[ 3rd Quarter of fiscal 2017 Performance Briefing ]Consolidated Results for 3Q of FY March 2017

Consolidated Full Year Projections for FY March 2017

Mr. Tetsuji Yamanishi

Corporate Officer

I’m Tetsuji Yamanishi, Corporate Officer at TDK. Thank you for taking the time to attend TDK’s performance briefing for the third quarter of the fiscal year ending March 2017. I will be presenting an overview of our consolidated results.

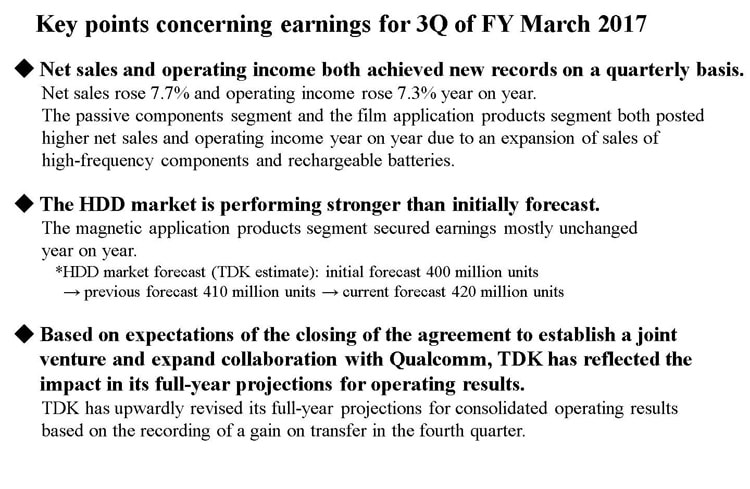

Key points concerning earnings for 3Q of FY March 2017

First, let’s take a look at the key points concerning earnings for the third quarter. There was a large year-on-year impact from the appreciation of the yen, which rose 12 yen, or 10%, against the U.S. dollar and 15 yen, or 12%, against the euro. In this environment, TDK increased both net sales and earnings. Net sales increased by 7.7% and operating income rose by 7.3% year on year. As a result, we set new record highs for both net sales and operating income on a quarterly basis.

In the automotive market, which has been trending firmly, TDK grew on a year-on-year basis despite a stronger yen by expanding sales of products that offer solid growth prospects, such as magnetic sensors and DC-DC converters for xEV, in addition to inductors and capacitors, where TDK has long held a high market share. Moreover, in the smartphone market, where growth is showing signs of slowing, passive components and film application products captured more stable demand by expanding their respective customer portfolios. As a result, passive components absorbed the impact of the yen’s appreciation to set a new record high for net sales on a quarterly basis and also generated operating income approaching a new record high. Film application products set new record highs for both net sales and operating income on a quarterly basis.

In the Passive Components segment, high-frequency components made significant progress on improving profitability through productivity improvements along with sales growth, helped in part by expanded sales of diversity modules in addition to discrete products. As a result, high-frequency components shrugged off the impact of the stronger yen to deliver much higher sales and income year on year, driving earnings of the Passive Components segment as a whole.

In rechargeable batteries, we are advancing on reducing our dependence on North American customers and building an expanded and more stable customer portfolio, through steady growth in sales to Chinese customers and growing sales for new applications such as drones and game consoles. In addition, we countered the impact of the yen’s appreciation and pressure for sales price reductions through improvements in productivity. As a result, in rechargeable batteries, we achieved both higher sales and income, setting new record highs on both fronts.

In HDD heads, TDK revised its projection for HDD demand. The projection has been increased to 420 million units, from the previous revised projection of 410 million units, as conditions for SSD demand and trends in PC demand have been heading in a better direction for the HDD market. Shipments of HDD heads for a Japanese customer remained strong. HDD head shipments increased by about 10% year on year, beating our initial estimation by around 30%, with HDD head sales increasing 2% year on year, despite the impact of the yen’s appreciation.

