2nd Quarter of fiscal 2024 Performance Briefing

H1, FY March 2024 Results Highlights

Mr. Tetsuji Yamanishi

Executive Vice President

Hello, I am Tetsuji Yamanishi, Executive Vice President of TDK. Thank you for taking the time to attend TDK’s performance briefing for the first half of the fiscal year ended March 2024. I will be presenting an overview of our consolidated results.

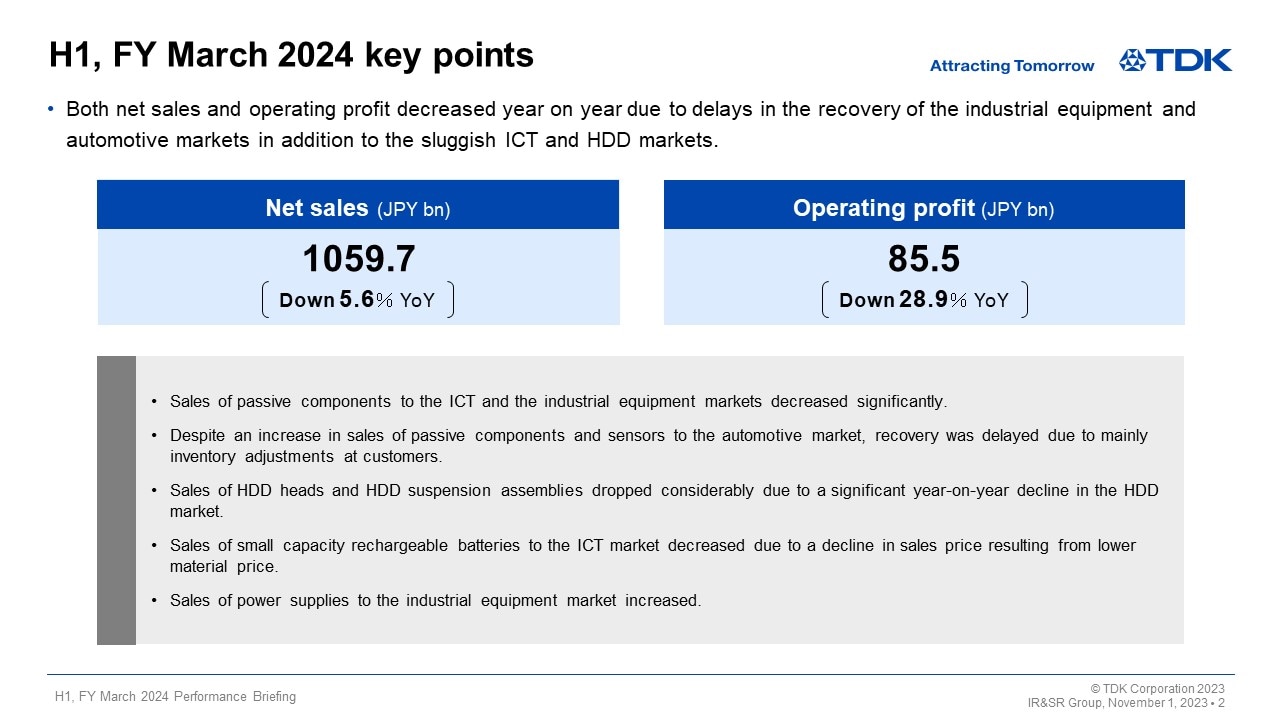

H1, FY March 2024 key points

I will present an overview of our consolidated results. Despite signs of economic recoveries appearing in some regions, the global economy remained unstable during the first half of fiscal 2024 due to regional differences in business confidence, such as sluggishness in Europe due to monetary tightening and an economic slowdown in China driven by a real estate slump. Foreign exchange rates were also affected by these developments, and the depreciation of the yen continued, especially against the U.S. dollar and the euro.

Under such an operating environment, in the electronics market—which has a large bearing on the consolidated performance of TDK—demand recovery was delayed in the industrial equipment and automotive markets, while the prolonged slump in final demand resulted in sluggish ICT and HDD market demand. As a result, net sales were down 5.6% year on year, and operating profit fell by 28.9% year on year.

Looking at sales in each business by market, sales of passive components to the ICT and the industrial equipment markets decreased significantly. Despite an increase in sales of passive components and sensors to the automotive market, demand recovery has been delayed due mainly to inventory adjustments by customers. Sales of HDD heads and HDD suspension assemblies dropped considerably due to a significant year-on-year decline in HDD-related demand. While the sales volume of small capacity rechargeable batteries to the ICT market remained virtually unchanged from the previous fiscal year, sales decreased year on year due mainly to a decline in sales prices resulting from lower material prices. On the other hand, sales of power supplies to the industrial equipment market have remained brisk.

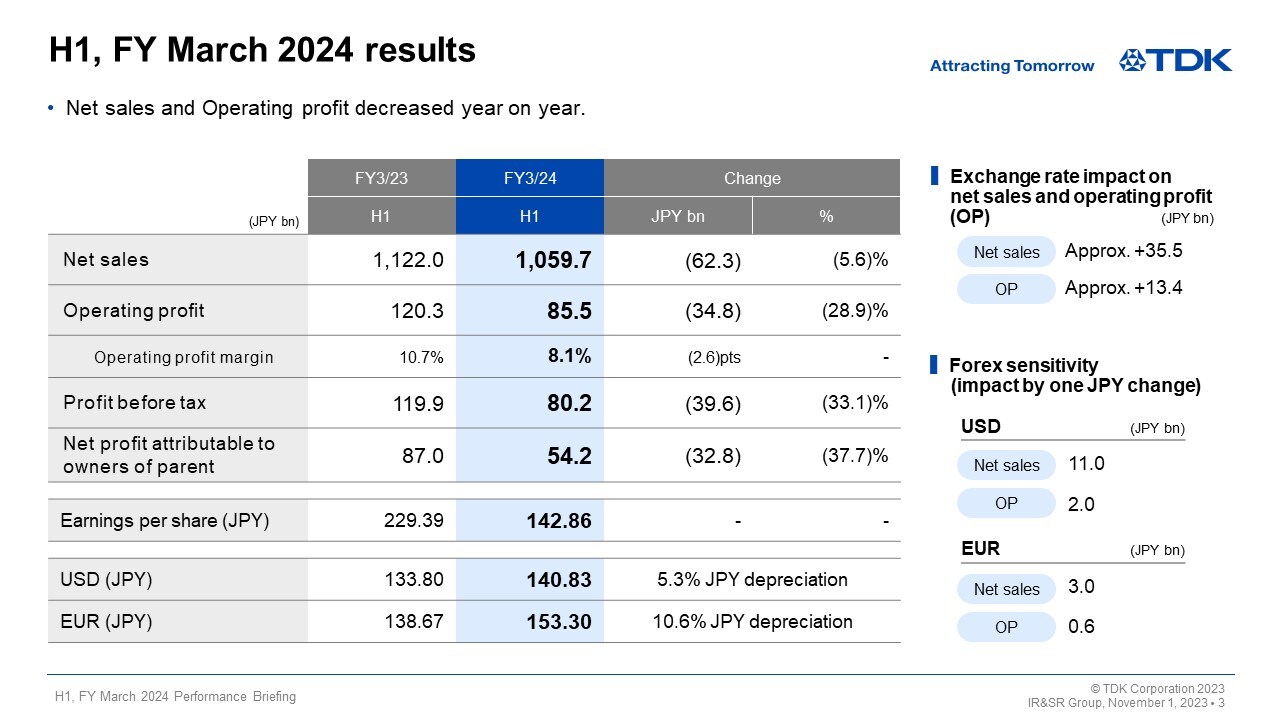

H1, FY March 2024 results

Next, I would like to present an overview of the results for the first half of fiscal 2024.

Due to exchange rate fluctuations against the U.S. dollar and other currencies, there was an increase of about 35.5 billion yen in net sales and an increase of about 13.4 billion yen in operating profit. Including this impact on operating profit, net sales were 1,059.7 billion yen, a decrease of 62.3 billion yen, or 5.6%, year on year. Operating profit was 85.5 billion yen, a decrease of 34.8 billion yen, or 28.9%, year on year. Profit before tax was 80.2 billion yen, and net profit attributable to owners of parent was 54.2 billion yen. Earnings per share were 142.86 yen.

