yen, or 7.5%, from the fourth quarter. Sales of Inductive Devices rose by 2.1 billion yen, or 5.4%, from the fourth quarter. As with Ceramic Capacitors, sales to the automotive market were strong, and sales for Chinese smartphones increased. In Other Passive Components, sales increased by 1.6 billion yen, or 6.3%, from the fourth quarter. In High-Frequency Components, sales of Ceramic Filters for Chinese smartphones increased from the fourth quarter, along with higher sales of Piezoelectric Material Products and Circuit Protection Components to the industrial equipment market.

Operating income in the Passive Components segment increased by 0.4 billion yen, or 2.9%, from the fourth quarter. The main contributing factors were higher profits from increased sales volume and enhanced productivity in Ceramic Capacitors, plus higher sales and profits in Inductive Devices.

In the Sensor Application Products segment, net sales decreased by 0.4 billion yen, or 2.1%, from the fourth quarter. Sales of MEMS Sensors to the ICT market decreased due to the impact of inventory adjustments and lower demand for use in industrial equipment and game consoles, despite an increase in sales of Magnetic Sensors to the ICT market.

In the Sensor Application Products segment, there was a decrease in the operating loss of 0.3 billion yen. The operating loss was sharply reduced by a decrease of 0.1 billion yen in acquisition-related costs for InvenSense and higher earnings from increased sales of Magnetic Sensors. However, these positive factors were outweighed by negative factors including lower sales of MEMS sensors and higher fixed costs due to the acquisition of Chirp Microsystems, Inc., resulting in an overall decrease in earnings.

In the Magnetic Application Products segment, net sales increased by 3.6 billion yen, or 5.4%, from the fourth quarter. HDD Head sales rose by 11% atop higher HDD Head shipments and an improved product mix. In HDD Suspension Assemblies, sales declined partly due to lower demand for Additive Metal Deposition Components, despite mostly flat sales of HDD Suspensions. Sales of Magnets decreased by around 5% from the fourth quarter due to a decrease in sales for renewable energy applications.

In the Magnetic Application Products segment, operating income increased by 2.9 billion yen from the fourth quarter. The main factors were the absence of restructuring expenses, a devaluation of HDD Head wafers, and a loss on a reduction in capacity utilization due to the Lunar New Year holidays, all of which were recorded in the fourth quarter, in addition to an increase in earnings from higher sales volume of HDD Heads.

In the Energy Application Products segment, net sales increased by 25.2 billion yen, or 25.1%, from the fourth quarter. In Rechargeable Batteries, orders grew for use in new Chinese smartphone models and a timely response was made to the launch of production after inventory adjustments in the fourth quarter, resulting in a large increase in overall net sales.

Operating income in the Energy Application Products segment was 21.0 billion yen, an increase of 8.0 billion yen from 13.0 billion yen in the fourth quarter. Profit grew sharply due to a rise in marginal profit from higher sales volumes and cost improvements, in addition to the absence of the loss on reduced capacity utilization due to the Lunar New Year holidays.