Since 2016, TDK has taken various strategic actions with the aim of expanding strategic growth products such as sensors and actuators, energy units and next-generation electronic components. As part of these efforts, TDK now expects to successfully close an agreement to establish a joint venture and expand collaboration with Qualcomm, as announced in January 2016. Therefore, based on expectations for recording a gain on transfer in connection with the closing of the agreement in the fourth quarter, we have upwardly revised our full-year projections for consolidated operating results.

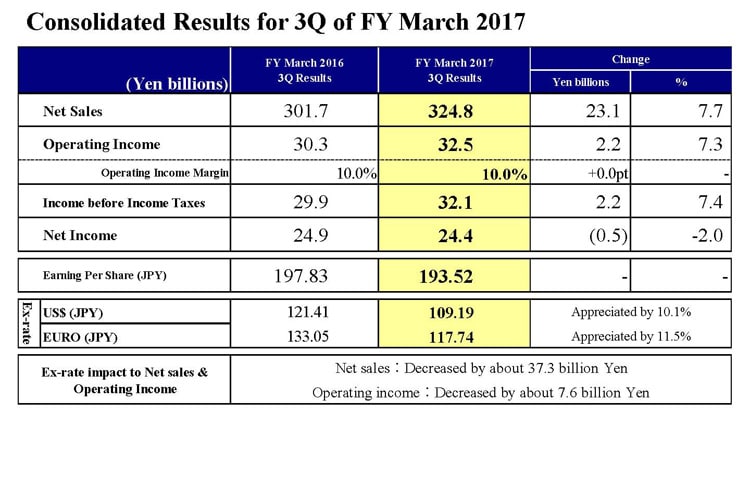

Consolidated Results for 3Q of FY March 2017

Next, let’s take a look at our results for the third quarter. Net sales were 324.8 billion yen, up 23.1 billion yen, or 7.7% year on year. Operating income increased 2.2 billion yen, or 7.3%, to 32.5 billion yen. We maintained a double-digit operating income margin of 10.0%, as we did in the third quarter of the previous fiscal year.

Income before income taxes was 32.1 billion yen, up 2.2 billion yen. Net income edged down to 24.4 billion yen for the third quarter.

Consequently, earning per share was 193.52 yen.

Average exchange rates for the period were 109.19 yen against the U.S. dollar, an appreciation of 10.1% year on year, and 117.74 yen against the euro, an appreciation of 11.5% year on year. In terms of the impact of these exchange rate movements, exchange rates pushed down net sales and operating income by around 37.3 billion yen and around 7.6 billion yen, respectively.

Regarding the exchange rate sensitivity, as before, we estimate that a change of 1 yen against the U.S. dollar will have an impact of approximately 1.2 billion yen on operating income, while a change of 1 yen against the euro will have an impact of approximately 0.7 billion yen.

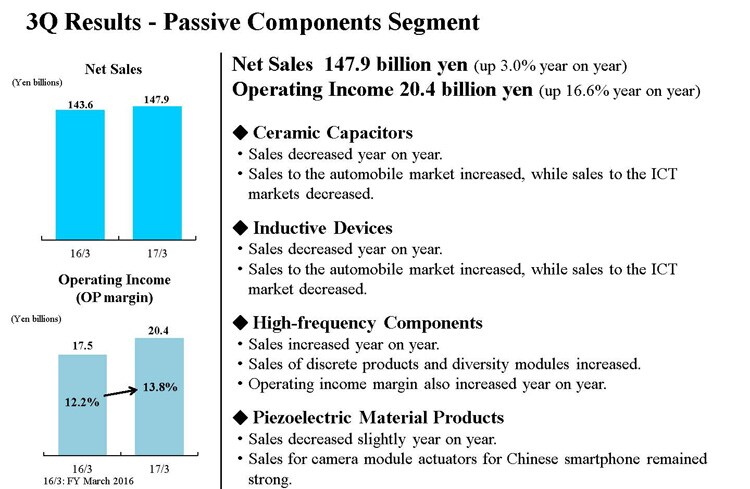

3Q Results - Passive Components Segment

Next, I would like to explain our business segment performance.