With regard to exchange rate sensitivity and operating profit, we maintain our estimate that a change of one yen against the U.S. dollar will affect operating profit by about 2.0 billion yen a year, while a one yen change against the euro will have an impact of about 0.6 billion yen a year.

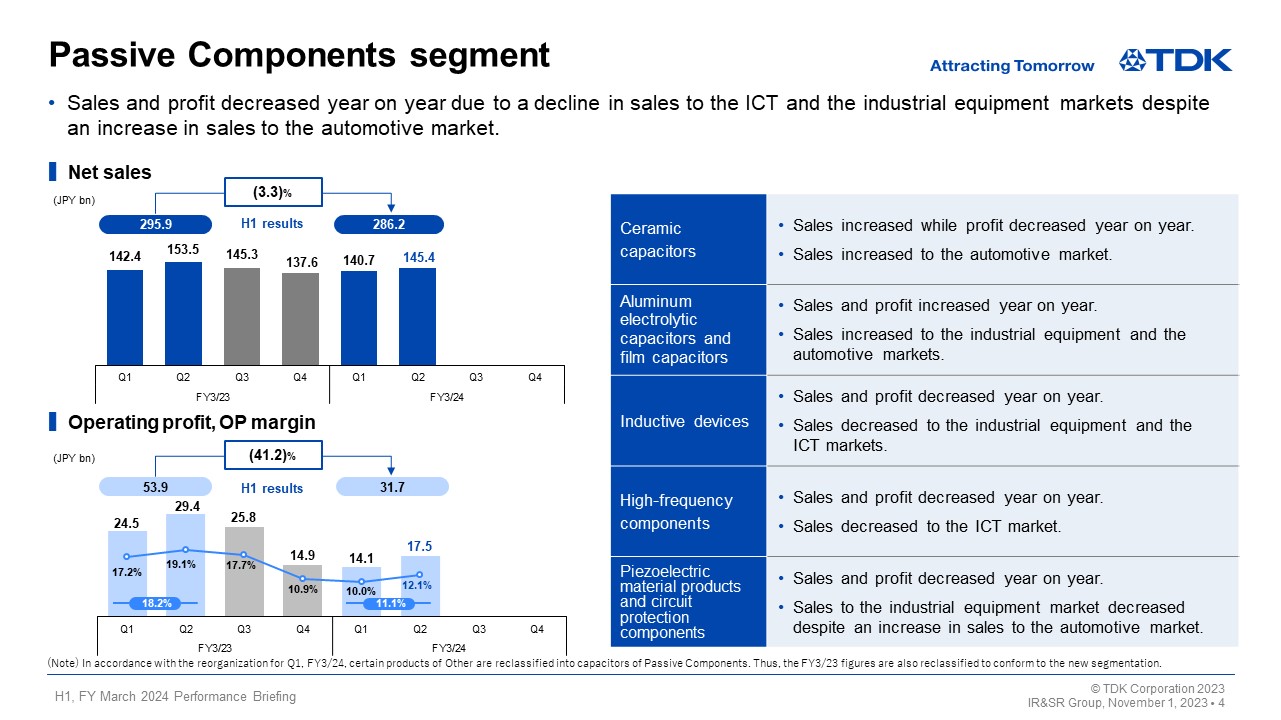

Passive Components segment

Next, I would like to explain our business segment performance for the first half of fiscal 2024.

Net sales in the Passive Components segment were 286.2 billion yen, a decrease of 3.3% year on year. Operating profit was down 41.2% year on year, due to a decline in sales to the ICT and industrial equipment markets, despite an increase in sales to the automotive market, especially for sales related to xEVs.

While sales to the automotive market increased across all businesses, performance in each business varied due to the difference in amount of orders from other markets and by application.

While sales of ceramic capacitors increased year on year, driven by a rise in sales to the automotive market, profit decreased year on year due mainly to the deterioration in the product mix. Sales and profits of aluminum electrolytic capacitors and film capacitors increased on a year on year basis, reflecting brisk long-term orders from the industrial equipment market on top of those from the automotive market. Sales and profits of inductive devices, high-frequency components, and piezoelectric material products / circuit protection components decreased year on year due to a decline in sales to the ICT and industrial equipment markets as well as to distributors.

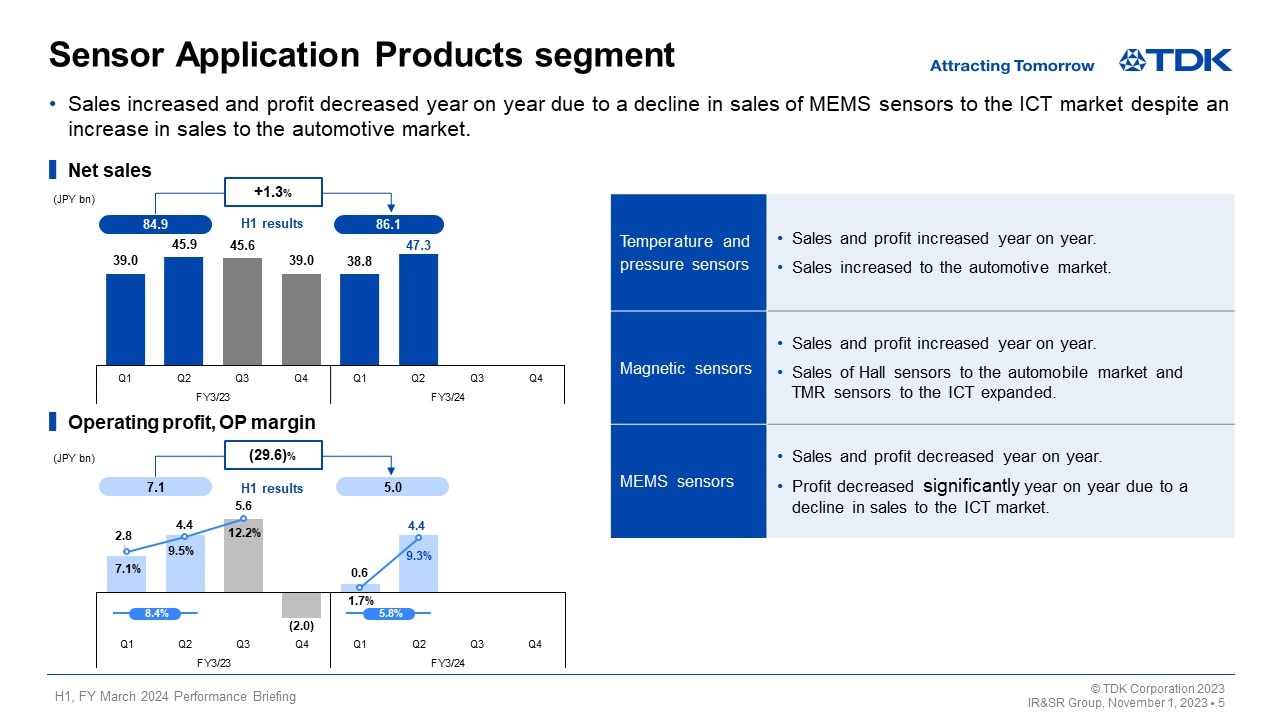

Sensor Application Products segment

Net sales in the Sensor Application Products segment amounted to 86.1 billion yen, up 1.3% year on year. Operating profit was 5.0 billion yen, down 29.6% year on year.

Sales and profits of temperature and pressure sensors increased year on year, reflecting a rise in sales to the automotive market. Sales and profits of magnetic sensors increased year on year as sales of Hall sensors increased to the automotive market and sales of TMR sensors for smartphone applications remained brisk. On the other hand, sales and profits of MEMS sensors decreased year on year due to a drop in sales to the ICT market, despite an expansion of sales of motion sensors to the automotive market.