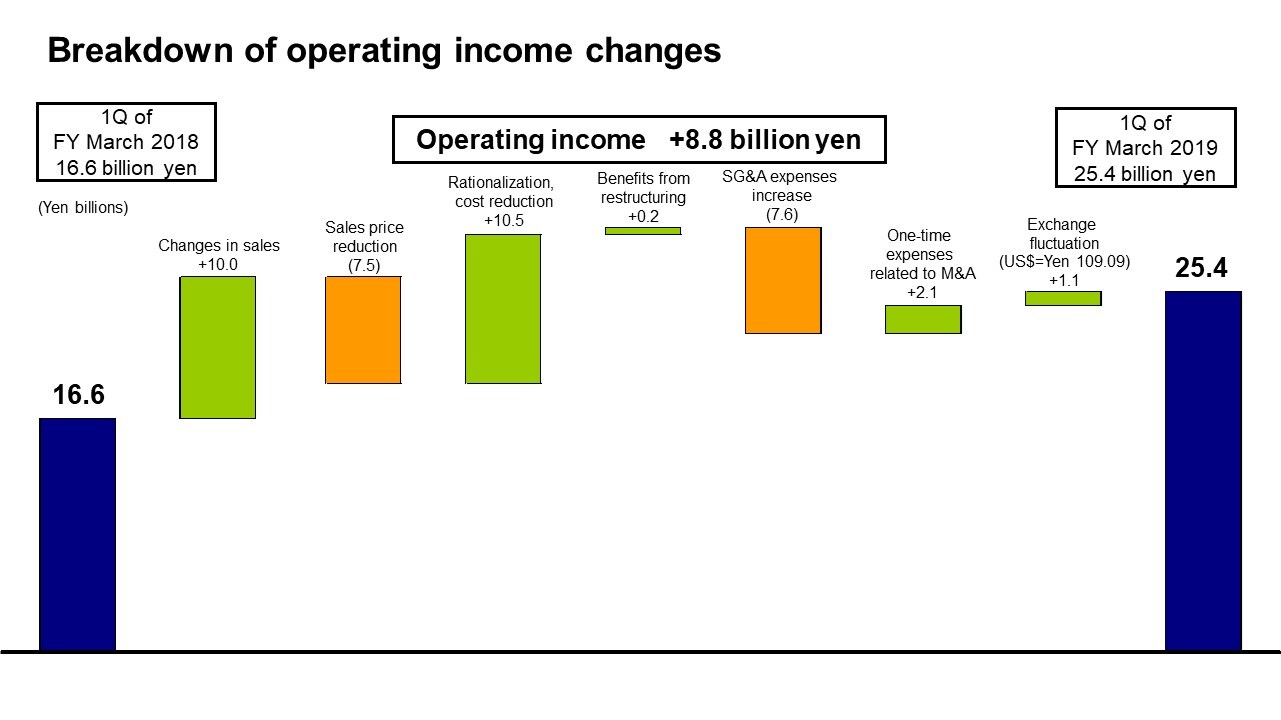

Breakdown of operating income changes

Next is the breakdown of the change in operating income. Let’s take a look at the main factors behind the increase of 8.8 billion yen in operating income. First, there was a positive impact of around 10.0 billion yen from an increase in net sales centered on Capacitors, HDD Heads, and Rechargeable Batteries. Reductions in sales prices had a negative impact of around 7.5 billion yen, but this was absorbed by the positive impact of 10.5 billion yen from rationalization and cost reduction. We recorded around 0.2 billion yen in benefits from restructuring implemented in the fourth quarter of the previous fiscal year and a positive impact of around 2.1 billion yen from the decrease in acquisition-related costs for InvenSense. However, SG&A expenses increased by 7.6 billion yen due to increases in administration and development expenses in connection with business expansion in Rechargeable Batteries, as well as higher costs arising from strengthening the development framework in the Sensor business. Including a positive impact of 1.1 billion yen from exchange rate fluctuations, operating income increased by 8.8 billion yen.

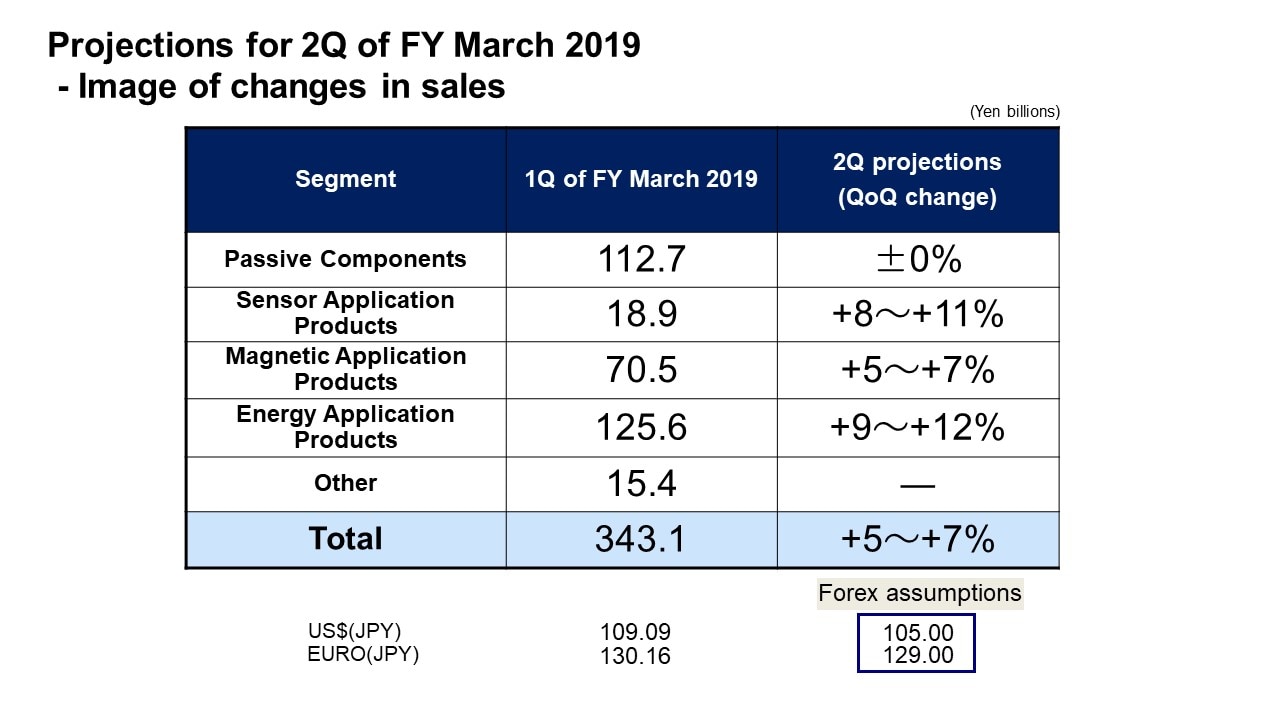

Projections for 2Q of FY March 2019- Image of changes in sales

Let me now discuss our image of changes in sales for the second quarter of the fiscal year ending March 2019.