First, in the Passive Components segment, net sales were 147.9 billion yen, up 3.0% year on year, and operating income was 20.4 billion yen, up 16.6% year on year. The operating income margin was 13.8%. Profitability improved, absorbing the impact of the yen’s appreciation and expanding earnings.

In ceramic capacitors and inductive devices, sales to the automobile market were solid, particularly in North America, Europe and China, outweighing the impact of the yen’s appreciation. Sales of ceramic capacitors and inductive devices in the automotive market account for around half of the overall sales for both products. Meanwhile, sales decreased to the ICT market, particularly sales for use in smartphones.

High-frequency components continued to see favorable sales of discrete products for smartphones to a major customer in North America, as well as in China and South Korea. Moreover, although Wi-Fi module sales volume declined, the increase in diversity module sales to major customers in North America absorbed the impact of foreign exchange, leading to a 1.5-fold effective increase in sales overall. Operating income increased significantly, reflecting a utilization gain from an increase in production in the run up to the third-quarter production peak and improved earnings from module products, in addition to higher earnings from an increase in sales volume. As a result, high-frequency components drove not only the earnings of the Passive Components segment, but also of the Company as a whole.

In piezoelectric material products, we continued to see strong sales of actuators for camera modules to smartphone manufacturers in China.

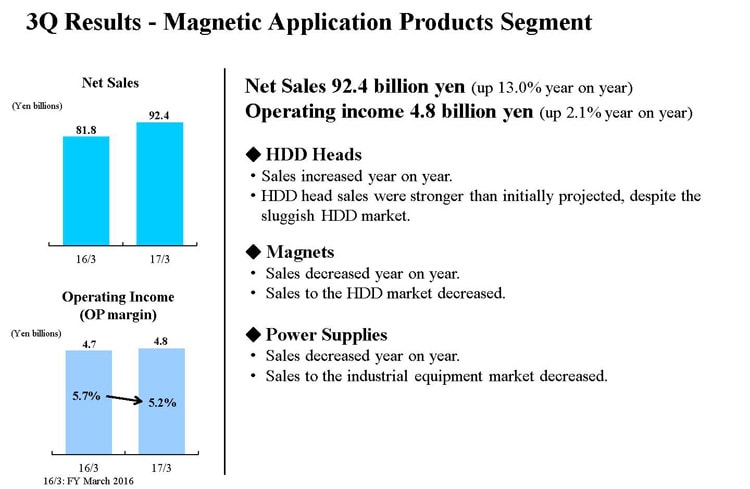

3Q Results - Magnetic Application Products Segment

Turning to the Magnetic Application Products segment, net sales were 92.4 billion yen, an increase of 13.0% year on year. Operating income rose by 2.1% year on year to 4.8 billion yen, with an operating income margin of 5.2%.

In HDD heads, shipments of 2.5-inch HDD heads for a Japanese customer continued to show strong activity, with no signs of a change in trends from the start of the current fiscal year. Combined with increased sales of 3.5-inch HDDs following a switch to full-turnkey sales, the impact of the yen’s appreciation was absorbed and HDD sales increased by about 2%. With the HDD shipments of the first quarter of the previous fiscal year indexed as 100, the third-quarter shipment index came in at 126, beating the previous estimation of 119, increasing 10% year on year. In terms of profitability, we delivered higher profits from HDD heads owing to improved profitability, despite the impact of the yen’s appreciation, due partly to an increase in a utilization gain derived from the benefits of integrating wafer sites. This was partly offset by a decline in earnings due to sales price reductions for new products and an end to HDD assembly sales to a North American customer.