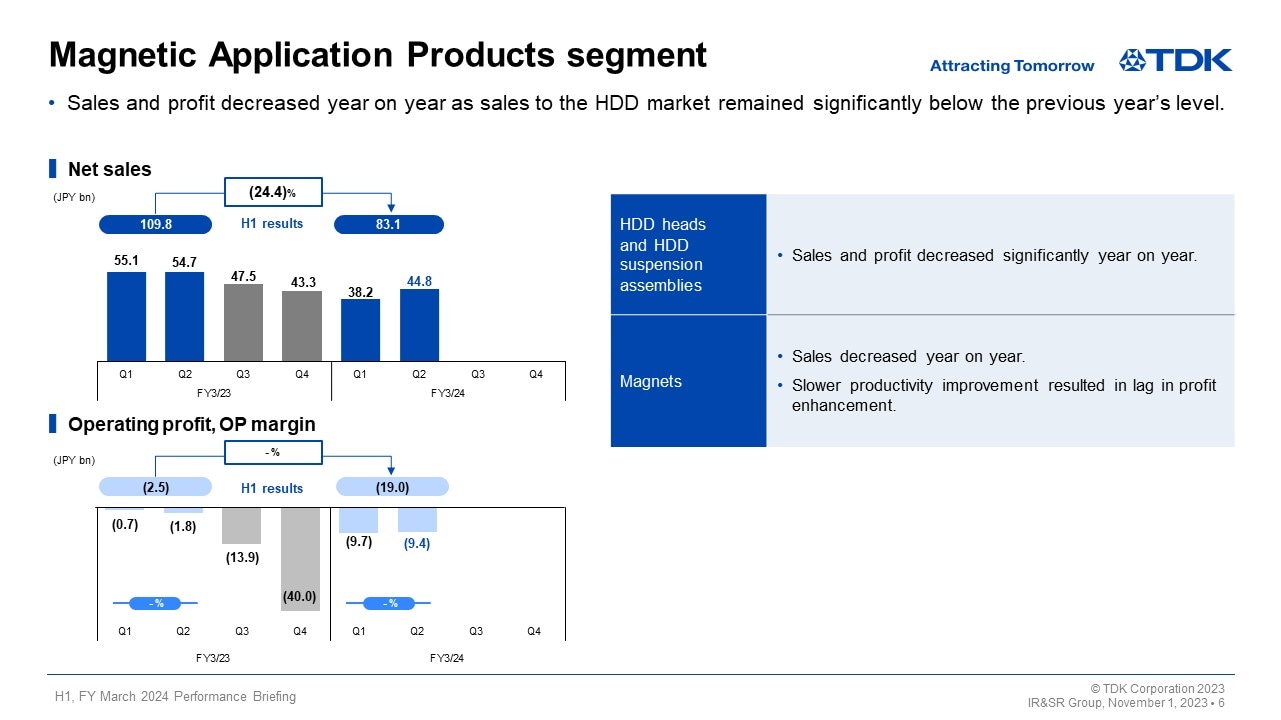

Magnetic Application Products segment

In the Magnetic Application Products segment, net sales fell 24.4% year on year to 83.1 billion yen. In addition, a significant operating loss of 19.0 billion yen was posted.

In HDD heads and HDD suspension assemblies, total demand for HDDs decreased 25% year on year as HDD-related demand remained sluggish. In particular, total demand for nearline HDDs declined 43% year on year. As a result, sales of HDD heads and HDD suspension assemblies dropped significantly, posting a loss, reflecting a substantial year on year decline in sales volume. Restructuring aimed at optimizing production systems has been implemented as scheduled, and restructuring costs of about 0.9 billion yen were posted in the second quarter. Sales of magnets decreased year on year, reflecting a decline in sales for industrial equipment applications despite a rise in sales related to xEVs. In addition, lags in productivity improvements resulted in a slight increase in losses.

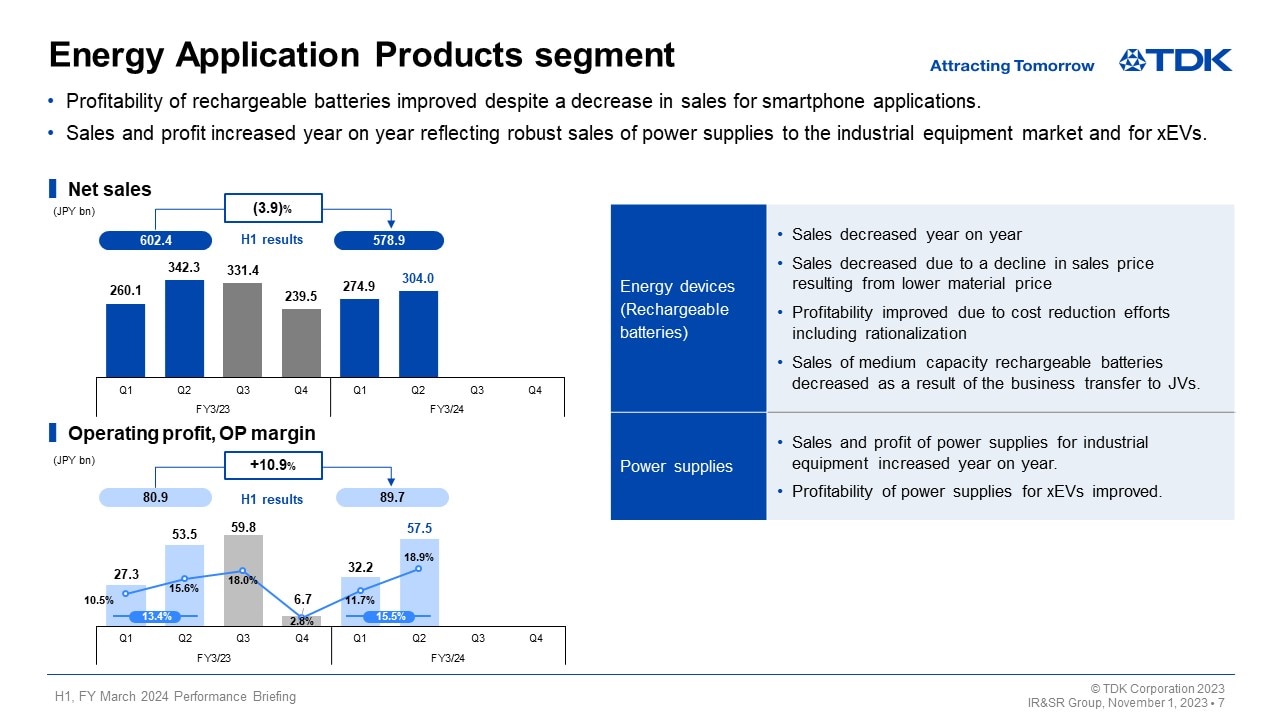

Energy Application Products segment

In the Energy Application Products segment, net sales decreased 3.9% year on year to 578.9 billion yen and operating profit rose 10.9% year on year to 89.7 billion yen.

In energy devices (rechargeable batteries) on the whole, sales and profits decreased year on year. Sales of small capacity rechargeable batteries for smartphone applications decreased year on year due to a decline in sales prices and discounts on selling prices resulting from lower material price, although sales volume remained virtually unchanged from the previous fiscal year. Sales of medium capacity rechargeable batteries also dropped year on year as a result of the progress in business transfer to JVs. On the other hand, an increase in profit was achieved on a year on year basis due to the effect of rationalization and gains from exchange rate fluctuation, despite a year on year decline in sales.

In power supplies for industrial equipment, demand related to industrial equipment such as semiconductor manufacturing equipment, as well as for medical equipment applications, remained robust and resulted in year on year increases in both sales and profits. In power supplies for EVs, losses diminished considerably reflecting the benefits from restructuring at the end of the previous fiscal year on top of a year on year increase in sales.