First, for the Passive Components segment, we are projecting mostly flat net sales from the first quarter. In MLCCs, we are addressing increased demand by operating at full production capacity and expect sales to remain mostly on par with the first quarter. In Inductive Devices and High-Frequency Components, demand is expected to increase on the back of the launch of new devices in North America. Meanwhile, demand is expected to decrease for Aluminum Electrolytic Capacitors and Film Capacitors due to the impact of the reduction of purchase prices for renewable energy in China. Based on these factors, we anticipate overall net sales in the Passive Components segment to remain mostly flat.

In the Sensor Application Products segment, we are projecting a net sales increase of 8-11%. We anticipate an increase in sales of Magnetic Sensors due to the launch of new devices in North America, and an increase in sales of MEMS Sensors for smartphone applications.

In the Magnetic Application Products segment, we are projecting a net sales increase of 5-7%. We expect HDD Head sales volume to increase by around 8% and HDD Suspension sales volume to increase by around 14%. In addition, sales of Additive Metal Deposition Components are expected to increase. In Magnets, overall sales are expected to remain mostly flat, despite changes in the product mix.

In the Energy Application Products segment, we are projecting net sales growth of 9-12%. In Rechargeable Batteries, demand for Chinese smartphones is expected to slow down slightly compared to the pace in the first quarter. Meanwhile, overall sales are projected to increase due to the launch of new devices in North America. Sales of Power Supplies are forecast to remain mostly unchanged.

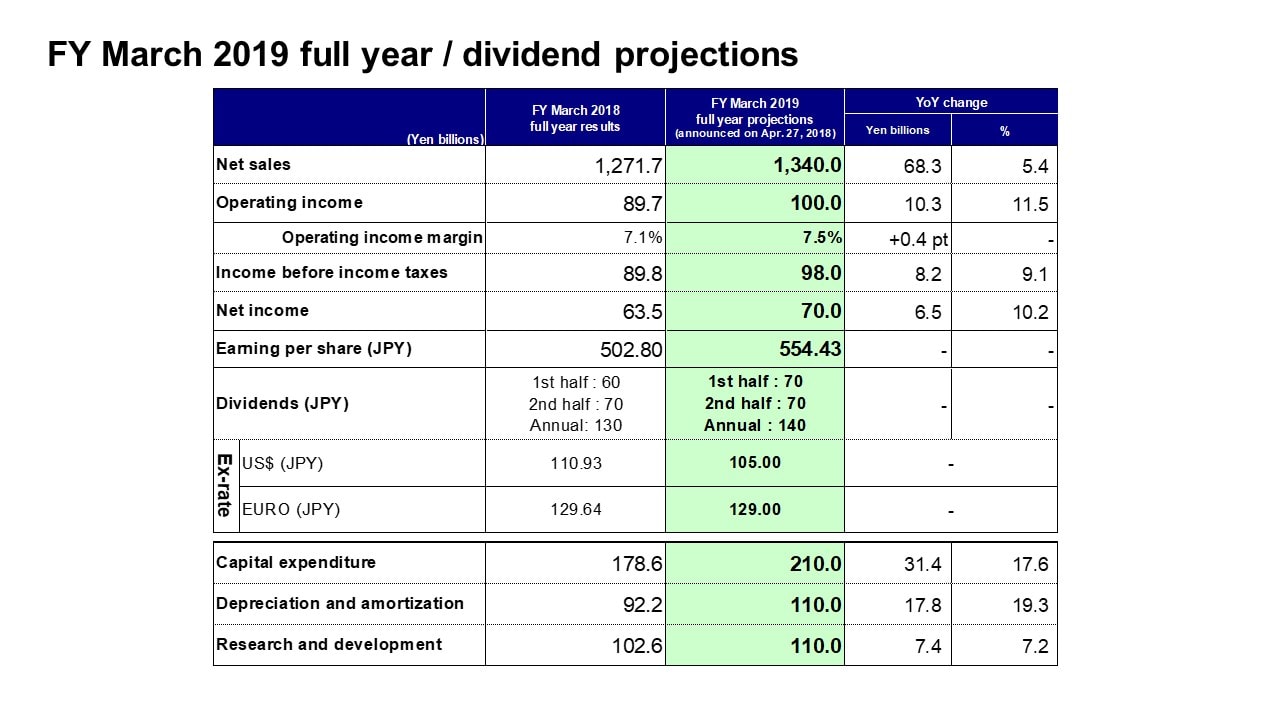

FY March 2019 full year / dividend projections

Finally, I would like to discuss our consolidated full-year projections for the fiscal year ending March 2019. We have maintained the full-year projections announced in April.

We finished the first quarter with stronger-than-expected results in comparison to the levels assumed in our full-year projections. However, the outlook for trends in the ICT market, which have a significant bearing on results, still presents uncertainties in the second half of the fiscal year. The impact of trade friction and exchange rate trends are also uncertain. Factoring in a conservative outlook, we have decided to maintain our projections. We will consider revising the full-year projections when we are able to predict trends in the business environment with greater accuracy.

That concludes my presentation. Thank you very much for your attention.