In magnets and power supplies, sales decreased due to the impact of the yen’s appreciation, although sales were largely flat year on year on an adjusted basis excluding the foreign exchange impact. In magnets, conditions remained severe, mainly due to a decline in HDD magnet sales in line with a drop in HDD demand. However, sales increased in motors for wind power generation, which are part of our efforts to bolster the industrial equipment business.

In power supplies, sales to the measuring equipment market in Europe declined slightly, but sales for use in industrial equipment grew steadily in other regions.

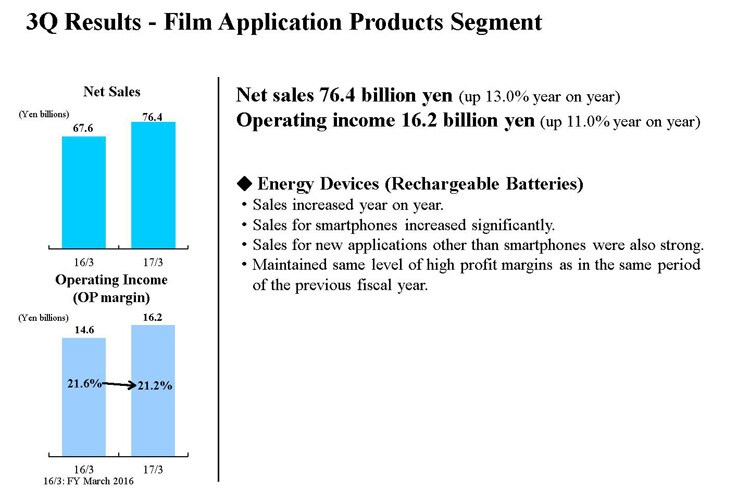

3Q Results - Film Application Products Segment

Next is the Film Application Products segment. In this segment, net sales were 76.4 billion yen and operating income was 16.2 billion yen. Sales rose by 13.0% and profits increased by 11.0%. The segment has maintained high profitability in conjunction with growth in the size of business. It has achieved a high operating income margin of over 20%, the same level as in the third quarter of the previous fiscal year.

In rechargeable batteries, sales outperformed the previous projection for the third quarter, despite a year-on-year decline in sales to a North American customer. In addition, sales to smartphone manufacturers in China roughly doubled year on year. Moreover, sales increased for new applications other than smartphones, such as drones and game consoles. TDK achieved much higher sales and profits as a result of meeting increased demand by executing timely investments to boost production capacity in conjunction with increasing productivity.

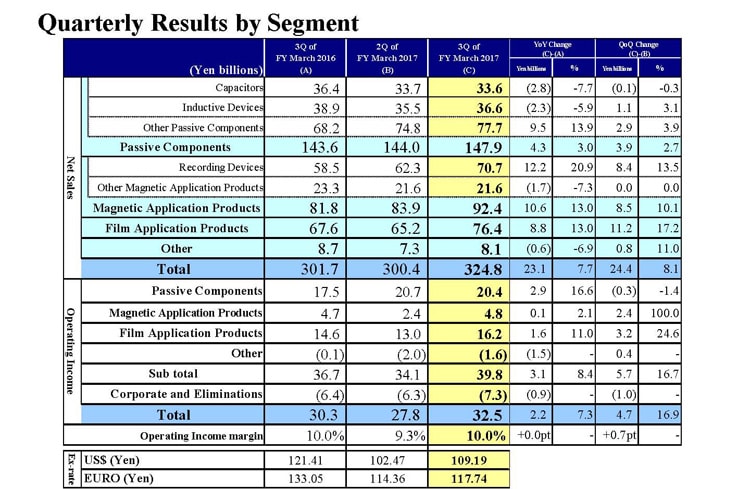

Quarterly Results by Segment

Next, I would like to explain the factors behind the changes in segment net sales and operating income from the second quarter to the third quarter. First, as was done previously, certain products have been reclassified between segments. Certain products in the Film Application Products segment have been reclassified to the Other segment from the current fiscal year. This change had the impact of increasing net sales of the Other segment by 0.8 billion yen in the third quarter of the previous fiscal year. Also, certain products in the Other segment have been reclassified to the Passive Components segment from the current fiscal year. This change had the impact of increasing net sales of the Passive Components segment by 2.1 billion yen in the third quarter of the previous fiscal year. These reclassifications had virtually no impact on operating income.