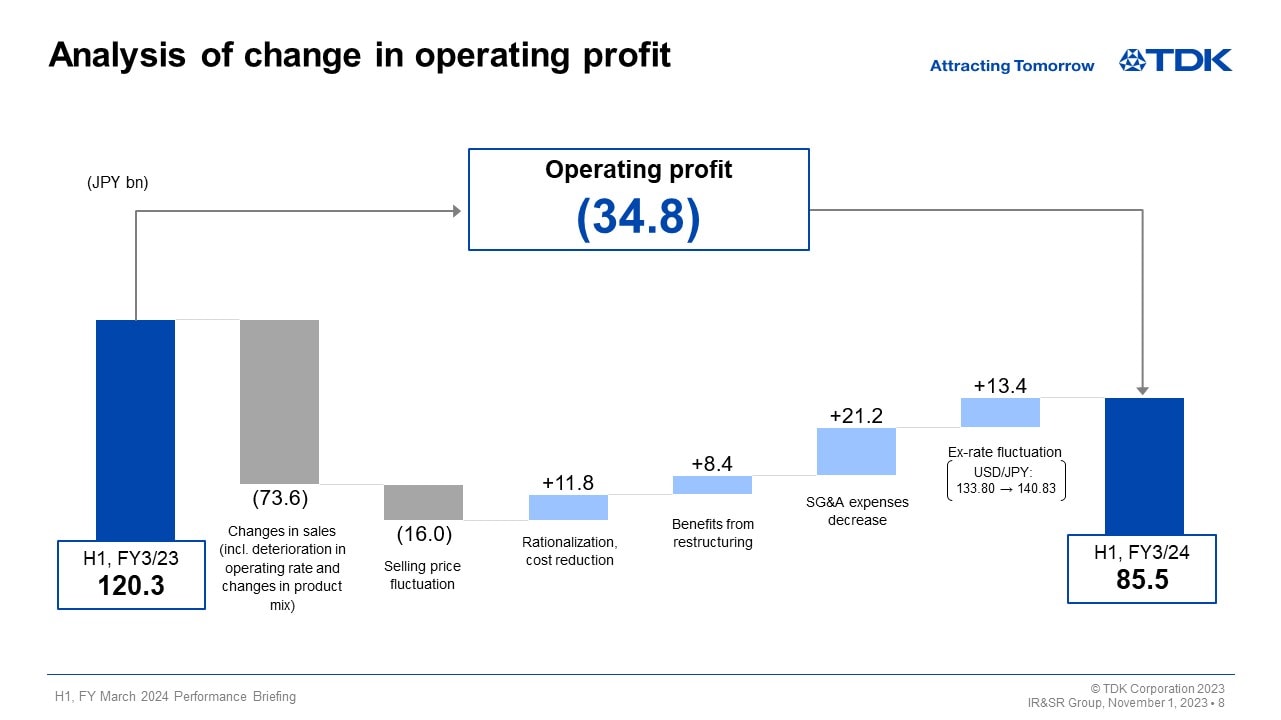

Analysis of change in operating profit

Next is an analysis of changes in operating profit. Let’s take a look at the main factors behind the 34.8 billion yen year on year decrease in operating profit.

First, operating profit decreased 73.6 billion yen due to changes in sales, reflecting a decline in the sales volume of HDD heads and HDD suspension assemblies, deterioration in the product mix of passive components on top of a decline in volume, and deterioration in the product mix of rechargeable batteries. There was also a decrease in profit of 16.0 billion yen due to selling price fluctuations. On the other hand, there were positive effects on operating profit, including the yen’s depreciation amounting to 13.4 billion yen, rationalization and cost reduction efforts mainly for rechargeable batteries and passive components amounting to 11.8 billion yen, benefits from restructuring during the previous fiscal year of 8.4 billion yen, and streamlining of SG&A expenses of 21.2 billion yen. However, these positive effects were not enough to offset the negative impact of the decrease in sales volume.

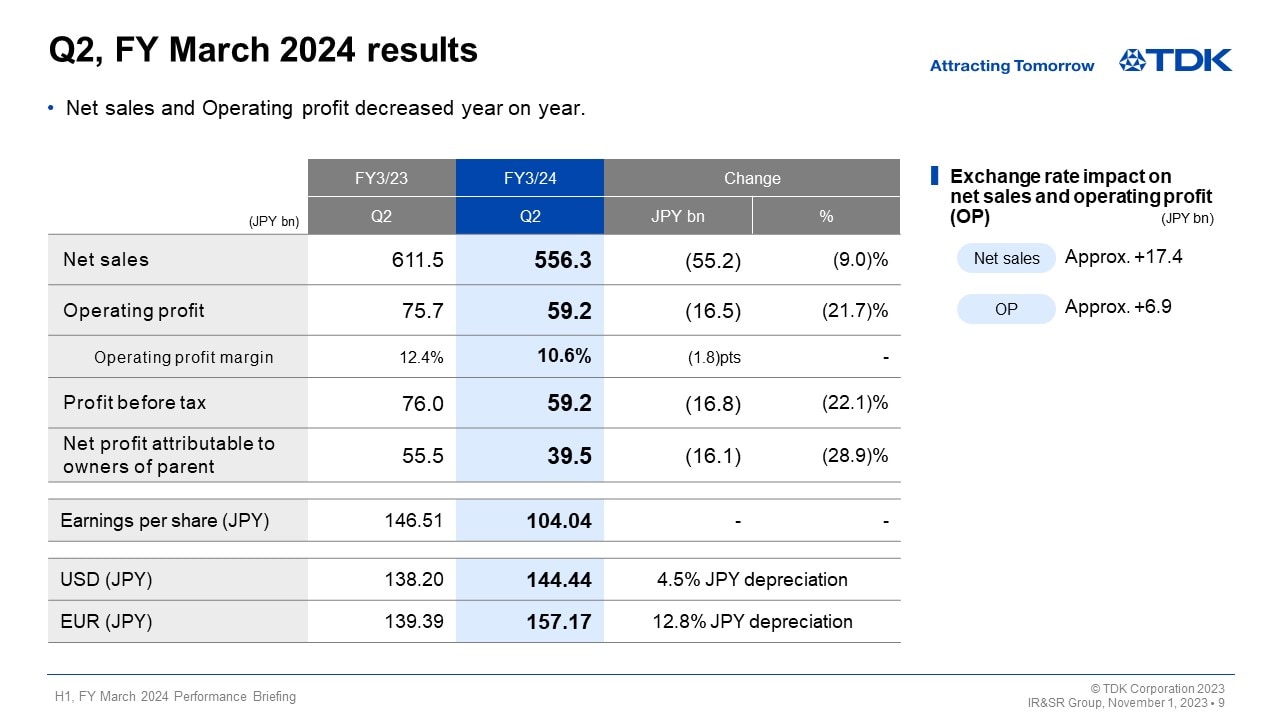

Q2, FY March 2024 results

Next, I would like to present an overview of our consolidated results for the second quarter (three months) of fiscal 2024.

Due to exchange rate fluctuations against the U.S. dollar and other currencies, there was an increase of about 17.4 billion yen in net sales and an increase of about 6.9 billion yen in operating profit. Including this impact on operating profit, net sales were 556.3 billion yen, a decrease of 55.2 billion yen, or 9.0%, year on year. Operating profit was 59.2 billion yen, a decrease of 16.5 billion yen, or 21.7%, year on year. Profit before tax was 59.2 billion yen, and net profit was 39.5 billion yen. Earnings per share were 104.04 yen.

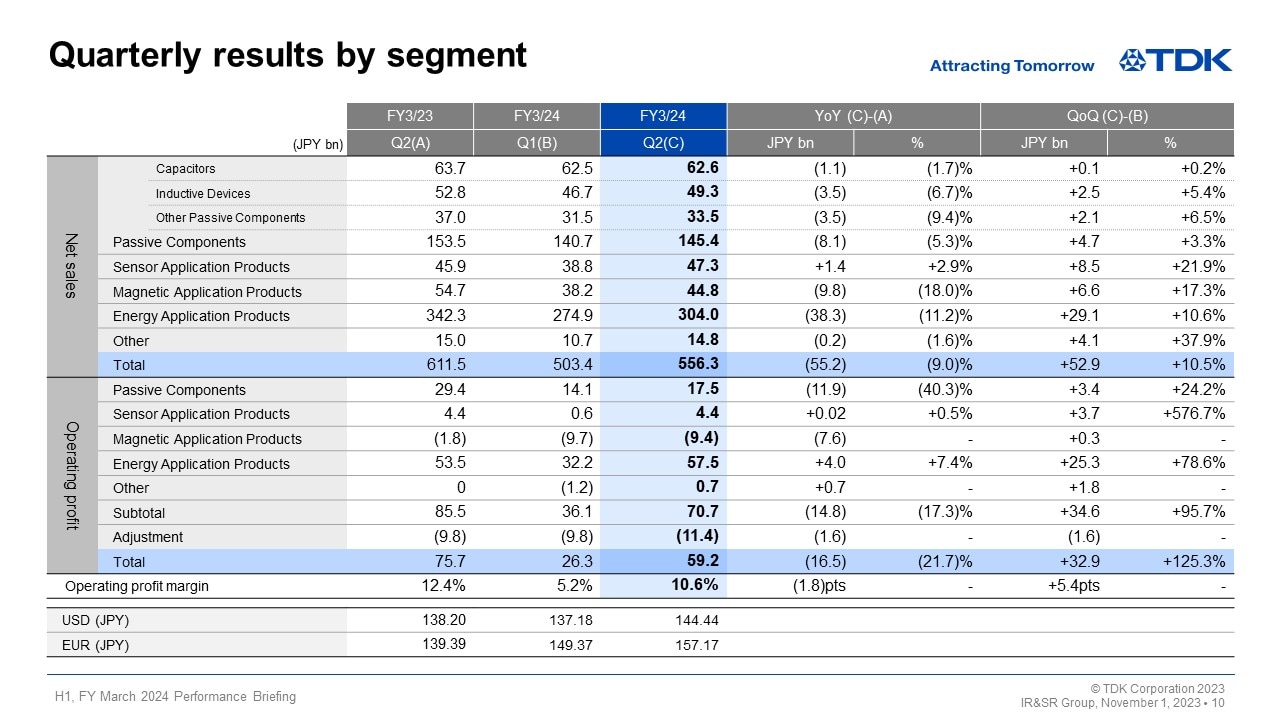

Quarterly results by segment

Now, I will explain some of the factors behind the changes in segment net sales and operating profit from the first quarter to the second quarter of fiscal 2024.

In the Passive Components segment, net sales increased by 4.7 billion yen, or 3.3%, from the first quarter, and operating profit rose by 3.4 billion yen, or 24.2%, from the first quarter. Sales to the automotive market increased across all businesses, and sales to the ICT market, mainly those of inductive devices and high-frequency components, increased as smartphone-related sales have reached a peak. On the other hand, sales to the industrial equipment market as well as to distributors decreased on the whole, due partly to the effect of inventory adjustments. Consequently, overall sales of passive components increased only slightly from the first quarter. Operating profit rose from the first quarter, reflecting the progress in cost improvement initiatives.

In the Sensor Application Products segment, net sales increased by 8.5 billion yen and operating profit rose by 3.7 billion yen from the first quarter. Sales of temperature and pressure sensors to the automotive market remained firm. Sales of magnetic sensors to the ICT market jumped significantly as smartphone-related sales have reached a peak. In particular, sales and profits of TMR sensors increased considerably due partly to the frontloaded orders from the third quarter. Sales of MEMS units on the whole slightly increased and operating profit remained virtually unchanged from the first quarter due to the growth of microphone sales, despite a decline in sales of motion sensors for gaming applications.

In the Magnetic Application Products segment, net sales increased by 6.6 billion yen, or 17.3%, and operating profit rose by 0.3 billion yen from the first quarter, including restructuring costs of 0.9 billion yen recorded in the second quarter. While total demand for nearline HDDs remained virtually flat from the first quarter, the sales volume of HDD heads increased about 40% from the first quarter, reflecting the frontloaded orders from the third quarter among other factors. Meanwhile, the sales volume of HDD suspension assemblies decreased about 5% from the first quarter, resulting in quarter on quarter growth in sales of HDD heads on the whole. Operating loss diminished, driven by an increase in sales volume when excluding the effect of restructuring costs of about 0.9 billion yen, which was recorded in the second quarter. Sales of magnets remained virtually unchanged from the first quarter and operating loss has decreased.

In the Energy Application Products segment, net sales increased by 29.1 billion yen, or 10.6%, and operating profit surged by 25.3 billion yen from the first quarter. Both sales and profits of rechargeable batteries increased on the whole from the first quarter as sales of small capacity rechargeable batteries increased for smartphone applications in China, despite a decline in sales of medium capacity rechargeable batteries as a result of the business transfer to JVs. Sales of power supplies for industrial equipment remained robust. While sales of power supplies for EVs remained virtually unchanged from the first quarter, profitability has improved.

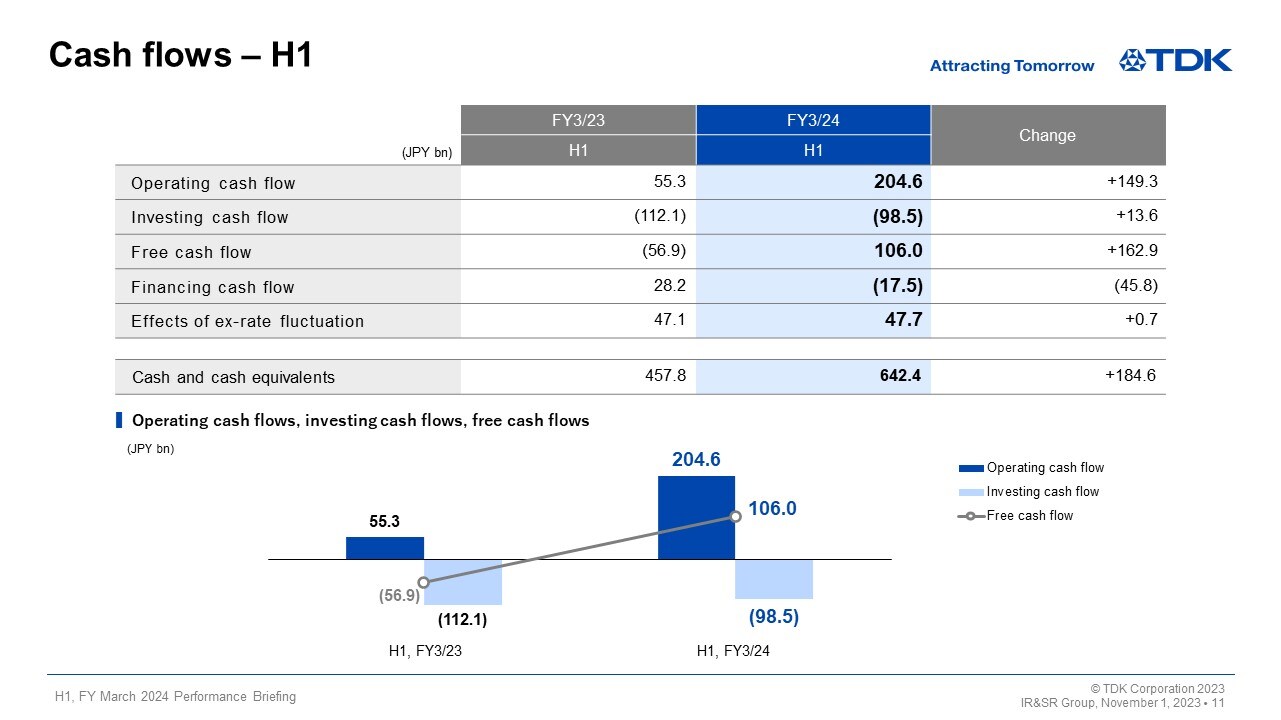

Cash flows – H1

Next, I would like to present an overview of cash flows.

For the first half of fiscal 2024, operating cash flow amounted to 204.6 billion yen, investing cash flow—such as capital expenditure—amounted to 98.5 billion yen, and free cash flow amounted to 106.0 billion yen. Operating cash flow increased significantly, reflecting thorough inventory optimization efforts and improvement in other working capital in light of market demand trends. In addition, as a result of implementing capital investment while carefully examining the demand-supply situation, free cash flow rose considerably.

While TDK made downward revisions to its projections for fiscal 2024 at the time of the first quarter earnings announcement on August 2, 2023, it did not revise its cash flow projections from the initial plan, maintaining its free cash flow projection of 80.0 billion yen for fiscal 2024. While free cash flow during the first half has significantly exceeded the level, we will continue to aim for further improvements in the second half.