Let’s now look at the changes in each segment, beginning with the Passive Components segment. In this segment, net sales increased by 3.9 billion yen, or 2.7% from the second quarter. Capacitor sales were strong to the automotive market but declined for use in ICT. In aluminum electrolytic capacitors and film capacitors, sales to the automotive market were strong, but were sluggish for use in industrial equipment, remaining mostly flat from the second quarter, owing to the continuing impacts of decelerating economies, particularly China, and low crude oil prices. Excluding the impact of the yen’s depreciation, sales decreased by about 6%. Sales of inductive devices declined by 1.1 billion yen, or 3.1%, from the second quarter. Sales to the automotive market remained favorable, but sales for use in industrial equipment declined. Excluding the impact of the yen’s depreciation, sales decreased only slightly. In other passive components, sales increased by 2.9 billion yen, or 3.9%. Sales of high-frequency components were generally strong across the board.

However, there were some adjustments at certain Chinese customers stemming from the supply of parts. Sales of actuators for camera modules were strong to Chinese customers but declined slightly when excluding the impact of the yen’s depreciation.

Operating income in the Passive Components segment decreased slightly by 0.3 billion yen, or 1.4%, from the second quarter. In terms of profitability, the operating income margin was maintained at about 14%, albeit decreasing slightly.

Next is the Magnetic Application Products segment. In this segment, net sales increased by 8.5 billion yen, or 10.1%, from the second quarter. In recording devices, sales rose by 8.4 billion yen, or 13.5%. The main contributing factors were an increase of around 2% in the HDD head shipment index to 126 in the third quarter, up from 124 in the second quarter, an increase in full-turnkey sales of 3.5-inch HDDs, and an increase in sales of about 6.0 billion yen from the consolidation of Hutchinson from the third quarter. Operating income in the Magnetic Application Products segment increased by 2.4 billion yen, doubling from the second quarter. In HDD heads, the main contributors were a utilization gain from the integration of front-end process sites, along with increased sales and profit due to growth in shipment volume of 2.5-inch heads.

Moving on to the Film Application Products segment, net sales increased significantly by 11.2 billion yen, or 17.2%, from the second quarter. There was a large increase in sales to Chinese customers, and strong sales to a North American smartphone customer were posted in line with initial forecasts. As a result, the customer portfolio balance improved as the sales mix to North American customers declined. Operating income rose by 3.2 billion yen, or 25%, to 16.2 billion yen from the second quarter. We achieved significant earnings growth even on an adjusted basis excluding the impact of the yen’s depreciation as an increase in marginal profit due to higher sales volume, and the pursuit of cost improvements, absorbed the impact of severe sales price reductions.