This concludes my presentation. Thank you very much for your attention.

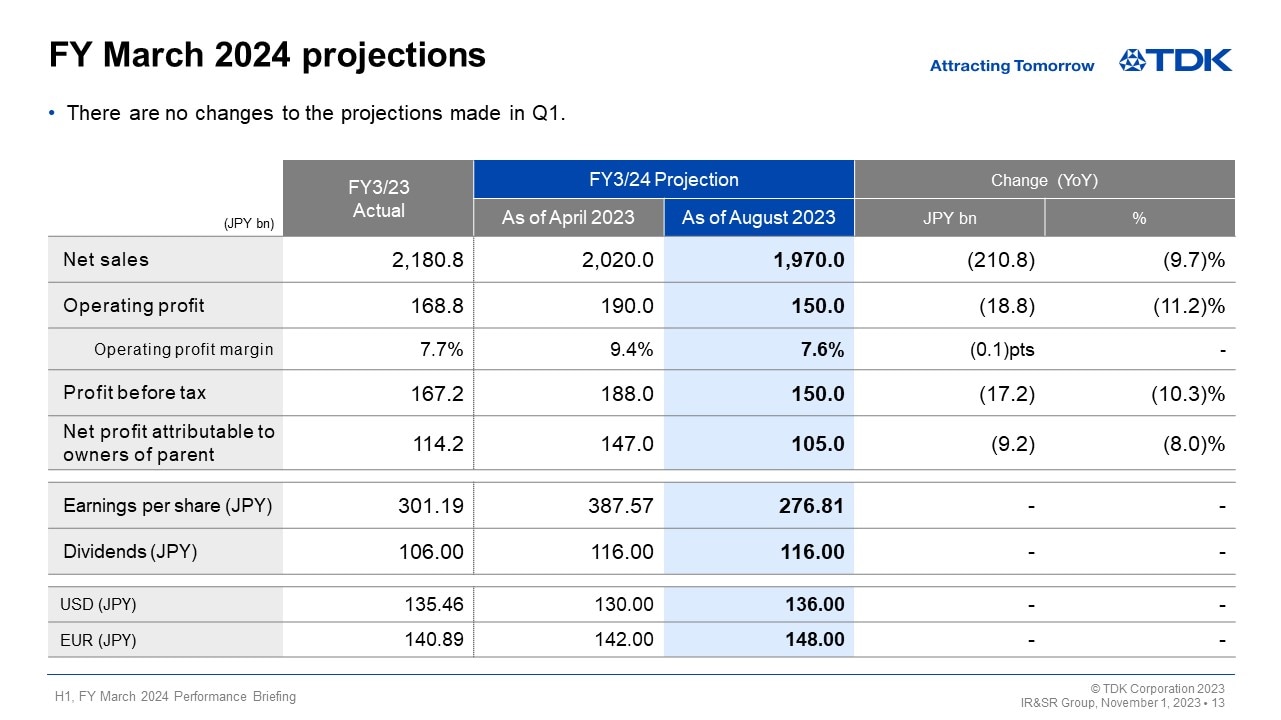

FY March 2024 Projections

Noboru Saito

President & CEO

Hello, I am Noboru Saito, President and CEO of TDK. Thank you for joining us today. I would like to go over our full year projections for the fiscal year ending March 2024.

FY March 2024 projections

Concerns over a slowdown of the global economy grew due to higher geopolitical risks, high interest rate policies in Europe and the United States aimed at tackling inflation, and an economic slowdown in China driven by a real estate slump.

Under these circumstances, although production in the electronics market slowed due to weakness in final demand, TDK’s performance for the first half of fiscal 2024 was impacted by factors such as the depreciation of the yen and exceeded the projections at the time of the first quarter earnings announcement on August 2, 2023.

In terms of forward projections, production volumes of smartphones and nearline HDDs for data centers are estimated to remain below the assumptions in August. In addition, demand recovery is expected to be delayed, especially in the industrial equipment market.

Also, the automotive market is expected to pick up more moderately than the previous forecast due to component inventory adjustments at some customers. Based on these factors, the market environment in which we conduct business is projected to remain uncertain.

Under such circumstances, our projections for fiscal 2024 have not been revised from the following projections announced in August: net sales of 1,970.0 billion yen, operating profit of 150.0 billion yen, and net profit attributable to owners of parent of 105.0 billion yen. There have been no changes from our initial projections for exchange rates for the second half of fiscal 2024, and our assumption is 130 yen against the U.S. dollar.

We will also maintain the free cash flow projection of 80.0 billion yen as announced in August and aim for further improvements given an increasing trend of operating cash flow.

We have also kept our initial annual dividend forecast unchanged.

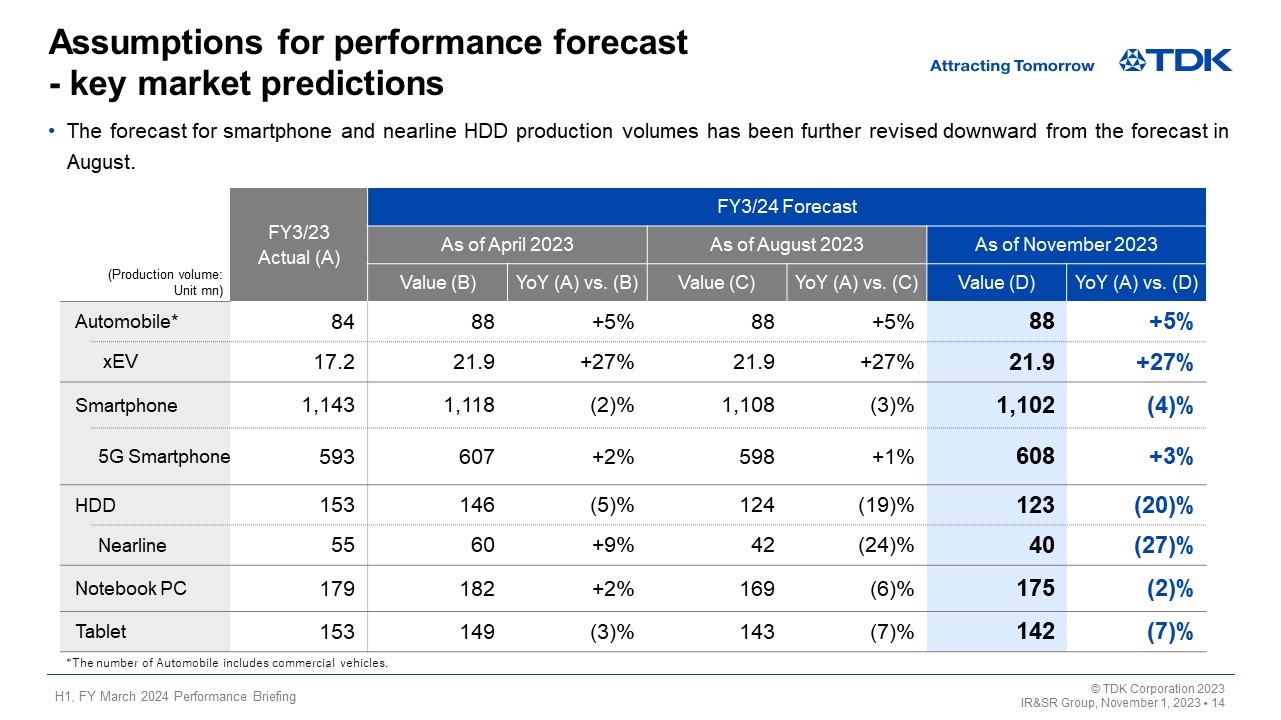

Assumptions for performance forecast - key market predictions

Regarding the assumptions in the performance forecast, I will talk about the revision of key market predictions.

In the automotive market, the semiconductor shortage and other issues are on the way to being resolved and the production volume of xEVs, in particular, has been steadily growing. Therefore, we have maintained our initial predictions for the production volume, despite some uncertainties. On the other hand, as predicted at the time of the earnings announcement in August, component demand is expected to pick up moderately in the future, despite some differences in component inventory adjustments among customers.

In the ICT market, while we had revised our initial forecast for the production volume of smartphones at the time of the earnings announcement in August, we revised it again from the August forecast of 1,108 million units to 1,102 million units.

In the HDD market, HDD inventory adjustments by customers have continued due to a rapid change in the environment surrounding data center investments. Given such situation, we have revised our prediction for the production volume of nearline HDDs once again, down from the August forecast to 40 million units.

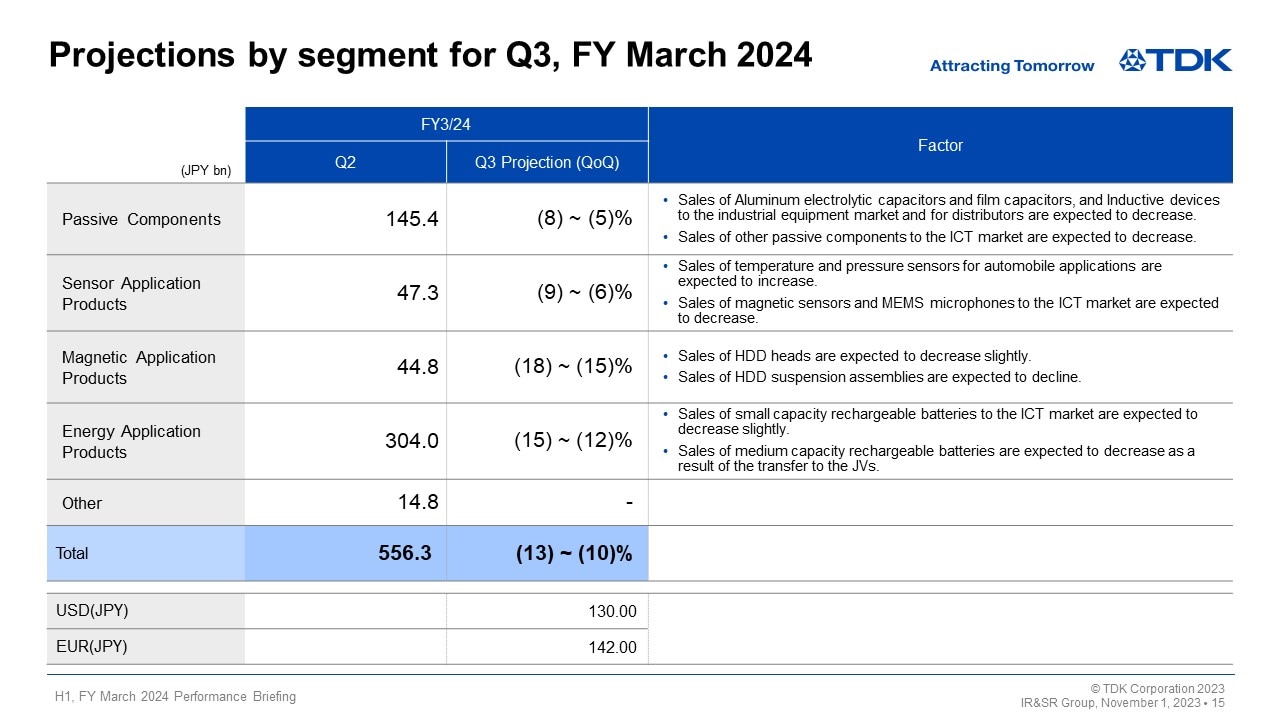

Projections by segment for Q3, FY March 2024

Now, I would like to discuss our projection regarding changes in net sales by segment from the second quarter to the third quarter of fiscal 2024.

This projection is based on the assumption that the yen will appreciate by about 14 yen against the dollar and the euro compared to the actual exchange rates during the second quarter, which is translated into negative effects of about 10% for each segment.

In the Passive Components segment, while sales of ceramic capacitors are expected to increase to the automotive market, sales of aluminum electrolytic capacitors and film capacitors to the industrial equipment market and sales of other passive components to the ICT market are anticipated to decline. As a result, the segment sales are forecast to decrease by 5–8% overall on a quarter on quarter basis.

In the Sensor Application Products segment, while sales of temperature and pressure sensors to the automotive market are expected to remain brisk, sales of magnetic sensors and MEMS microphones to the ICT market are predicted to decline in the third quarter due to the impact of components orders being frontloaded from the third quarter to the second quarter. As a result, the segment sales are forecast to decrease by 6–9% overall on a quarter on quarter basis.

In the Magnetic Application Products segment, the sales volume of HDD heads is expected to remain virtually unchanged from the second quarter to the third quarter as the orders for HDD heads and HDD suspension assemblies were also frontloaded from the third quarter to the second quarter. On the other hand, the sales volume of HDD suspension assemblies is predicted to decline by about 23% from the second quarter. As a result, the segment sales are forecast to decrease by 15–18% overall on a quarter on quarter basis. In the previous projection, we predicted that the sales volume of HDD heads would increase about 1.8 times in the second half compared to the first half of fiscal 2024. However, we currently predict that it will increase about 1.3 times given the frontloaded orders from the third quarter to the second quarter and the delay in the project launch, among other factors.

In the Energy Application Products segment, sales of small capacity rechargeable batteries are expected to decline slightly and sales of medium capacity rechargeable batteries will likely be affected by the progress in business transfer to JVs. As a result, the segment sales are forecast to decrease by 12–15% overall on a quarter on quarter basis.

Based on the above, we predict that total sales across all segments will decrease by 10–13% on a quarter on quarter basis.

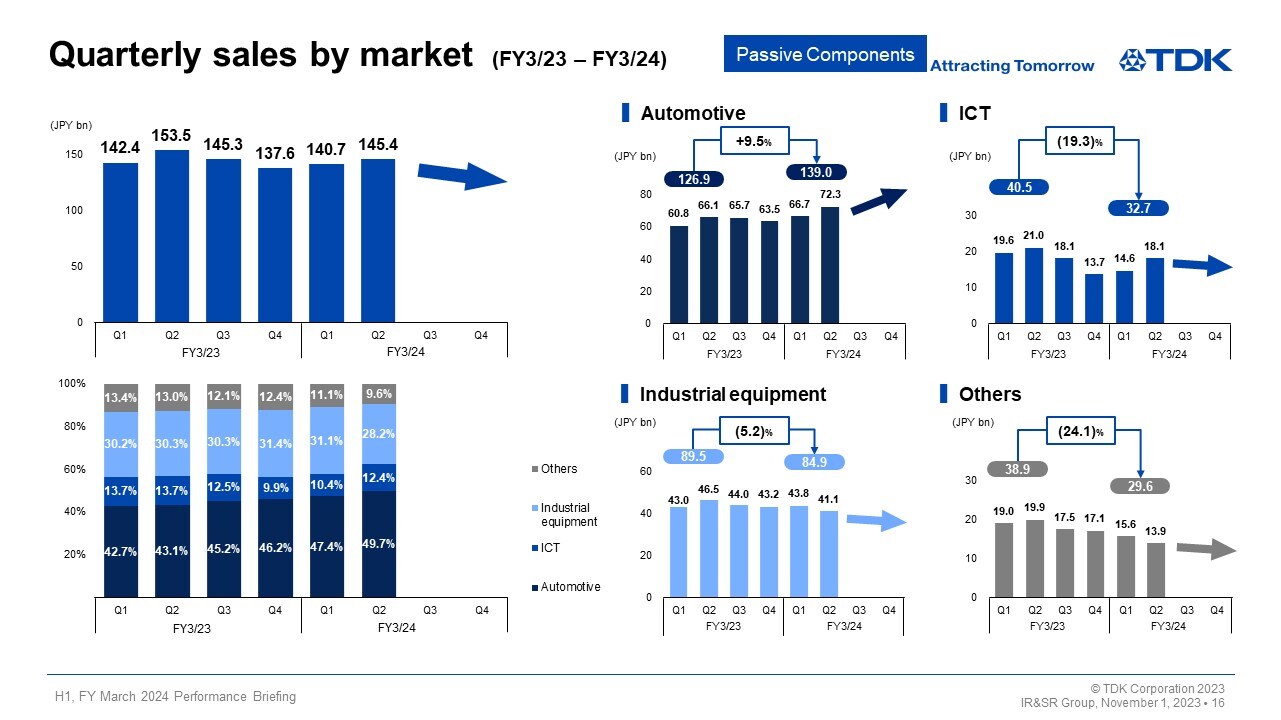

Quarterly sales by market (FY3/23 – FY3/24) -Passive Components-

In addition to our projection regarding changes in net sales by segment, I would like to provide an additional explanation on the future outlook of passive components by market based on the second quarter results.