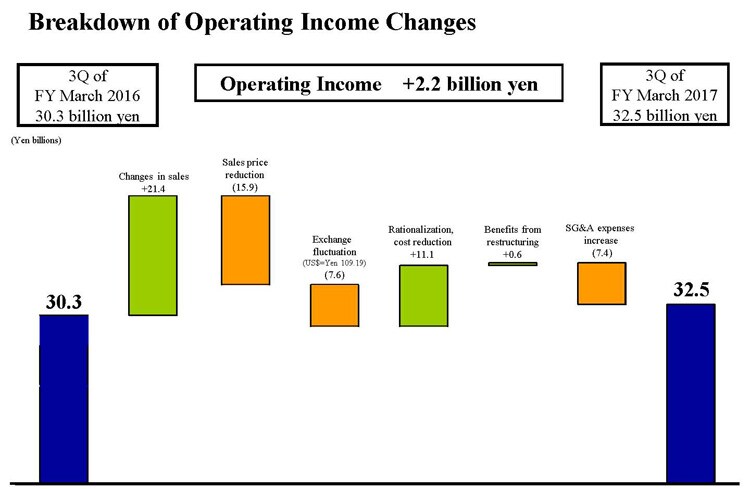

Breakdown of Operating Income Changes

Next is the breakdown of changes in operating income. Looking at the factors behind the 2.2 billion yen increase in operating income, the first factor, changes in sales, had a positive impact of approximately 21.4 billion yen, reflecting sales increases attributable to factors including capacity utilization and product mix. The main contributor here was continued strong sales of high-frequency components and rechargeable batteries.

The next factor, sales price reduction, had a negative impact of approximately 15.9 billion yen, with an average sales price reduction rate of about 5%. Exchange fluctuation, specifically the stronger yen, had a negative impact of approximately 7.6 billion yen on operating income. Rationalization and cost reduction, in combination with progress on boosting efficiency and improving production yields, as well as discounts on raw materials, had a positive impact of 11.1 billion yen. Benefits from restructuring lifted operating income by 0.6 billion yen. An increase in SG&A expenses had a negative impact of 7.4 billion yen on operating income. Around half of this increase was attributable to relevant expenses incidental to M&A activity. The main components were increased expenses for consolidating Micronas and Hutchinson, restructuring expenses to boost efficiency after the acquisition of Hutchison, expenses related primarily to preparations for establishing a joint venture with Qualcomm, and M&A expenses related to the acquisition of InvenSense and other entities. The remainder comprised an increase in selling expenses in step with sales expansion and an increase in expenses incurred to strengthen development activities. The main components of development expenses were research and development expenses for strengthening new product development and process development in connection with the expansion in high-frequency components and rechargeable batteries and for promoting the TDK Monozukuri revolution.

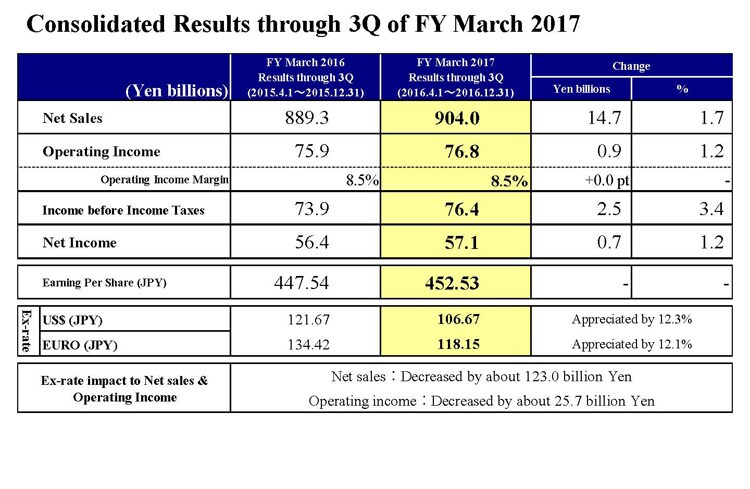

Consolidated Results for 3Q of FY March 2017

Next, let’s take a look at consolidated results for the first three quarters of the fiscal year ending March 2017.

For the nine-month period, net sales were 904.0 billion yen, an increase of 1.7% year on year. Following on from the previous fiscal year, TDK has once again set a new historical high for a nine-month period. Operating income was 76.8 billion yen, up 1.2% year on year. As with net sales, this is also a new historical high for a nine-month period. Net income rose 1.2% to 57.1 billion yen.