Sales to the automotive market in the first half of fiscal 2024 increased 9.5% year on year, and sales are expected to continue to rise on a quarter on quarter basis. As for sales to the automotive market, we predict that this upward trend will continue given an increase in the number of xEVs and required components, despite some differences in component inventory adjustments among customers. On the other hand, in the first half of fiscal 2024, sales to the industrial equipment market decreased 5% year on year, those to the ICT market fell 19% year on year, and those to other markets, mainly to distributors, dropped 24% year on year. We expect this adjustment to continue a little longer.

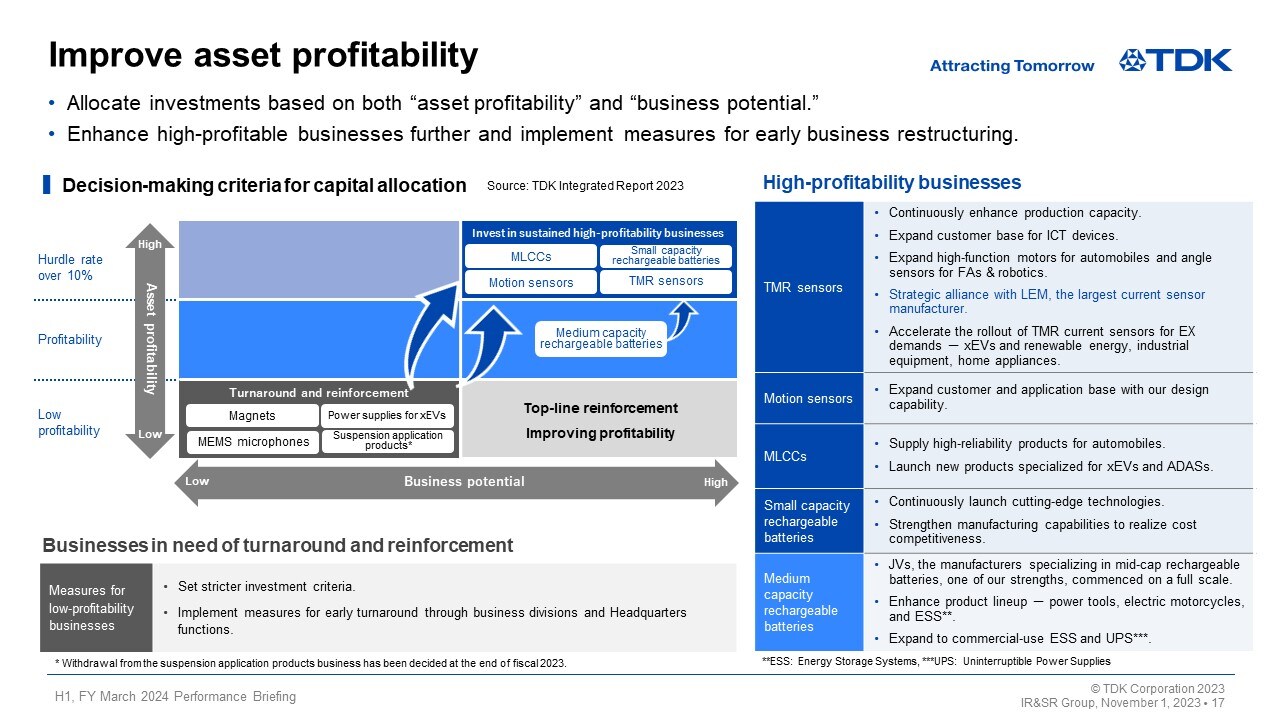

Improve asset profitability

Lastly, I will talk about our initiatives aimed at improving the asset profitability of TDK’s businesses.

At the beginning in fiscal 2022, we stratified our approximately 80 business units under four segments into six categories along two axes, “asset profitability” and “business potential.” We also clarified the criteria for capital allocation and have been revising and optimizing our portfolio. The positioning of major business units as well as the directions for growth and improvement are shown in the diagram.

We have set a weighted average cost of capital (WACC) of 10% as a hurdle rate for return on invested capital. We prioritize investments in business that clear this rate and have strong potential, including MLCCs, small capacity rechargeable batteries, TMR sensors, and motion sensors, treating them as sustained high-profitability businesses as shown at the right top of the diagram. This list includes those explained as strategic growth businesses at the beginning of the current fiscal year. Now, let me explain our measures for each business.

As announced in April, we will continue to enhance the production capacity for TMR sensors as the business is expected to grow continuously in the future, especially those related to ICT applications, such as smartphones, and angle sensors used in high-function motors for automotive and FA/robotics applications. As for current sensors for EVs, we commenced mass production last year. In addition, we decided to conclude a strategic alliance with LEM, the largest current sensor manufacturer, as announced in a press release on October 25. Through this alliance with the largest player in the industry, we will accelerate expansion into various applications, including those related to renewable energy, industrial equipment, and home appliances, in addition to automotive applications such as for EVs.

In terms of MEMS motion sensors, we believe that demand will grow significantly in the future as an entry point for information of various applications amid the growth of a DX-oriented society. In particular, sales to the automotive market have been brisk. We will continue to enhance our advanced design capability, looking ahead to sustainable market growth over the medium to long term.

In MLCCs, demand has been steadily growing mainly for high-function, high-reliability products used in xEVs and ADASs. We are steadily enhancing our production capacity with the aim of doubling it in fiscal 2025 compared to the level in fiscal 2021. We are also considering capacity expansion thereafter.

In small capacity rechargeable batteries, we will strive to maintain our position as a leader in small capacity rechargeable batteries to the ICT market by continuously developing and launching cutting-edge technologies. Significant growth in production volume of ICT devices, such as smartphones, cannot be expected. However, we will strive to secure profitability by increasing cost competitiveness through rigorous labor-saving, automation, and rationalization.

In medium capacity rechargeable batteries, our JVs with CATL commenced full-fledged mass production in April 2023, with steady progress in business relocation to the new plant. As the only manufacturer specializing in medium capacity rechargeable batteries, the JVs will aim to increase market share and sales by leveraging its broad product lineup, safety, long-term reliability, mass production know-how, and scale. The JVs will also expand applications in the future to industrial- and commercial-use ESSs and uninterruptible power supplies (UPSs) in addition to residential energy storage systems (RESSs). As for net sales consolidated at TDK, the JVs will aim to deliver more than mid-100 billion yen in fiscal 2027 and 400–500 billion yen by 2030.

Next, I will explain about businesses in need of turnaround and reinforcement at the left bottom of the diagram.

Magnets have been faced by the issue of delays in productivity improvements for products to the automotive market. We are aiming to achieve an early turnaround through the integration of capabilities by providing the resources of Headquarters functions, such as the Production HQ and the Materials Research Center, to business divisions. At the same time, we have set stricter investment criteria at the time of business acquisition for businesses related to the automotive market with a longer period from design-in to mass production.

In power supplies for EVs, we will aim for an early turnaround as procurement issues related to semiconductor shortages have been resolved and profitability has been improving.

In terms of MEMS microphones, we will strive to secure the lead by acquiring new businesses, as demand for digital microphones used in smartphones and wearable devices is expected to grow.

As just explained, we will strengthen our business portfolio by continuously implementing adequate measures for the turnaround of low-profitability businesses while further enhancing high-profitability businesses. While the current economic environment remains extremely uncertain, we will continue to promote our growth strategy by capturing the EX and DX trends through the implementation of measures.

Our measures that I just explained are linked with our basic stance toward the next Medium-Term Plan. While the specific details are scheduled to be announced in May 2024, we plan to enhance asset efficiency and significantly grow our strategic growth businesses—such as passive components and sensors—to become revenue pillars similar to rechargeable batteries in order to achieve a new growth stage at TDK.

This concludes my presentation. Thank you very much for your attention.