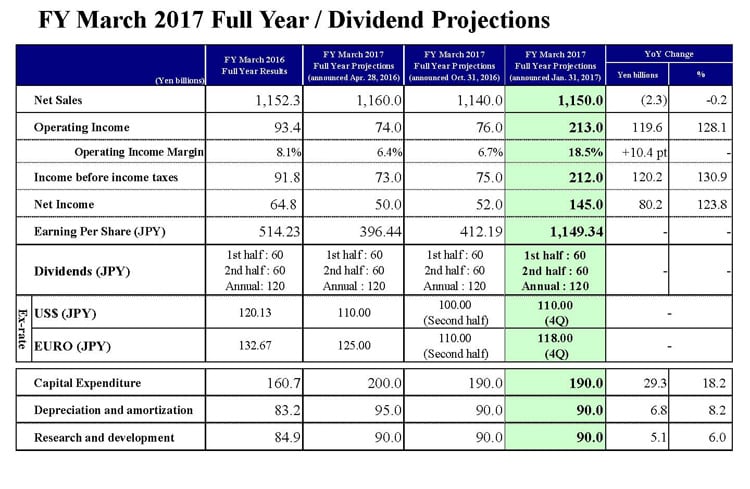

FY March 2017 Full Year / Dividend Projections

Finally, I will explain our full-year consolidated earnings projections.

First, let me point out that the assumed average foreign exchange rate of the initial announcement has changed. For the fourth quarter, the exchange rate assumption has been revised to 110 yen to the U.S. dollar and 118 yen to the euro.

As I explained at the beginning, TDK now expects to successfully close its agreement with Qualcomm. Therefore, we have revised our full-year projections for consolidated operating results by factoring in a gain on transfer in connection with the closing of the agreement.

The gain on transfer reflects operating income and income before income taxes of 149.0 billion yen and net income of 120.0 billion yen. In conjunction with the closing of the agreement, the high-frequency components subject to the agreement will be deconsolidated after the closing. As a result, TDK expects net sales to decrease by about 20.0 billion in the fourth quarter, and operating income and income before income taxes to both decrease by about 2.0 billion yen.

Looking at the revisions excluding these impacts, TDK previously announced a revised net sales forecast of 1,140.0 billion yen. We have increased this forecast by 30.0 billion yen to reflect the impact of the yen’s depreciation, bringing the forecast to 1,170.0 billion yen.

Deducting the impact of deconsolidation of 20.0 billion yen from the forecast, the newly revised net sales forecast is 1,150.0 billion yen. In terms of operating income, TDK previous announced a revised operating income forecast of 76.0 billion yen. We have increased this forecast by 10.0 billion yen to 86.0 billion yen. Deducting the impact of deconsolidation of 2.0 billion yen, we are now projecting operating income of 84.0 billion yen. Leveraging the collaboration with Qualcomm, we will accelerate earnings growth through three strategic growth products, with the aim of achieving sustained growth. Meanwhile, we will accelerate the transformation of the earnings structure of existing businesses. Restructuring expenses that will lead to a stronger earnings structure are projected at about 20.0 billion yen in the fourth quarter. In HDD heads, we will book impairment losses on long-lived assets in connection with the conversion of domestic wafer sites to the TMR sensor business. In metal magnets, we will book impairment losses on long-lived assets in connection with the shift from an earnings structure overly reliant on HDDs to a product portfolio focused on automobiles and industrial equipment, with the aim of fundamentally transforming our earnings structure. In aluminum electrolytic capacitors, we will book impairment losses on goodwill and long-lived assets in connection with our shift from an over-concentration on products for infrastructure markets that are significantly swayed by business cycles to expanding products for automotive markets where TDK is competitive. By boldly implementing structural reforms focused on these initiatives, TDK will work to build up its earnings base.

Based on these factors, TDK has upwardly revised its projections for consolidated operating results. Including the gain on transfer, we are now projecting net sales of 1,150.0 billion yen, operating income of 213.0 billion yen, income before income taxes of 212.0 billion yen and net income of 145.0 billion yen. We have also revised our projection for earning per share to 1,149.34 yen. As for the gain on transfer, we will prioritize reinvesting in the expansion of strategic growth products that is currently under way. Based on this, our dividend outlook calls for maintaining the final dividend at 60 yen per share, for an annual dividend of 120 yen per share.

That concludes my presentation. Thank you for your attention.